When will Adobe release Q3 results?

Adobe will release third quarter earnings after US markets close on Tuesday September 21.

Adobe Q3 earnings preview: what to expect from the results

Adobe has found itself flourishing as businesses digitally transform themselves and move more of our day-to-day lives online. The pandemic has caused an accelerated digital shift and resulted in greater demand for Adobe’s creative, marketing and analytics software.

Heading into the third quarter of its financial year, Wall Street is expecting Adobe’s annual revenue to jump 21% in the year to the end of November compared to the 15% increase reported last year – putting it on course to deliver another set of record full year earnings.

As for the third quarter, Adobe has said it is targeting $3.88 billion in revenue and diluted EPS of $2.27. Analysts are expecting the firm to beat those targets with forecasts that quarterly revenue will rise to $3.89 billion from $3.22 billion the year before, with diluted EPS forecast to rise to $2.29 from $1.97. Notably, Adobe has beaten expectations for eight consecutive quarters.

Analysts anticipate Adobe’s Digital Experience division will report revenue growth of over 25% year-on-year in the third quarter, accelerating from 21% in the second. The unit provides a range of apps and tools for businesses to manage their customer’s experience, covering everything from insights and content to engagement, and is more exposed to the economic recovery as businesses bounce back from the pandemic and speed up their digital transformations.

That should counter a slowdown in growth from its larger Digital Media division that homes the likes of its creative and digital documents software. Having delivered 25% topline growth in the last quarter, markets are anticipating this will come in closer to 20% in the third.

There is an expectation that Adobe’s profitability, which benefits from higher margins thanks to its subscription-based model, could come under mild pressure this quarter as it raises spending on marketing and hiring new staff.

Adobe shares currently trade at just under $650 per share, hovering near the all-time high of $673 it achieved last week after rallying by over one-third since the start of 2021. The 29 brokers covering Adobe have an average Buy rating on the stock but only see 1.6% potential upside from the current average target price of $662.62. Notably, the most recent upgrades made over the last two weeks have resulted in significantly higher target prices of late. Mizhuo raised its target to $695 from $640, BMO upped its target to $730 from $630, Stifel to $725 from $675 and Goldman Sachs $735 from $665.

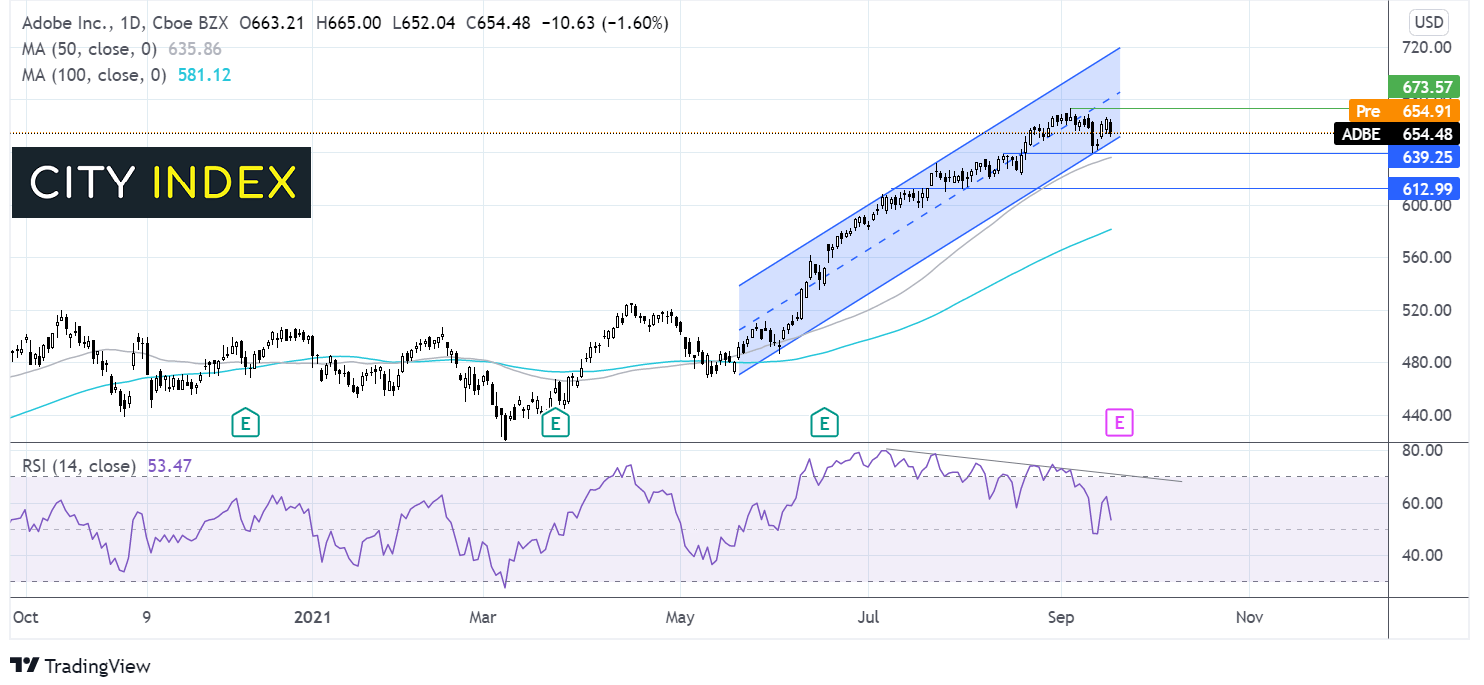

Where next for the Adobe share price?

Adobe share price has been trending higher within a rising channel since late May. The price reached an all time high of $673 on September 7 and has been consolidating since. Whilst the stock remains above $650 and in the rising channel potential remains for $673 to be reached again and fresh record highs achieved.

However, the bearish RSI divergence suggests that momentum is slowing. A break below $640 / $635 contention zone comprised of Septembers low and the 50 sma could negate the near term uptrend and see the sellers gain traction towards $610 a level which offered resistance in July and support in early August.

How to trade Adobe shares

You can trade Adobe shares with City Index in just four easy steps:

- Open a City Index account, or log-in if you’re already a customer.

- Search for ‘Adobe’ in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM