Yen stands to gain if US inflation also misses

Updated 16th September 9.37am BST Thursday’s US economic data continue the thread of weakness that has been seen for several weeks, setting the stage for […]

Updated 16th September 9.37am BST Thursday’s US economic data continue the thread of weakness that has been seen for several weeks, setting the stage for […]

US retail sales fell more than expected in August amid weak purchases of automobiles and a range of other goods, pointing to cooling domestic demand that could diminish expectations of a Federal Reserve interest rate increase next week even further. Retail sales declined 0.3% after an upwardly revised 0.1% gain in July. Retail sales in July were previously reported as flat. Sales were up 1.9% from a year ago.

Excluding automobiles, gasoline, building materials and food services, retail sales slipped 0.1% last month after a downwardly revised 0.1% drop in July. These so-called core retail sales correspond most closely with the consumer spending component of gross domestic product. They were previously reported to have been unchanged in July. Economists had forecast overall retail sales would tick 0.1% lower and core sales would inch 0.3% higher last month.

Coming on the heels of reports showing a slump in manufacturing activity in August and a slowdown in job growth, the retail sales data temper hopes of a strong rebound in economic growth in the third quarter. The report also suggests the Fed will leave interest rates unchanged at its 20th-21st September policy meeting. Federal Reserve Board Governor Lael Brainard said on Monday she wanted to see stronger consumer spending data and signs of rising inflation before raising interest rates.

The US’s industrial production data for August also came in below expectations on Thursday. A sharp decline in utilities output was the main reason according to the Federal Reserve board.

Industrial output fell 0.4% last month after a downwardly revised 0.6% increase in July. Last month, manufacturing output also declined 0.4%. Economists polled by Reuters had forecast industrial production would ease 0.3% last month. The industrial sector measured by the US central bank comprises manufacturing, mining, and electric and gas utilities. It had recently picked up after declining for much of the last 18 months but continues to struggle to shake off the dampening effects of weak global demand, a strong dollar and low oil prices.

Last month, there were some positive signs for the hard-hit energy sector, with mining output rising 1.0%, its fourth consecutive monthly increase. However, the index for utilities fell 1.4%. Business equipment output also dropped 0.4%, with cutbacks of nearly 2% for industrial and other equipment, the Fed said.

With overall output decreasing, the percentage of industrial capacity in use fell 4 tenths of a percentage point in August to 75.5%, from an unrevised 75.9% in July. Given that the Fed sees industrial capacity use as a leading indicator in deciding how much further the economy can grow before sparking higher inflation, the industrial reading does not bode well for a rate hike and it might have some read-through to Friday’s key Consumer Price Index update.

A very modest rise of 0.1% is the consensus for the seasonally adjusted monthly rate of inflation after zero growth in July, whilst an unadjusted yearly rise of 1% is foreseen, the latter representing an advance from 0.8% the month before. Core rates, which exclude volatile food and fuel costs and which traders tend to react to more, are forecast to rise 0.2% monthly and 2.2% annually, both unchanged from July.

Economists point to eye-catchingly sharp declines in vehicle prices and airline fares—perhaps pointing to domestic promotional activity—leaving scope for bounces that could bolster inflation, enabling it to reach or perhaps exceed expectations. On the other hand, already fragile monthly inflation readings could easily evaporate should no particular economic sector come to the rescue of inflation, and even the steadier core figure could also begin to retreat.

The deterioration of US economic gauges of late has been well-represented in the US Dollar Index which has ground about 2% lower from July highs to date.

