UK mid-cap outlook remains challenging as investors sharpen focus

All three UK mid-cap stocks reporting results on Wednesday were rewarded with gains, bolstering hopes that laggards could rebound in the second half of the year and lift the FTSE 250 too.

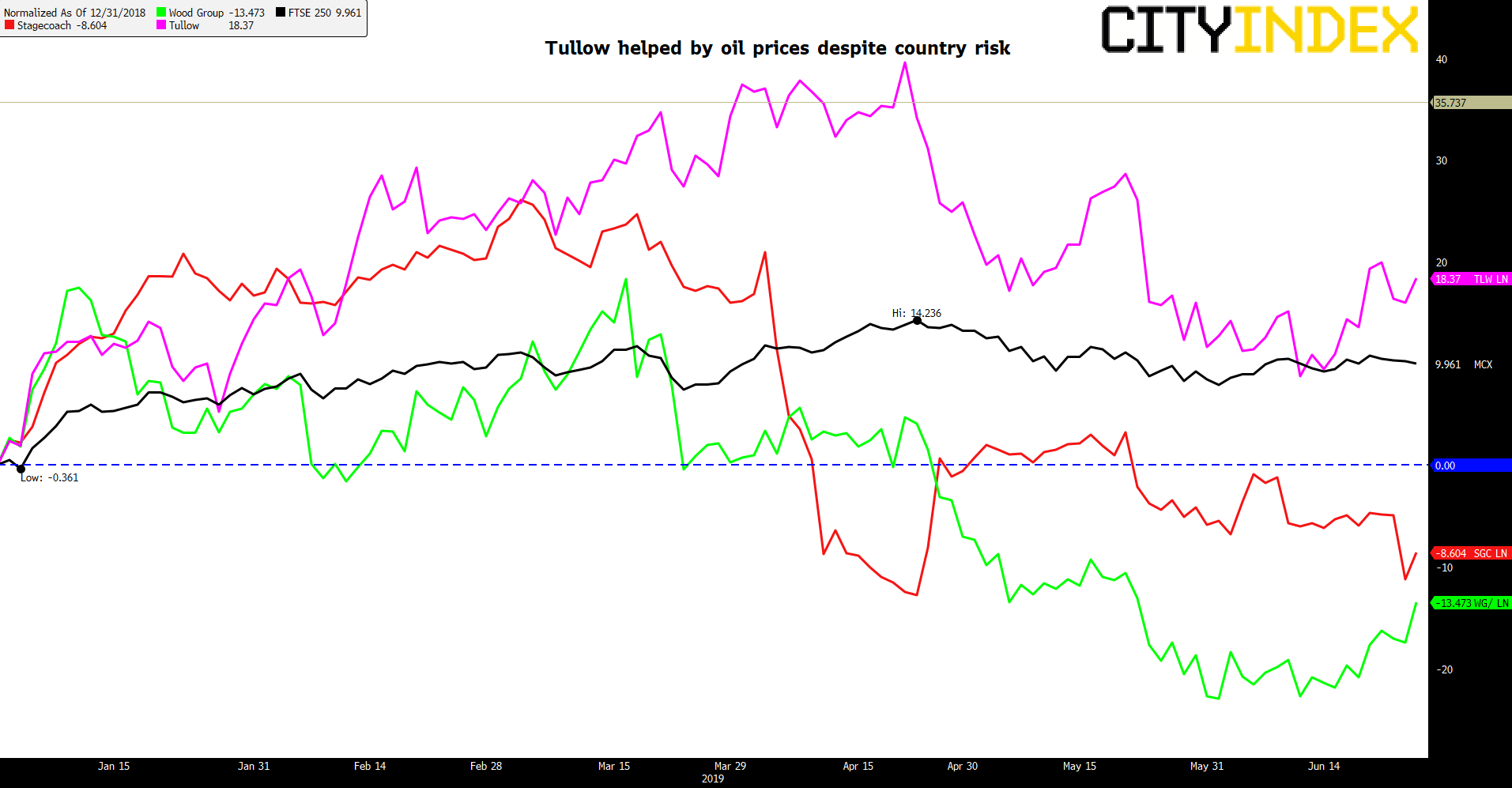

Stagecoach traded as much as 4.5% even after the bus and franchise owner missed full-year revenue and profit forecasts. The UK’s biggest bus and tram operator’s decision not to bid for another domestic rail contract combined with forecast growth in its key UK bus arm helps keep investors on board, for the day at least. The shares have retreated some 9% so far this year, extending a five-year decline to 60%. The long-term decline of Stagecoach’s North America bus unit, disposed of last year, has been compounded by recent disqualification from three British rail routes for prompting withdrawal from a business that has accounted for half its revenue. Profits from continuing operations rose 4% in 2018/19 as revenues collapsed by almost £1bn due to costs for exiting north America bus. It’s possible that exit from loss-making or otherwise problematic businesses to concentrate on the core bus operations can stem the shares’ long decline. Lifting net cash from a 16-year low will remain challenging amid economic and internal uncertainties. SGC could well extend the year’s decline to more than 10% before any recovery

Tullow Oil stock has fared better than the other energy-sector group reporting on Wednesday Wood Group, illustrating disparate sentiment on exploration and production firms compared with oil field services providers. Wood had slumped 19% in 2019 before surging 7% at its best this session, its best one-day rise since April. Investors, who have seen the stock price drain by 40% since 2014, are mostly cheering strengthening signs of a turnaround as margins firm, debt falls and profits for the half-year are expected to advance 25% compared to a year ago. Wood’s non-core disposal programme has helped maintain its cash pile close to £3bn. Net debt is still more than half that at £1.6bn, and almost 4 times last annual core earnings.

Like many producers, Tullow at least had a tailwind from frequent upsurges in the volatile price of oil in recent years. Despite that, a 17% rise this year barely scratches an 80% five-year slump which woefully undershot the FTSE All-Share Oil & Gas index’s 45% gradient. Tullow’s frequent country risk is illustrated again by an overrun of talks with Kenyan authorities. Environmental and Social Impact Assessments will now be submitted in the second half of 2019, “which is later than anticipated”. Despite “significant progress” and “encouraging” steps, a Final Investment Decision in Kenya is now seen in 2020, rather than end-2019. In Uganda Tullow is “considering all options in pursuing the sale of its interests” after failing to finalise agreements with the government. Outstanding investment decisions could essentially cap Tullow shares till at least the end of the year.

The minority of mid-caps reporting today at least provide little guarantee that the FTSE 250 can step up a gear in the medium term. More broadly, with many UK-focused mid-caps theoretically beset by Brexit and sterling concerns, uncertainty can keep the lower-tier market tethered. Like the FTSE 100, it has risen around 10% this year, with most gains in the first half. Our research from a couple of months ago suggests informed investors into UK mid-caps have become even more sharply discriminating, with a select focus on capital goods. By default, their peers are set to be left behind.

Normalised chart: Tullow Oil, Stagecoach, Wood Group – 31/12/2019 to [26/06/2019 14:59:25]

Source: Bloomberg/City Index

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Shares market articles

November 2, 2023 01:41 PM

November 1, 2023 01:33 PM

October 31, 2023 01:15 PM

October 31, 2023 10:24 AM