Why currency wars may be on the back burner

President Trump has a lot on his plate at the moment, from finding a new security advisor to batting off claims he knew about General […]

President Trump has a lot on his plate at the moment, from finding a new security advisor to batting off claims he knew about General […]

President Trump has a lot on his plate at the moment, from finding a new security advisor to batting off claims he knew about General Flynn’s contact with the Russians before he became a formal member of team Trump. One thing he may want to put on the back burner while he deals with this developing storm are his threats to label China a currency manipulator.

China goes with the dollar’s flow

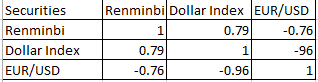

The table below shows a simple correlation analysis of the dollar index, the Chinese renminbi (spot), and the EUR/USD. The results make for very interesting reading. This analysis uses weekly correlations over the past year, and found that the Chinese renminbi and the dollar have a strong positive correlation of 0.79. This means that over the past year the renminbi has moved in line with the USD nearly 80% of the time. Even if you switch to daily correlation analysis, which is more volatile, the renminbi moved alongside the US dollar 63% of the time, which is still significant.

Can President Trump justify calling China a currency manipulator?

This analysis could weaken President Trump’s argument that China is manipulating its currency. Even though the renminbi has fallen some 6% versus the USD in the past year, the fact that it has been roughly tracking the USD, even though the dollar has had a stronger performance, suggests that the Chinese authorities are not actively trying to weaken the renminbi vs. the USD.

In contrast, this analysis could support Trump’s criticism of Germany. The euro has moved in the opposite direction vs. the US dollar 96% of the time over the past 12 months. This has corresponded with an uptrend in the dollar and a profound downtrend in the euro.

Germany can’t stop the euro weakening

But, the devil is in the detail, and this is where Trump’s argument gets stuck. Germany does not manipulate the euro, and doesn’t even set monetary policy for the currency bloc, that is down to the ECB. Also, political risk and weak growth across the currency bloc have contributed to the euro’s recent demise, which, again, is essentially out of Germany’s control.

In contrast, the Chinese authorities actively manage the renminbi, but have loosened the reigns recently, and have allowed the renminbi to more closely track the US dollar. To highlight this, in 2014, the renminbi had no significant correlation with the dollar index.

Currency wars no threat to risk sentiment

So what does this all mean? After lashing out at Germany, who run a trade surplus with the US as well as a weak currency, Trump did not label Japan a currency manipulator when he met Japanese PM Abe at the weekend, even though Japan also has a trade surplus with the US and actively tries to weaken its currency through a loose monetary policy.

This is significant, as problems start to boil over at home, Trump may abandon his plans to talk down the dollar and label those with weaker currencies than the US currency manipulators. This could put the threat of currency wars on the back-burner for now, which is positive for risk sentiment.

Figure 1: CNY/ DXY/ EUR/USD weekly currency matrix

Source: City Index