October 1, 2019 2:27 AM

The month of October is upon us, a month that carries a reputation for delivering elevated volatility, largely courtesy of the 1987 stock market crash.

In 2018, October’s reputation for volatility was further enhanced as surging U.S. yields triggered a +20% fall in the S&P 500 and other global equity markets. A fall that forced several the worlds key central banks to flip from a hawkish flight path to a dovish path and which culminated in the RBA slashing interest rates today, for the third time in 2019.

As was the case in early October 2018, the S&P 500 is currently trading near to all-time highs. However, there are some key differences in 2019.

1. After an unrelenting flow of mixed signals emanating from the U.S. – China trade dispute, including the latest instalment overnight as U.S. officials denied they planned to block Chinese listings on U.S. exchanges, markets have become somewhat desensitized.

This may also explain why last week’s political dramas on both sides of the Atlantic including the Democrats opening an impeachment inquiry into President Trump and the UK Supreme Court ruling that PM Boris Johnsons suspension of parliament was unlawful, failed to have a lasting impact.

2. Interest rates are at extremely low levels and this makes stocks significantly more attractive.

3. The prospect of fiscal stimulus is rising in countries including Europe and Australia.

Whether the three points of difference above are enough to ensure the S&P500 remains Teflon coated during October 2019 remains to be seen.

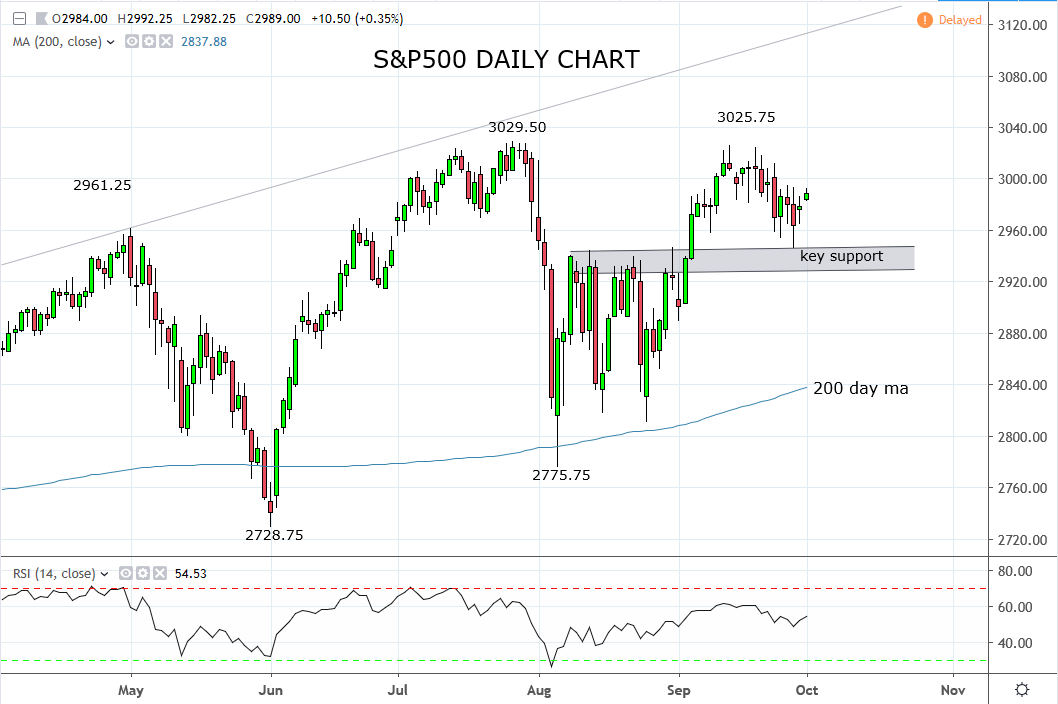

From a technical point of view, we are open-minded keeping an eye on two possibilities with vastly different implications.

The bullish case: Should the S&P 500 break and close above the July 3029.50 high without first falling through the key near term 2940/30 support region, it would suggest a rally towards 3100/50 is underway for a Wave V.

The bearish case: Should the S&P 500 break and close below the key near support at 2940/30 without trading above 3030 beforehand, it would open the way for a deeper pullback towards 2770 to commence.

Source Tradingview. The figures stated are as of the 1st of October 2019. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Disclaimer

TECH-FX TRADING PTY LTD (ACN 617 797 645) is an Authorised Representative (001255203) of JB Alpha Ltd (ABN 76 131 376 415) which holds an Australian Financial Services Licence (AFSL no. 327075)

Trading foreign exchange, futures and CFDs on margin carries a high level of risk and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to invest in foreign exchange, futures or CFDs you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss in excess of your deposited funds and therefore you should not invest money that you cannot afford to lose. You should be aware of all the risks associated with foreign exchange, futures and CFD trading, and seek advice from an independent financial advisor if you have any doubts. It is important to note that past performance is not a reliable indicator of future performance.

Any advice provided is general advice only. It is important to note that:

- The advice has been prepared without taking into account the client’s objectives, financial situation or needs.

- The client should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation or needs, before following the advice.

- If the advice relates to the acquisition or possible acquisition of a particular financial product, the client should obtain a copy of, and consider, the PDS for that product before making any decision.