Will there be another Ruble rout

Back in Jan/ Feb the Ruble was under attack, USDRUB reached a record high of nearly 80.00, causing intervention from Russian officials and hasty rate […]

Back in Jan/ Feb the Ruble was under attack, USDRUB reached a record high of nearly 80.00, causing intervention from Russian officials and hasty rate […]

Back in Jan/ Feb the Ruble was under attack, USDRUB reached a record high of nearly 80.00, causing intervention from Russian officials and hasty rate hikes to stem the decline in the currency. Things calmed down for the RUB over the next few months, however, it started to drift higher in June, as US dollar strength gathered pace, and the RUB has been the worst performer in the emerging market FX space this week.

The sharp 3% fall in the RUB on Friday was triggered by the 50 basis point cut in interest rates by the Russian central bank. The central bank has been cutting rates in recent months to erode the negative economic effects of hiking rates to 17% at the start of the year to halt the previous slide in the RUB.

Why cut rates?

The decision to cut rates again today comes on the back of weak economic data, wages have been falling, retail sales are slumping and business investment is at a 6 year low. Q1 GDP slumped by 2.2%, and the future does not look good for growth for the rest of this year.

The central bank has had to weigh up the risks of cutting interest rates to try and boost the economy, with the weakening RUB and rising inflation. For now growth seems to be the bigger priority, as inflation is currently an eye wateringly high 15.3%, which hasn’t been helped by the decline in the currency.

Russia bucks the trend:

Interestingly, the Russian authorities have bucked the trend by cutting rates, after Brazil hiked the Selic rate by 50 basis points to 14.25% earlier this week to stem the decline in BRL. The rate hike has helped to stem USDBRL strength, but the impact has been limited so far and there could be pressure on the Brazilian authorities to step back in to the market and prop up the BRL in the coming weeks.

Where does this leave Russia?

If we continue to see RUB weakness then we think that the Russian authorities may have no choice but to reverse its recent dovish stance and start hiking interest rates once more. As we mentioned, the RUB has been the weakest performer in the emerging market FX space this week and we expect the decline to continue. The RUB could get punished further for the Bank of Russia’s unwillingness to follow the lead of countries like Brazil and support its currency.

The RUB faces the same pressures as it did back in January: the prospect of a Fed rate rise making Russia’s external debt load more expensive, and a lower oil price threatening the long term economic health of the country. With Brent crude prices back at April levels, the latter point remains a major cause of concern, and if the Fed does hike rates in September then it could add even more downward pressure to the RUB.

The technical view:

