June 3, 2021 3:59 PM

What is driving the US Dollar higher?: DXY

The US Dollar Index (DXY) was on a tear today. The US session began with the DXY selling off after Russia announced that they were exiting US Dollars from their Sovereign Wealth Fund. However, that move later reversed, and the DXY turned sharply higher with a better than expected ADP Employment Change figure for May, as well as, with a better than expected initial Jobless Claims figure for the week ending May 29th. Expectations for tomorrows Non-Farm Payrolls for May are +645,000. ( See Matt Weller’s complete NFP Preview HERE). But if good jobs numbers mean a stronger economy, wouldn’t that mean stronger stocks and a weaker US Dollar?

By now you know the story: better data means there is more of a chance that the Fed may do more than just “Talk about talk about tapering”. The worry is that with a better print, the Fed will announce tapering at their June meeting in 2 weeks. Tapering, or decreasing their $120 billion of bond purchases per month, would mean lower bond prices and higher yields. In addition, less support from the Fed would also mean lower stock prices and a higher DXY.

However, the risk for the NFP print is twofold:

1) it is weaker than expected

2) there is a large revision from the horrible April print (+266,000)

We also need to pay attention to the average hourly earnings figure. With higher inflation data lately, the Fed will want to make sure that inflation is feeding through to the employment data before they do anything. They have consistently said that they want to see a string of months of improvement in the labor market, which includes increases in pay. Expectations are 0.2% for May.

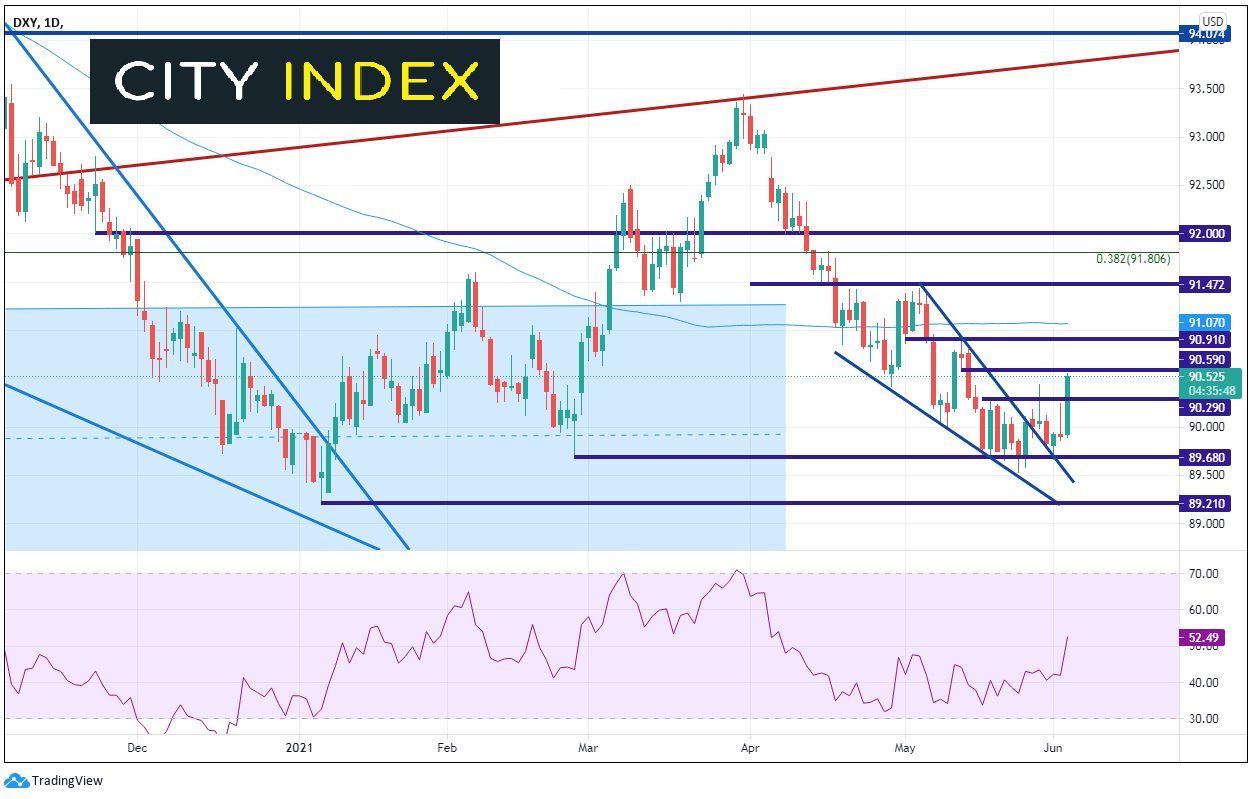

After moving lower for most of 2020, DXY bounced for almost the entire first quarter of 2021. Thus far in the second quarter, the DXY has been moving lower. After hovering around the 200 Day Moving Average near 91 at the end of April/beginning of May, price continued lower in a descending wedge formation. Price broke above the wedge on May 27th, and today, finally accelerated higher away from the wedge. The DXY traded to horizontal resistance today near 90.59.

