WTI Crude Futures Intraday: Potential Signals of a Correction

WTI Crude Futures (August contract) plunged 5.9% to $38.01 yesterday, as sentiment was dragged down by a resurgence in coronavirus infections across the U.S. and a larger-than-expected build in U.S. crude oil inventory.

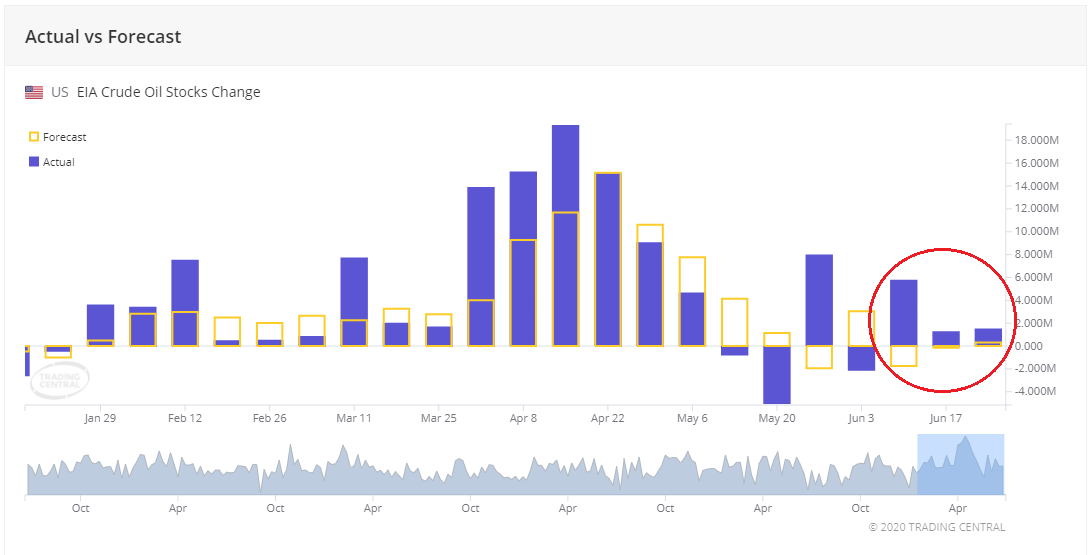

Source: EIA, Trading Economics

The U.S. Energy Information Administration (EIA) reported that crude oil inventory rose 1.44 million barrels, more than an increase of 0.30 million barrels estimated and it is the third consecutive week of worse than expectations.

Previously, we mentioned that despite there might be some more room for oil's rebound in the short term, over-optimism should be avoided. Now there may be signs of a correction in oil prices.

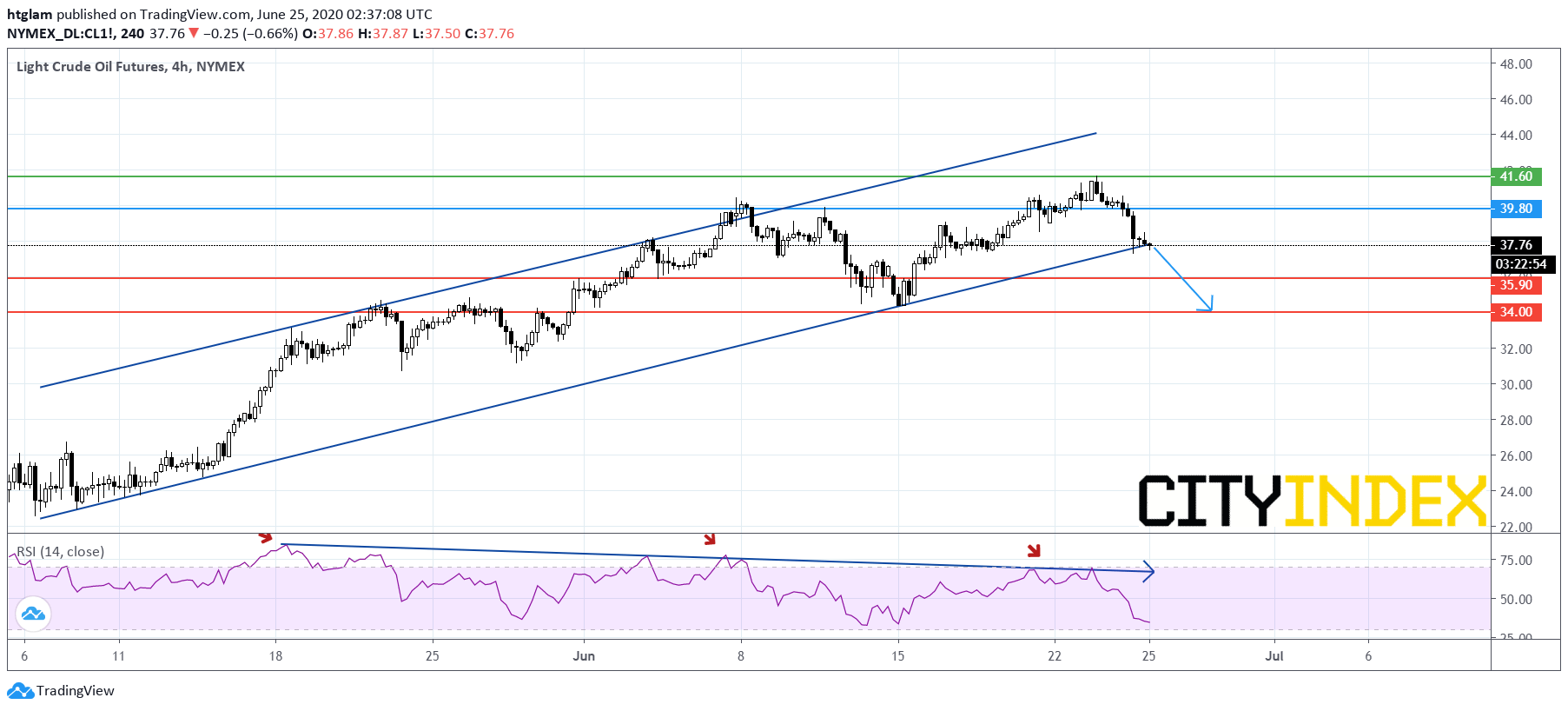

From an intraday point of view, WTI Crude Futures (August contract) is under pressure as shown on the 4-hour chart. There initial signs that a bullish channel drawn from early May might be broken, while the relative strength index continues to show a bearish divergence. Bearish investors might consider $39.80 as the nearest intraday resistance, with prices likely to test the 1st and 2nd support at $35.90 and $34.00 respectively. Alternatively, a break above $39.80 may trigger a revisit to the next resistance at $41.60.

Source: TradingView, Gain Capital

Latest market news

Yesterday 11:09 PM

Yesterday 11:01 PM

Yesterday 04:00 PM

Yesterday 01:15 PM

Yesterday 11:30 AM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM