The ECB is due to make its monetary policy announcement on Thursday 10th December at 12:45 GMT.

Expectations are running high after Christine Lagarde already pre-committed to additional easing in the October meeting. €500 billion in QE purchases and extremely generous loans to banks are widely expected and priced in. Sinking to the Euro could take a lot more.

Why ease?

In light of second national lockdowns in the likes of France and Germany the reasons for easing monetary policy further are clear; growth appears to be struggling in the final quarter. PMIs have pointed to resilience in the manufacturing sector however, the service sector has tumbled deep into contraction over the quarter. The composite PMI which gauges business activity across the service & manufacturing sector has also contracted each month since September.

In light of second national lockdowns in the likes of France and Germany the reasons for easing monetary policy further are clear; growth appears to be struggling in the final quarter. PMIs have pointed to resilience in the manufacturing sector however, the service sector has tumbled deep into contraction over the quarter. The composite PMI which gauges business activity across the service & manufacturing sector has also contracted each month since September.

The ECB’s previous forecast of 3% QoQ growth in Q4 now looks overly optimistic. A significant downward revision is expected. That said the latest vaccine developments could see an upward revision to H2 GDP 2021.

Lackluster inflation has been a headache for the ECB and is expected to remain weak going forwards, which is only aggravated further by the supercharged Euro.

EUR strength in focus

With the EUR pushing higher even though the ECB are set to ease it could be difficult for the central to reverse the current EUR/USD uptrend despite. The bearish bias on the US Dollar is proving to be too strong. In fact there could be a bigger risk of the ECB under delivering in the press conference by way of a weak forward guidance past December, which could well lift the common currency.

The meeting comes as the Euro has been hovering around 32 month highs. However, the trade weighted EUR trades around its 2009 peak. A strong currency can not only restrict economic growth but can also hold back inflation and with disinflation of -0.3% the ECB could do without a strong Euro.

With the EUR pushing higher even though the ECB are set to ease it could be difficult for the central to reverse the current EUR/USD uptrend despite. The bearish bias on the US Dollar is proving to be too strong. In fact there could be a bigger risk of the ECB under delivering in the press conference by way of a weak forward guidance past December, which could well lift the common currency.

The meeting comes as the Euro has been hovering around 32 month highs. However, the trade weighted EUR trades around its 2009 peak. A strong currency can not only restrict economic growth but can also hold back inflation and with disinflation of -0.3% the ECB could do without a strong Euro.

Over-delivering?

If the central bank is looking to pull down the Euro an above consensus QE purchase of €750 billion or even a rate cut could do the job. However recent commentary suggests that the ECB isn’t there yet.

Let’s not forget that a deep divide between the ECB doves and hawks is likely to prevent the central bank from over delivering.

Market reaction

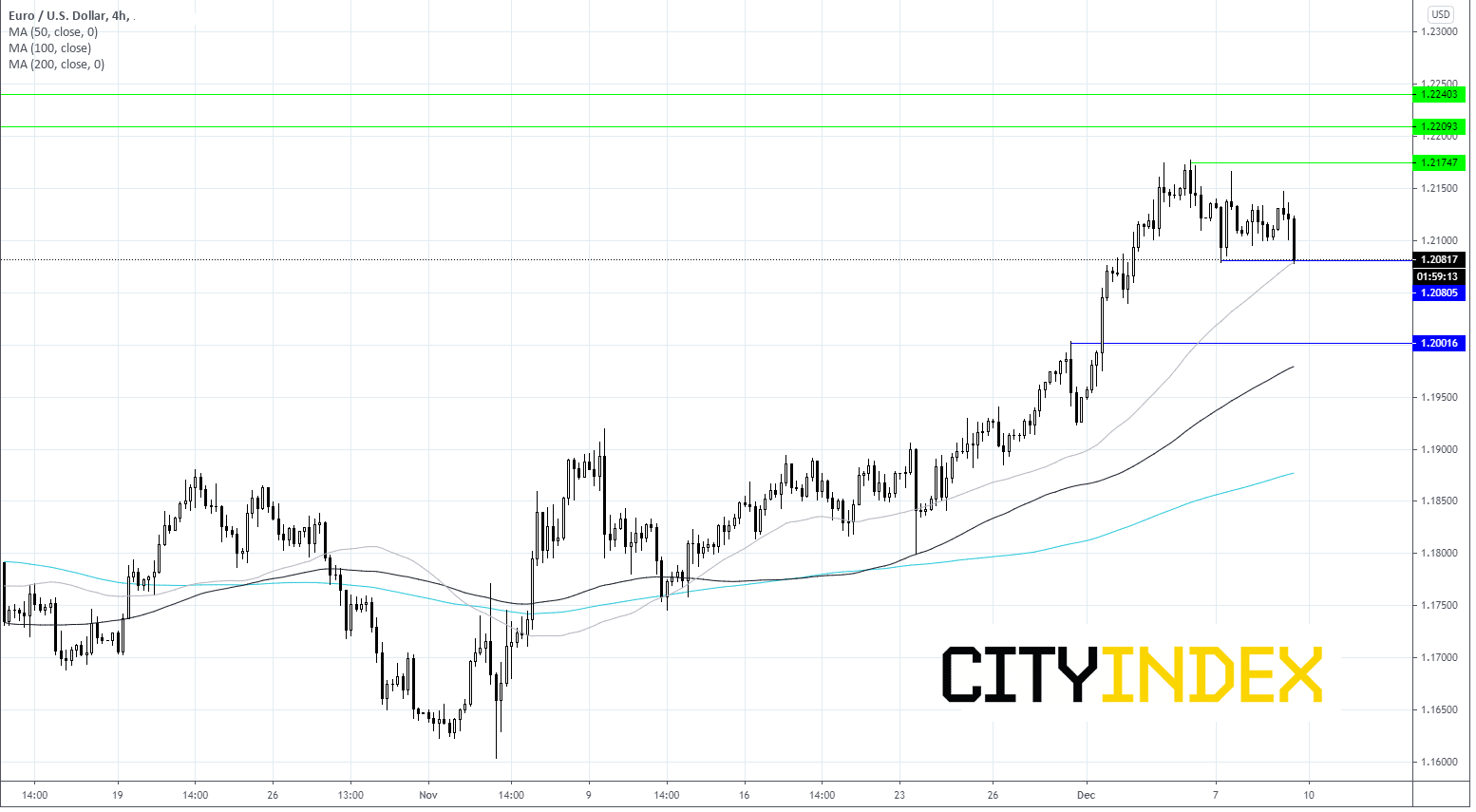

If the market is disappointed by what he ECB brings then the Euro could push higher. Any spike higher could struggle at $1.2175 resistance, a break beyond here could bring $1.2210 into the picture.

However, if Lagarde gets her way and manages to overdeliver near term support can be seen at $1.2080 50 sma & horizontal support prior to $1.20 round number.

Latest market news

Today 04:00 PM

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest EUR articles

April 13, 2024 08:00 PM

March 25, 2024 02:55 AM

January 22, 2024 04:19 AM

January 18, 2024 04:46 AM