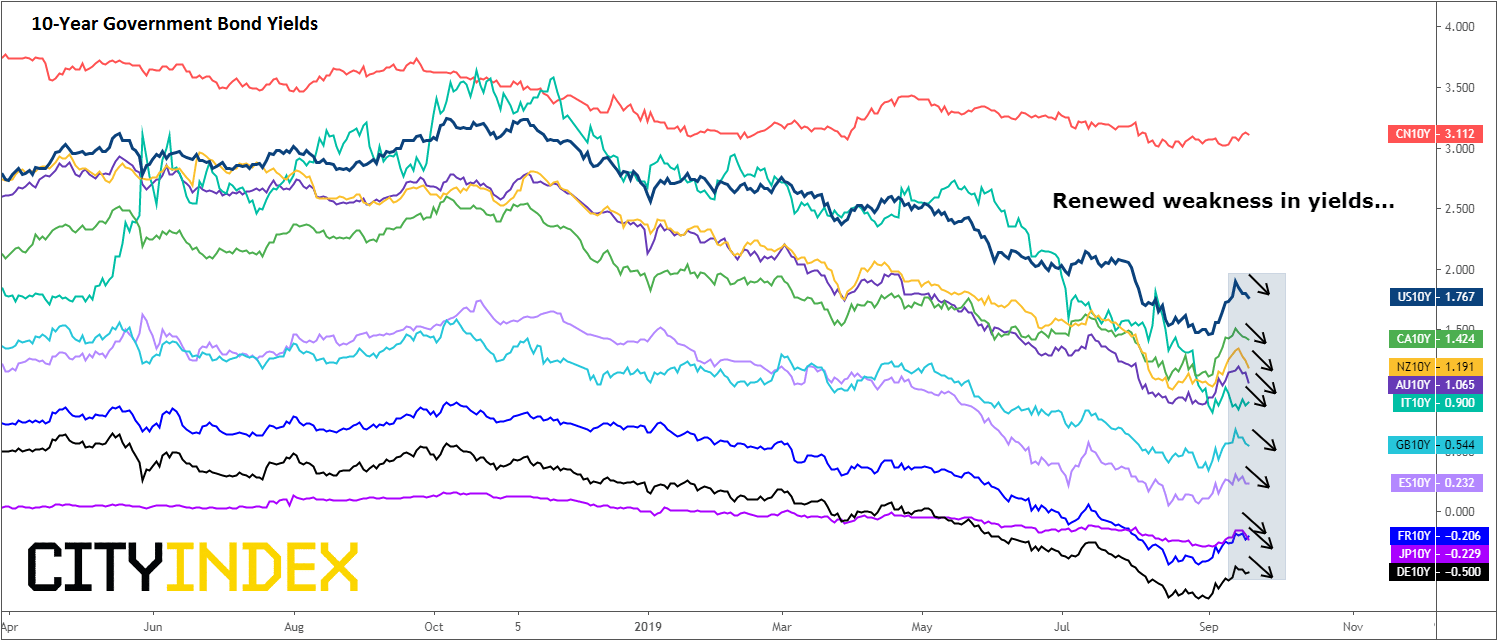

Over the past 24 hours or so, we have seen lots of central bank action (or inaction) and the message has been clear: global interest rates will remain at or near record lows for the foreseeable future. For that reason, yields have come under renewed pressure (see the chart below). This is helping to keep equity indices supported and near record levels in the case of the US, keeping the bears at bay despite raised geopolitical tensions and concerns over global demand hurting company earnings.

Source: Trading View and City Index.

This week’s main event was the Federal Reserve’s rate decision last night. As widely expected - and much to the displeasure of US President Donald Trump - the Fed did indeed cut interest rates by 25 basis points for the second consecutive meeting. There were three dissenters with Rosengren and George voting for no change again, while Bullard called for a larger 50 bps cut. But contrary to expectations, there was an element of a hawkish surprise as the so-called dot plots revealed a median view for a pause through to next year, rather than 2 more cuts expected. Still, it wasn’t hawkish enough to completely derail the rally on Wall Street.

The Bank of England was the latest major central to make a decision on interest rates today. “Shockingly,” it decided to leave its monetary policy unchanged. But it did strike a dovish tone, as it raised the prospects of a rate cut for the first time should Brexit uncertainty persists. The MPC said there was “entrenched uncertainty” over Brexit, which means “domestically generated inflationary pressure would be reduced”.

Elsewhere, the central bank of the world’s third largest economy disappointed some very hopeful expectations overnight despite exports falling there for the ninth consecutive month. The Bank of Japan decided to leave all policy settings unchanged, as widely expected. Its forward guidance was the same: extraordinary low policy to remain unchanged for an extended period at least through spring 2020.

In Hong Kong, the central bank decided to lower its base rate by 25 basis points to 2.25%, as expected and in tandem with the Fed.

Meanwhile there was some speculation that the Swiss National Bank would take some sort of policy action following the European Central Bank’s decision last week to re-introduce QE and cut rates further into negative. But the SNB decided against such a move this morning, even though it slashed its growth forecast for the year due to rising global headwinds.

Now there was one central bank which bucked the trend again and lifted interest rates. Norway’s central bank decided to hike rates by 25 basis points to 1.5%. This was Norges Bank’s fourth hike in the past year but probably it’s last for a while as other banks ease policy.Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Bonds articles

April 18, 2024 06:20 AM

April 10, 2024 01:09 AM

March 19, 2024 02:30 AM

March 15, 2024 01:38 AM