October 16, 2019 2:00 AM

A strong rally in equity markets overnight following a good start to the Q3 U.S. reporting season, soothing tones from Chinese media channels over the trade truce and optimism that an end to Brexit is near, has been tempered this morning after reports the U.S. House passed a bill to support protesters in Hong Kong.

This comes just two days after Chinese President Xi issued a warning that independence advocates anywhere in China would be opposed and “end in crushed bodies and shattered bones.” The tension over Hong Kong serves as a reminder that China – U.S rivalry extends across many spheres including trade, intellectual property, and human rights.

No surprises then that USDJPY has fallen this morning from 108.90 back to 108.60. That said there are several reasons why I favour buying dips in USDJPY outlined below.

- As mentioned in previous notes, USDJPY generally displays a positive correlation with U.S. 10-year yields. My expectation is for U.S. 10-year yields to rally back towards 2.00% in coming weeks.

- There remains 15bp of a 25bp rate cut priced for the October FOMC meeting in just under 2 weeks’ time. A solid retails sales number in the U.S. this evening should support a further unwind of rate cut pricing.

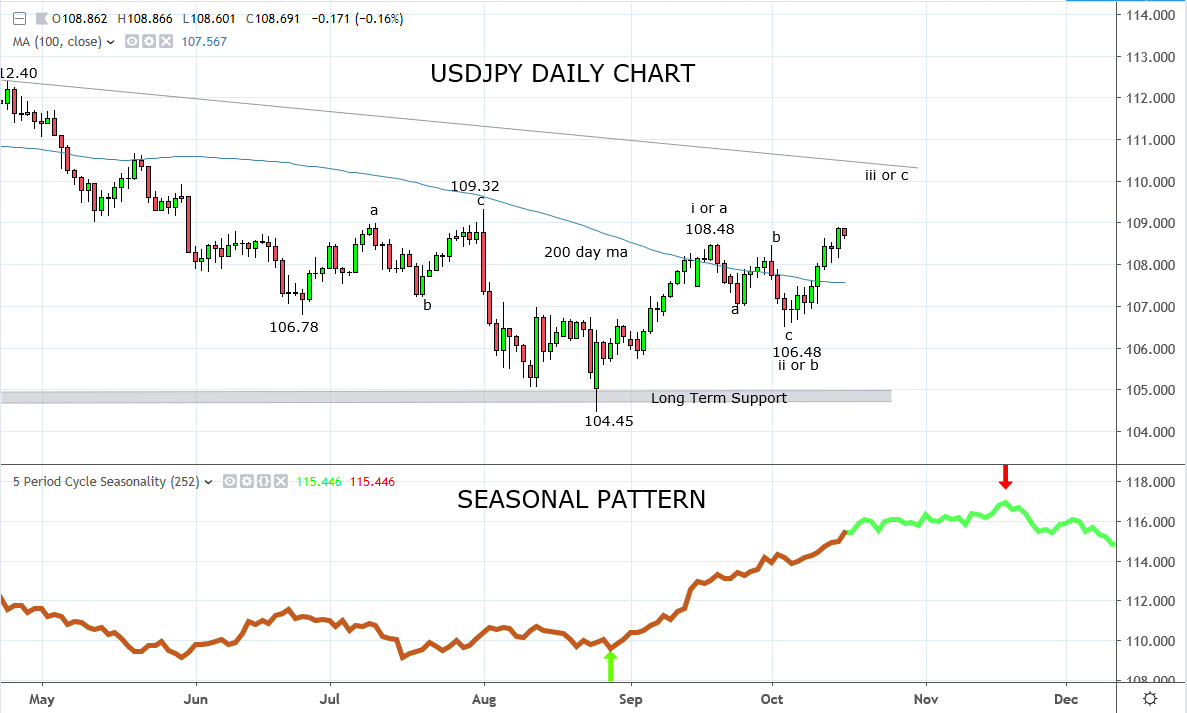

- USDJPY exhibits a seasonal tendency to rally from August into September as viewed on the chart below.

- Portfolio outflows and a tendency towards greater unhedged foreign bond investment by Japan’s Government Pension Investment Fund (GPIF), the world’s largest pension fund is supportive of USDJPY.

- The market remains short USDJPY.

- Technically, the price action from the 108.48 high on the 18th of September to the October 106.48 low appears to be a corrective pullback. After breaking above the 108.48 double high last Friday, there is potential for USDJPY to extend its recent rally towards 109.30 and then 110.30.

In summary, dips in USDJPY towards the recent double high 108.50 area, are likely to find support. Stops should be placed below 106.50, looking for a move towards 110.30/50.

Source Tradingview. The figures stated are as of the 16th of October 2019. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Disclaimer

TECH-FX TRADING PTY LTD (ACN 617 797 645) is an Authorised Representative (001255203) of JB Alpha Ltd (ABN 76 131 376 415) which holds an Australian Financial Services Licence (AFSL no. 327075)

Trading foreign exchange, futures and CFDs on margin carries a high level of risk and may not be suitable for all investors. The high degree of leverage can work against you as well as for you. Before deciding to invest in foreign exchange, futures or CFDs you should carefully consider your investment objectives, level of experience, and risk appetite. The possibility exists that you could sustain a loss in excess of your deposited funds and therefore you should not invest money that you cannot afford to lose. You should be aware of all the risks associated with foreign exchange, futures and CFD trading, and seek advice from an independent financial advisor if you have any doubts. It is important to note that past performance is not a reliable indicator of future performance.

Any advice provided is general advice only. It is important to note that:

- The advice has been prepared without taking into account the client’s objectives, financial situation or needs.

- The client should therefore consider the appropriateness of the advice, in light of their own objectives, financial situation or needs, before following the advice.

- If the advice relates to the acquisition or possible acquisition of a particular financial product, the client should obtain a copy of, and consider, the PDS for that product before making any decision.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Forex articles

Yesterday 11:00 AM

April 23, 2024 11:09 PM

April 23, 2024 04:00 PM