September 21, 2020 1:05 AM

Based on the strong evidence of this relationship, it would be fair to think that the reverse should also be true and that if U.S. stock markets fall, the AUDUSD should also fall.

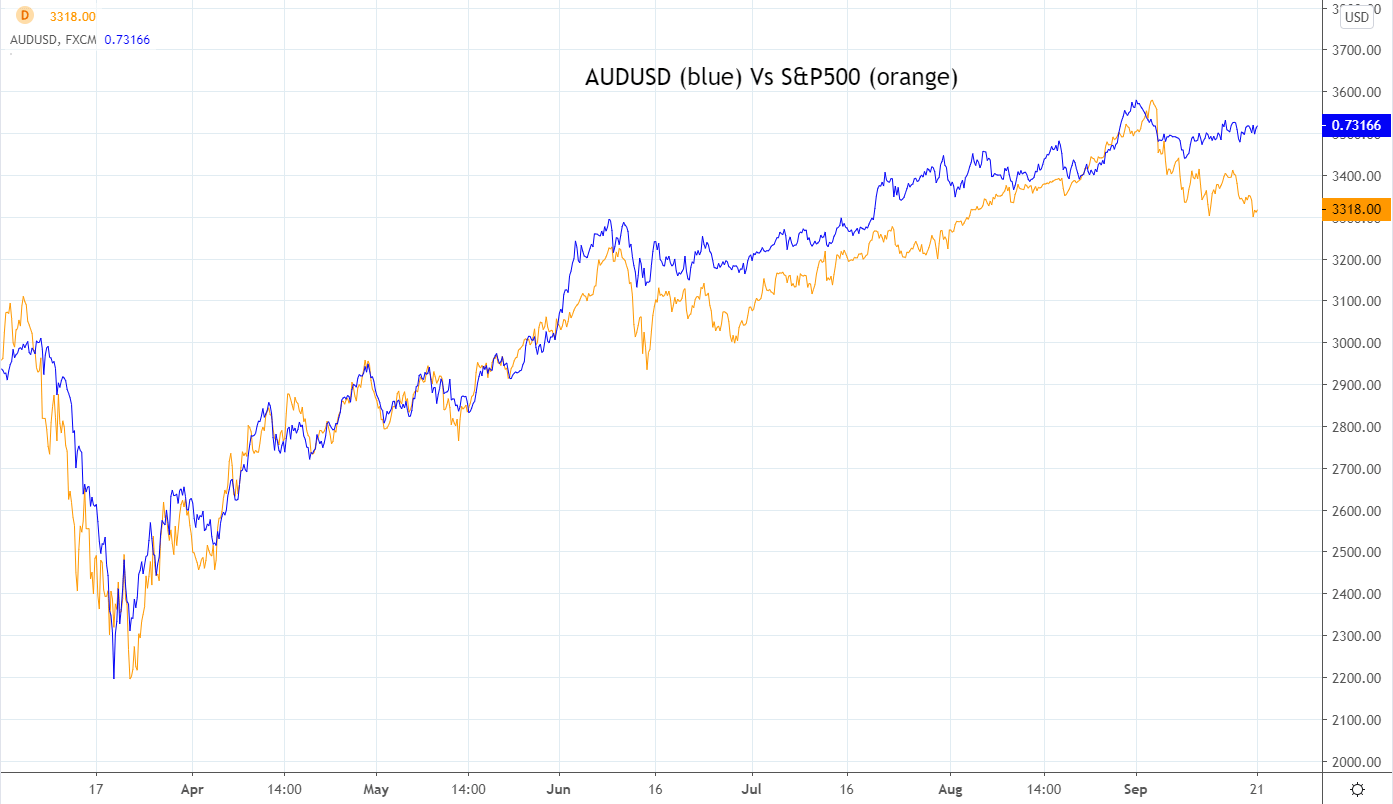

However, as the chart below shows, the AUDUSD remains just 1.5% below cycle highs, content to ignore this month’s -7.5% fall in the S&P500. A simple extrapolation of the price action from earlier in the year, suggests the AUDUSD should in theory be trading about 150 pips lower, near .7150.

Not only did the AUDUSD ignore the S&P500’s stumble in September, IMM positioning data released over the weekend reveals that speculative accounts increased their existing long AUDUSD position from 10.9k contracts to 28.6k contracts.

When looking for reasons why this occurred, it’s important to remember the price of Australia’s largest export iron ore remains buoyant, trading at above U.S $120.00 per tonne. Copper another key export of Australia is trading at 2-year highs, supported by a plunge in LME copper inventory, to its lowest level since 2005.

Elsewhere economic data in Australia during September has been much better than expected including strong consumer and business confidence numbers and the August jobs data released last week.

Reflecting the better data, the economics team at CBA have this morning revised higher their forecast for Australian GDP. Q3 2020 GDP has been revised higher from 0% to +2.0% while GDP for 2020 is expected to fall by -3.3% vs the previous estimate of -4.3%.

Technically, the correction from the .7415 high, now entering its fourth week has up until this point been unremarkable.

Providing the AUDUSD remains above trendline support .7250/30ish, the uptrend remains intact and keeps open the possibility of a retest of the .7414 high, before .7500c.

However, a break/close below support .7250/40 would warn of a retest of the recent .7192 low, before .7130, and possibly as deep as .7075/65.

Source Tradingview. The figures stated areas of the 21st of September 2020. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest AUD articles

April 24, 2024 06:51 AM

April 24, 2024 02:03 AM

April 22, 2024 10:40 PM

April 16, 2024 12:44 AM