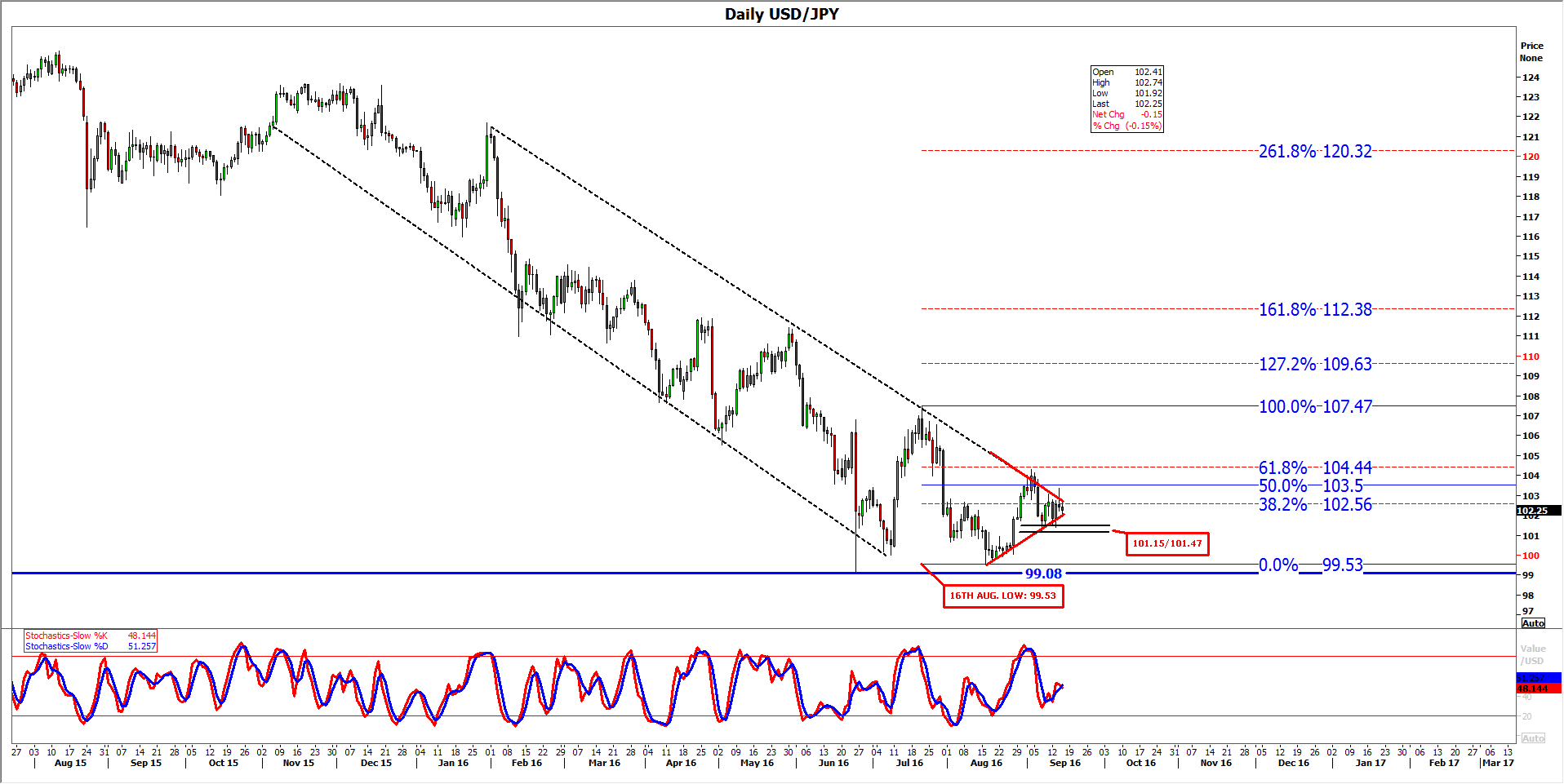

Ironically, the dollar’s overall decline does not appear to be reflected in the USD/JPY pair which has risen 2.4% since touching 99 yen per dollar for only the third time since 2013 albeit the second time within about two months. The USD/JPY’s reputation for being more linked to the global economy and a proxy for economic risk-seeking (when it rises) may account for the relative strength of the dollar against the yen in recent weeks.

Despite the dollar’s decline against other major currencies due to weakening macroeconomic and interest rate expectations, global markets have found a base this week after a shaky start and last week’s jitters.

Even so, the USD/JPY has declined significantly this year (representing a rally by the yen) in step with an increasingly uncertain outlook for the Bank of Japan’s quantitative easing policies and the dollar’s bounce against the yen appears to be reaching an important medium-term juncture.

Whilst the rate again failed to break through the 99 yen level on 16th August, confirming that price’s status as a support, the pair’s shorter-term rising trend is now triangulating against an upper bound of the USD/JPY’s decline this year, potentially setting the stage for a ‘breakout’ which could imply a sharp move, though technical analysis cannot tell us definitively whether that will be up or down.

Either way, the USD/JPY does seem to be coming to a tipping point that is coinciding with increasingly soft US economic data.

Traders note that USD/JPY tagged (early this month) the important 61.8% Fibonacci retracement interval of the summer’s rise to a high of 107.47 yen on 21st July. USD/JPY’s failure to breach that implied resistance level placed the rate on watch for a potential retest of 99 yen despite its seven-day recoupment following a major setback on 6th September.

A first hurdle for the dollar is a 38.2% Fibonacci, at 102.56 which was being tested at the time of writing. A climb above it on Thursday night would buttress any move to 104.4 (61.8%).

Then yen, however, still stands to gain (i.e. USD/JPY may fall) should frustration with the US’s economic progress this year turn into something more like anxiety.

If even the mediocre expectations about US inflation in August are not met, it’s possible the yen’s safe-haven role for markets will again come into focus.

The extent of USD/JPY’s down leg in any event will be lengthened should it lose recent support between 101.15/101.47.

Please click image to enlarge