May 11, 2022 10:24 AM

Heading into tonight’s crucial CPI data, gold is trading lower for a fourth consecutive week and has lost ~ 8% from its April 18, $1999 high.

After topping in early March at $2070 after the Russian invasion of Ukraine, the decline in gold accelerated in mid-April after a stream of hawkish Fed Speakers raised expectations of a more aggressive hiking cycle.

While there was initial relief after the May FOMC that Fed Chair Powell downplayed the possibility of a 75bp rate hike, he did pre-signal two inflation-busting 50bp rate hikes at the upcoming FOMC meetings in June and July.

The Fed’s more aggressive super tightening cycle, which is expected to take the Feds Fund target back above 3% by early year, has undermined the value of gold for two key reasons outlined below.

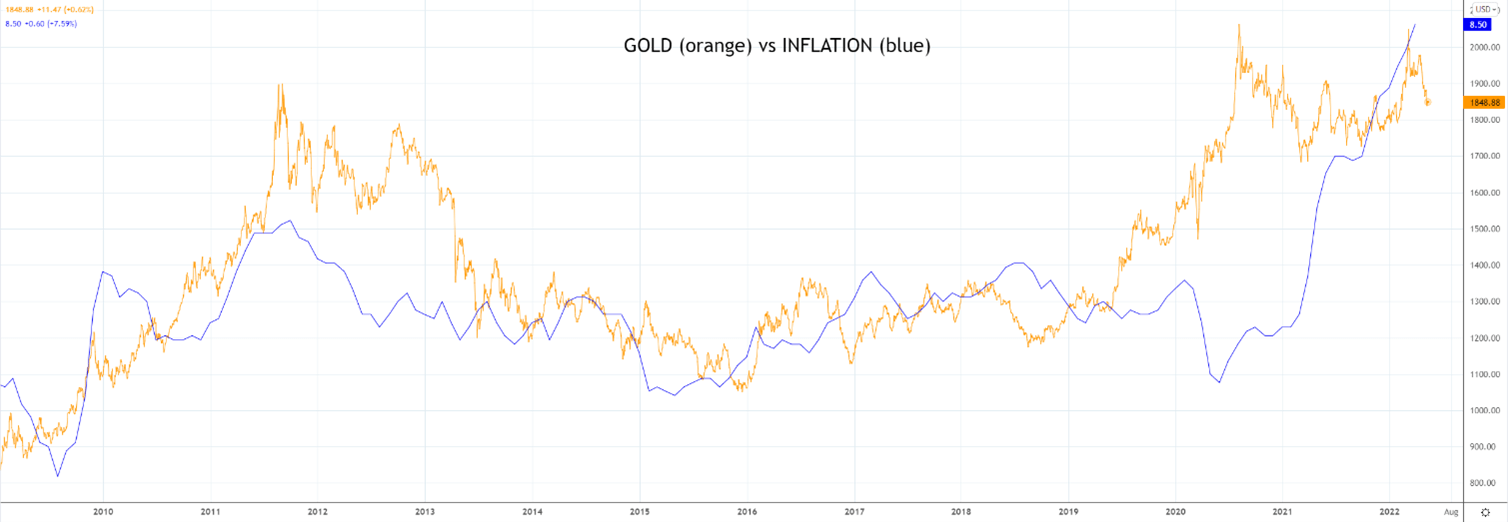

Peak inflation

Gold is viewed as an inflation hedge to protect against the debasement of fiat currencies. As can be viewed on the chart below, both inflation and gold have rallied in tandem until recently.

Gold has turned lower, likely pre-empting a slowdown in inflation as early as this evening’s U.S CPI print. Headline inflation for April is expected to slow to an annual rate of 8.1%, down from a 40 year high of 8.5% in March. The core inflation rate is expected to fall from 6.5% to 6%.

