Yen 8217 s Reflexive Rebounds During Risk off

Some pundits have indicated that the yen is no longer a safe haven, and has now started to fall even when markets decline. That is […]

Some pundits have indicated that the yen is no longer a safe haven, and has now started to fall even when markets decline. That is […]

Some pundits have indicated that the yen is no longer a safe haven, and has now started to fall even when markets decline. That is false.

The yen may be bruised by the Bank of Japan’s willingness to unleash a monetary shock-&-awe, but stating that the yen is no longer a safe haven is a flawed. Some are basing this argument on the deteriorating correlation between the yen and the Vix.

That is inaccurate on several levels.

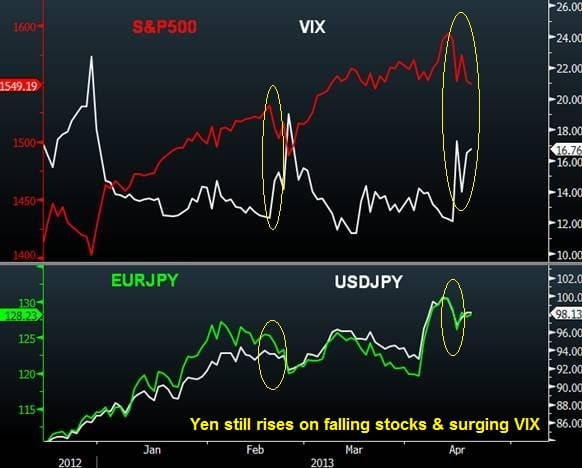

Firstly, the yen’s reflexive rallies during market sell-offs continue to emerge.

On February 25, the yen jumped 2.7% versus the euro and 1.7% against the US dollar (significant moves by FX market standards), while the S&P00 fell 1.8% on the day, its biggest percentage decline of the year at the time.

On April 15, the yen rose 2% and 1.4% versus the euro and the US dollar respectively, as the S&P500 plummeted 2.3%, its biggest decline of the year.

Judgements may be clouded by the fact that equities have not been subject to any real test by the bears. Thus, year-to-date, the yen is down 12% versus the euro and down 13% against the US dollar, while the S&P500 is up 10%. But note that the VIX is up 15% year-to-date, at a time when so-called “risk” markets are also higher.

These episodes clearly highlight the Japanese yen retains its safe haven lustre during intraday and intraweek sell-offs. One reason is that the US dollar cannot solely and continuously assume the role of safe-haven currency at a time when neither the majority of Federal Reserve members, nor US data support the case for reducing asset purchases. Also, investors use currencies as vehicles to get in and out of risk-taking endeavours. Forced liquidations are increasingly frequent during overstretched markets and a rising yen is unavoidable. Most of all, it is premature to claim the end of the yen’s safe haven. Let’s wait until markets dare to decline by at least 7-10%, before assessing the currency flows.