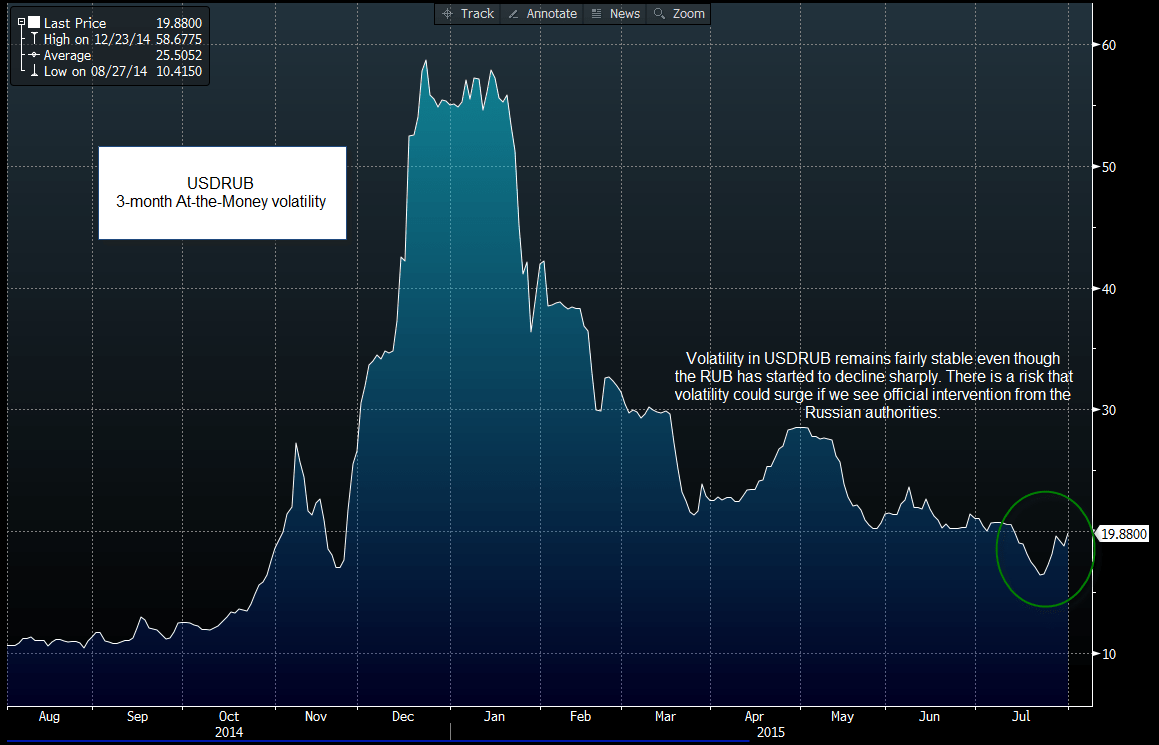

Interestingly, USDRUB volatility has managed to stay fairly stable around the 20 mark during this latest bout of RUB weakness (see figure 1). This could be because the market for USDRUB options is fairly quiet, however we would expect volatility to pick up sharply in the coming days and for the price of protection against further RUB declines to rise.

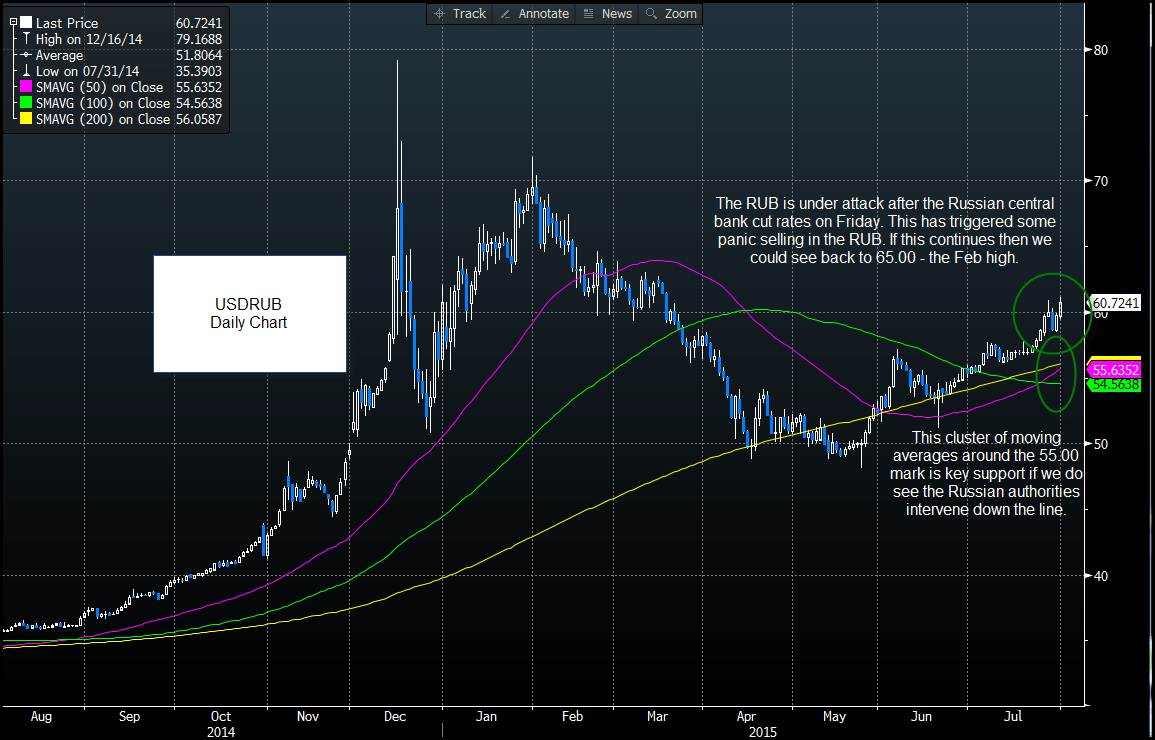

From a technical perspective, USDRUB is already above the major moving averages, and momentum seems to be on the side of the RUB bears. The daily range in USDRUB widened sharply in recent days, which suggests that there could be further downside for the RUB. When there is a risk of panic selling in a currency, it is worth looking for the big psychological levels that may slow down the decline. For USDRUB that includes 65.00 – the high from 23rd Feb, and then 70.00 – the 2nd Feb high.

As we mention above, if we continue to see the RUB decline then the risk of official intervention increases. If the Russian authorities step into the market and buy RUB or the central bank reverses course and starts hiking interest rates (the latter is more likely in our view), then we could see a sharp short-term relief rally in RUB, back to the 55.00 area – a cluster of simple moving average support (as you can see in figure 2).

Takeaway:

Figure 1:

Source: City Index Data: Bloomberg

Figure 2:

Source: City Index Data: Bloomberg