Source: Tradingview, City Index

What is the US Dollar Index (DXY)?

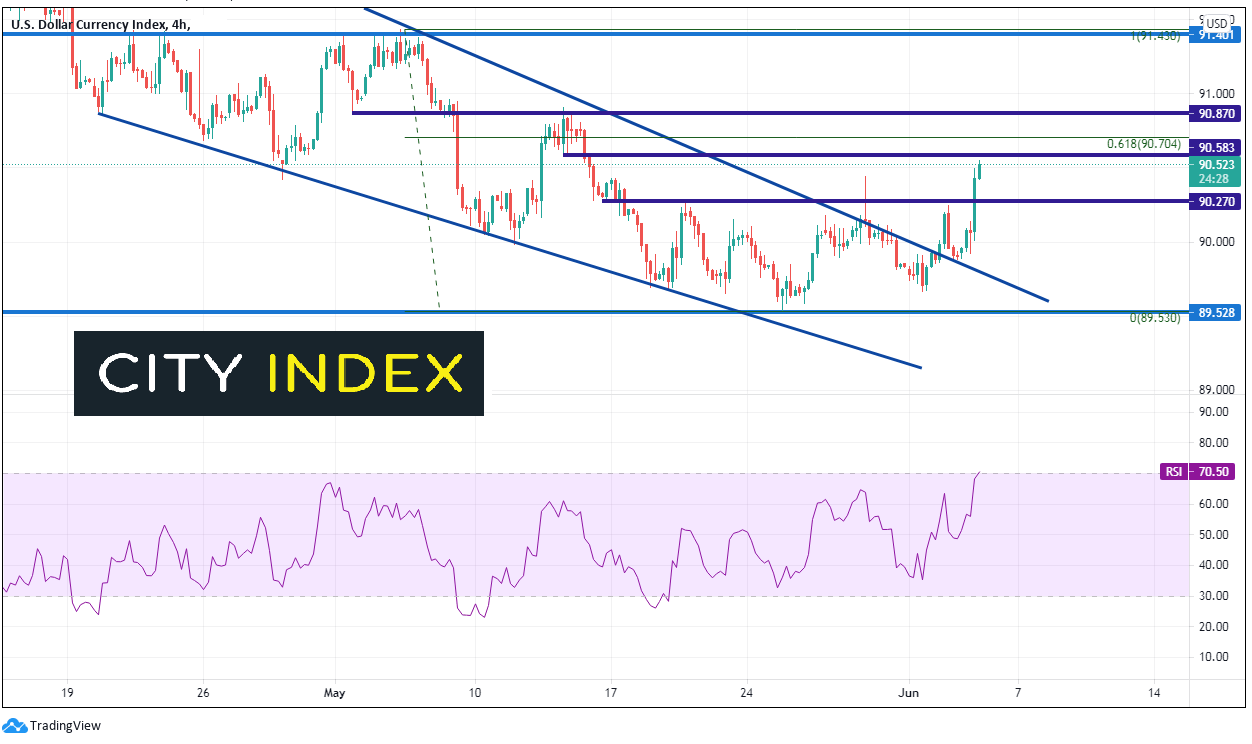

Above there on the 240-minute chart is resistance at the 61.8% Fibonacci retracement level from the highs of May the to the lows of May 25th at 90.70 and then the May 3rd lows near 90.87. Horizontal support below is near 90.27 and the June 2nd lows and trendline support near 89.88. The next support isn’t until the May 25th lows near 89.53.

Source: Tradingview, City Index

With the possibility of a stronger than expected NFP print for May, the DXY has gone bid on taper hopes. Of course, the other reason for the bid could simply be profit taking ahead of the data, as the US Dollar has been falling since the first day of Q2. Watch for revisions to the April print, as well as Average Hourly Earnings for a better gauge on market direction ahead of the Fed in mid-June.

Learn more about forex trading opportunities.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest DXY articles

April 23, 2024 11:01 PM

April 23, 2024 04:19 AM

April 10, 2024 11:24 PM

April 8, 2024 03:35 AM