Yen Shorts Yield Lows amp five year Cycles

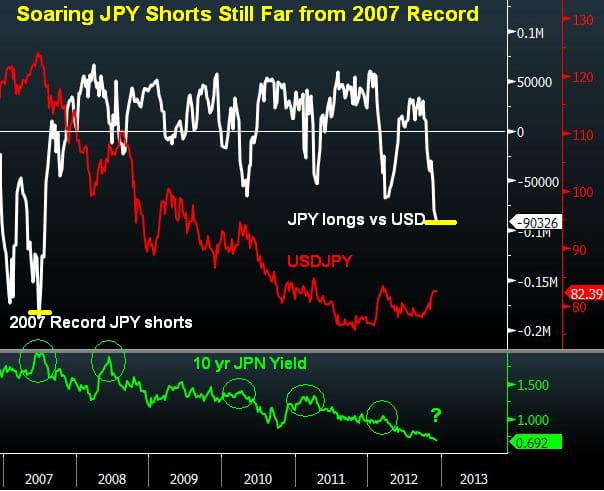

Escalating yen shorts against the USD in the Chicago Mercantile Exchange which shows the highest negative positioning in the currency since the June 2007. Back […]

Escalating yen shorts against the USD in the Chicago Mercantile Exchange which shows the highest negative positioning in the currency since the June 2007. Back […]

Escalating yen shorts against the USD in the Chicago Mercantile Exchange which shows the highest negative positioning in the currency since the June 2007. Back then, USD/JPY was at a five-year high of 124.14, global equities hit new records, private equity deals were raging with extreme leverage and even busts in US mortgage providers were still under the media radar.

Also in June 2007, yields on 10-year Japanese government bonds jumped by more than 40 bps to exceed 1.80%. The yield rally was broad throughout the global sovereign complex, prompting Japanese investors to flee zero interest rates to chase returns abroad. Unsurprisingly, yields on the US 10-year note also a hit a five-year high at 5.32%.

Today, the yen is entering its third consecutive monthly decline amid expectations that LDP Shinzo Abe will force the Bank of Japan into extreme easing of monetary policy when he is likely to win the elections on Dec 16. Stepping up military and construction spending and pressing on the asset purchases accelerator are part of Abe’s goal of attaining a new 2-3% inflation target.

But the missing link remains in bonds. Unlike in 2007, when global yields were soaring in tandem on an overheating global economy and emerging inflation fears, today’s yields are mired by margin suppression, financial repression, interventionist central banks and continuous downgrades of global growth by the IMF and all major central banks. 10-year JGBs remain adrift at generation lows below 0.70%, while their US counterparts are 30 bps above their lows.

With the yen falling at such a pace despite languishing yields may lead us to imply that the current yen sell-off would quickly intensify by a mere blip in global yields.

Yen shorts against the US dollar have hit a five-year of 90,000 contracts. As high as this may seem, it pales to the 188,000 contracts of yen shorts in June 2007. And thus, it may well be that in order for JPY shorts to breach above the 100,000 contracts territory, markets may need some help from further run-up in equities. This could well transpire from a temporary deal on the Fiscal Cliff, a more durable resolution for Greece or the next equity assault on the bears following the latest round of asset purchases from the Fed. Equities may not be at the lofty levels of 2007, but are successfully shaking off the European woes and fears of a Fiscal Cliff. Germany’s Dax index is competing with its emerging Asian counterparts in the +25% YTD territory, the FTSE-100 attempts in breaking the 6,000 level, while US equities remain resilient atop their 200-DAY MAs. We await the rest of the pieces to fall into place.