Year end FX recap Will King Dollar s reign end in 2016

Of course, it’s impossible to write a concise recap of an entire year’s worth of developments in any field, much less the world’s largest market, […]

Of course, it’s impossible to write a concise recap of an entire year’s worth of developments in any field, much less the world’s largest market, […]

Of course, it’s impossible to write a concise recap of an entire year’s worth of developments in any field, much less the world’s largest market, but we wanted to provide at least a 500-foot overview of the major trends that drove FX traders in 2015. As the world’s primary reserve currency, the US dollar is the star of any FX discussion, and that was no different in 2015.

After rocketing higher by over 10% in the first three months of the year, the US dollar index cooled off for the last three quarters, generally holding its ground below the 100 level over that period. Just like an amateur tennis player focused merely on returning his opponents shot (rather than hitting highlight-reel “winners”) can win most games, the dollar’s performance was driven more by other regions dropping the ball rather than stellar performance from the world’s largest economy.

The Federal Reserve did (finally) raise interest rates last month, becoming the first major central bank to embark on a sustainable tightening cycle since the Great Financial Crisis, but relative to the start-of-the-year expectations for a June rate hike, the US central bank was hardly aggressive. However, other major central banks, including the ECB, BOJ, PBOC, BOC, RBA, and RBNZ were all forced to cut interest rates or expand their asset buying programs in 2015, making the US economy and US dollar look like “the best house in a bad global neighborhood” for traders.

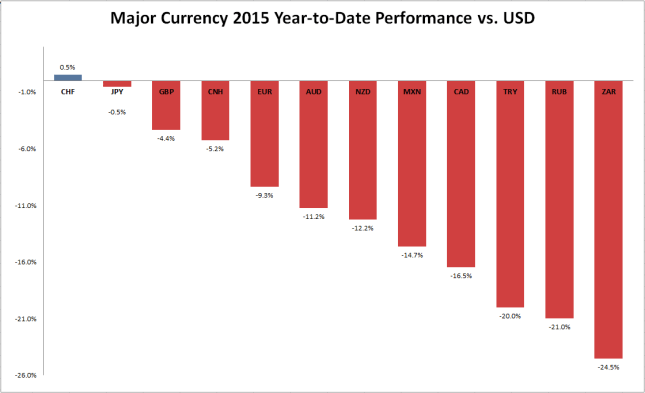

As the chart below shows, the dollar was particularly strong against some of the more fragile emerging market currencies, including the Turkish lira, Russian ruble, and South African rand. Each of these lesser followed currencies had their own idiosyncratic travails in 2015: the lira was hit by consistent political uncertainty and stagflation, the ruble has amidst the persistent weakness in oil, Russia’s most important export, and South Africa’s economy also fell sharply on the back of weakness in commodity prices.

Of the major currencies shown below, only the Swiss franc has gained ground against the greenback. Again, this move was not driven by improving prospects for Switzerland’s economy or currency; instead, the franc rocketed higher in January when the Swiss National Bank decided to stop artificially keeping a lid on its value.

Once again proving that monetary policy is a major driver of currency values, the British pound held up relatively well in 2015. The Bank of England kept interest rates steady at 0.5% throughout the year, the same level they’ve been at since 2009, but did show turn incrementally more hawkish as the UK economy outperformed many of its developed market rivals. The Bank of England looks poised for liftoff at some point in 2016, though uncertainty around a potential “Brexit” (British exit from the European Union) could force the central bank to hold off for longer than it otherwise would like.

Will King Dollar’s reign finally end in 2016?

We’ll be covering the 2016 outlook in more detail for all of these major currencies and markets in the coming weeks, but it’s safe to say that the outlook for the King Dollar in 2016 will depend on the Fed. If the US central bank is able to meet its expectation to raise interest rates four times next year (or even three), the ensuing monetary policy divergence could push the dollar to new heights against its rivals in 2016.

The more likely scenario in our view is that the Fed will only be able to raise interest rates about twice in 2016. As the recent deterioration in FX sensitive areas of the US economy (namely the balance of trade and manufacturing) shows, the elevated value of the US dollar is already starting to weigh on economic activity. The last thing the Fed wants to do is choke out economic growth and the nascent price pressures by raising interest rates too aggressively and therefore may err on the side of caution when it comes to raising interest rates. If this scenario plays out, the dollar’s reign as king of the FX world could come to an end in 2016.