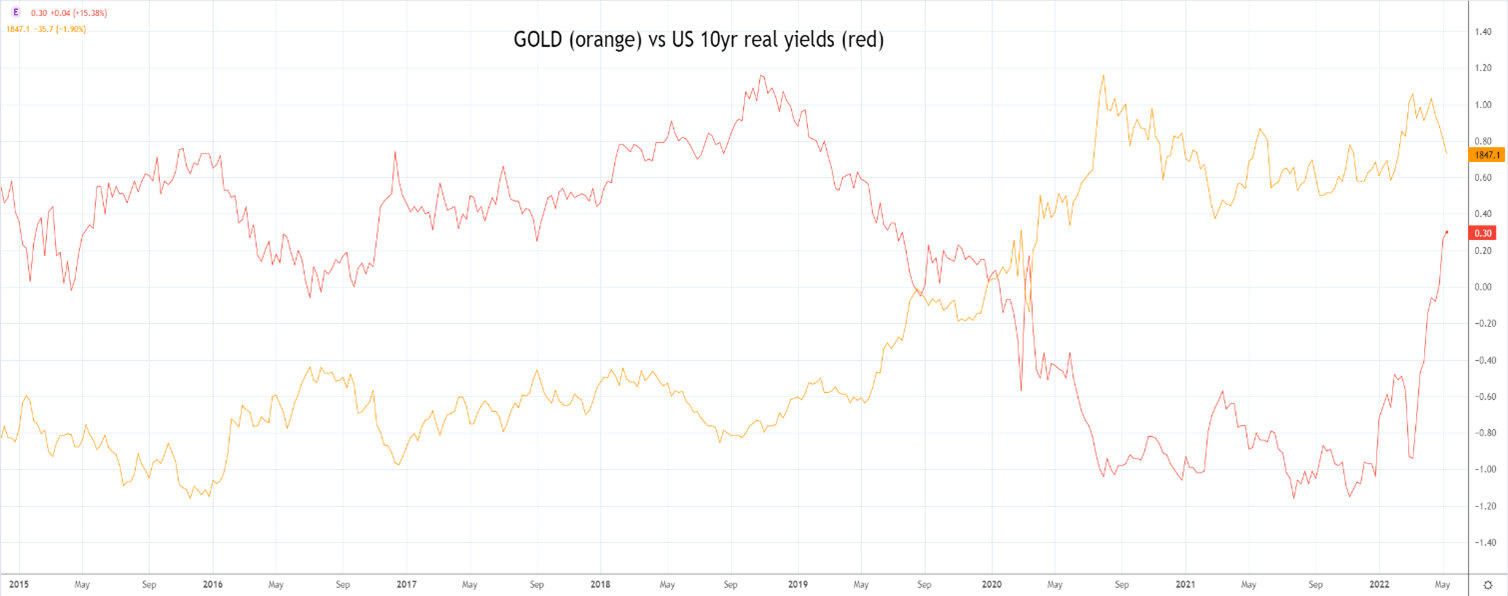

Positive U.S real yields

In late November, the renomination of Fed Chair Powell over Fed Governor Lael Brainard was considered a hawkish development and the catalyst for real yields to move away from the deeply negative levels of early November (-117bp).

Overnight, U.S. 10-year real yields (the interest rate adjusted for inflation) closed at +30 points. It is noticeable that the downside move in gold accelerated in mid-April as real yields moved from negative into positive territory.

Positive real yield undermines demand for gold because gold yields nothing. Real yields are expected to continue to move higher while the Fed maintains its hawkish stance.

What do the charts say?

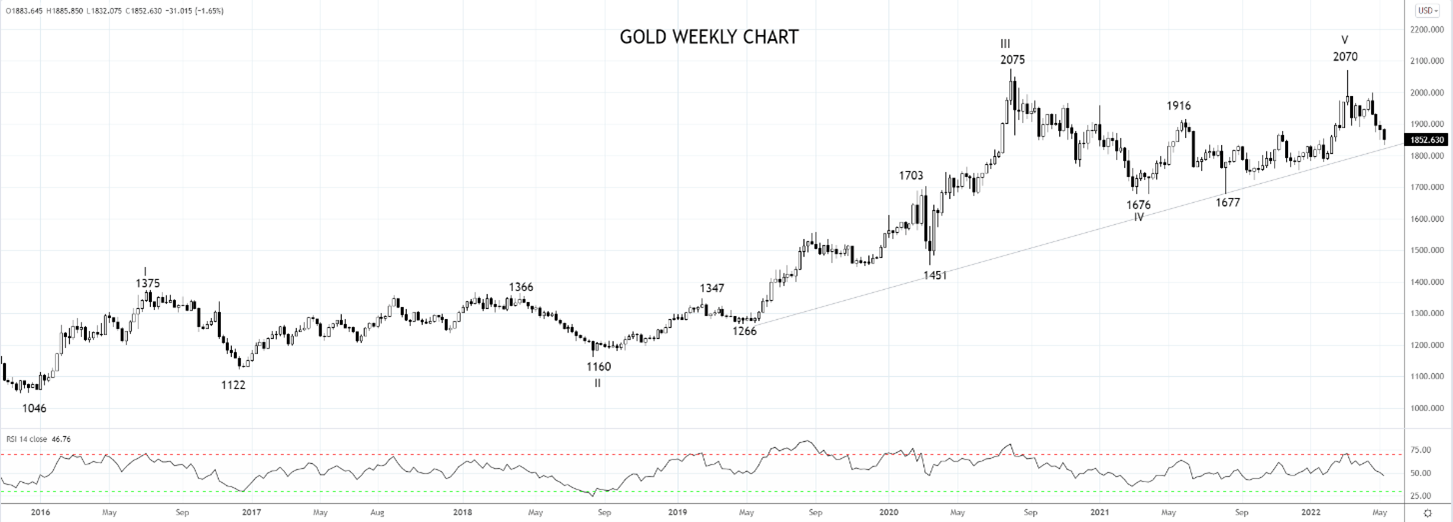

In an article on March 18 here we described the reversal pattern from the $2070 high as “tweezer/double top that could turn out to be one for the ages.” It is also noticeable gold completed an Elliott Wave five wave advance from the $1046, 2015 low.

The ensuing pullback has seen gold slip towards weekly uptrend support near $1830/20. This level is likely to provide initial support. However, if gold does see a sustained break below $1820ish the risks are for a deeper pullback towards range lows $1700/$1670 into year-end.

Source Tradingview. The figures stated are as of May 11, 2022. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the company you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Today 08:15 AM

Today 05:45 AM

Yesterday 11:09 PM

Latest Gold articles

Yesterday 11:30 AM

Yesterday 03:18 AM

April 22, 2024 10:48 PM

April 22, 2024 03:42 AM