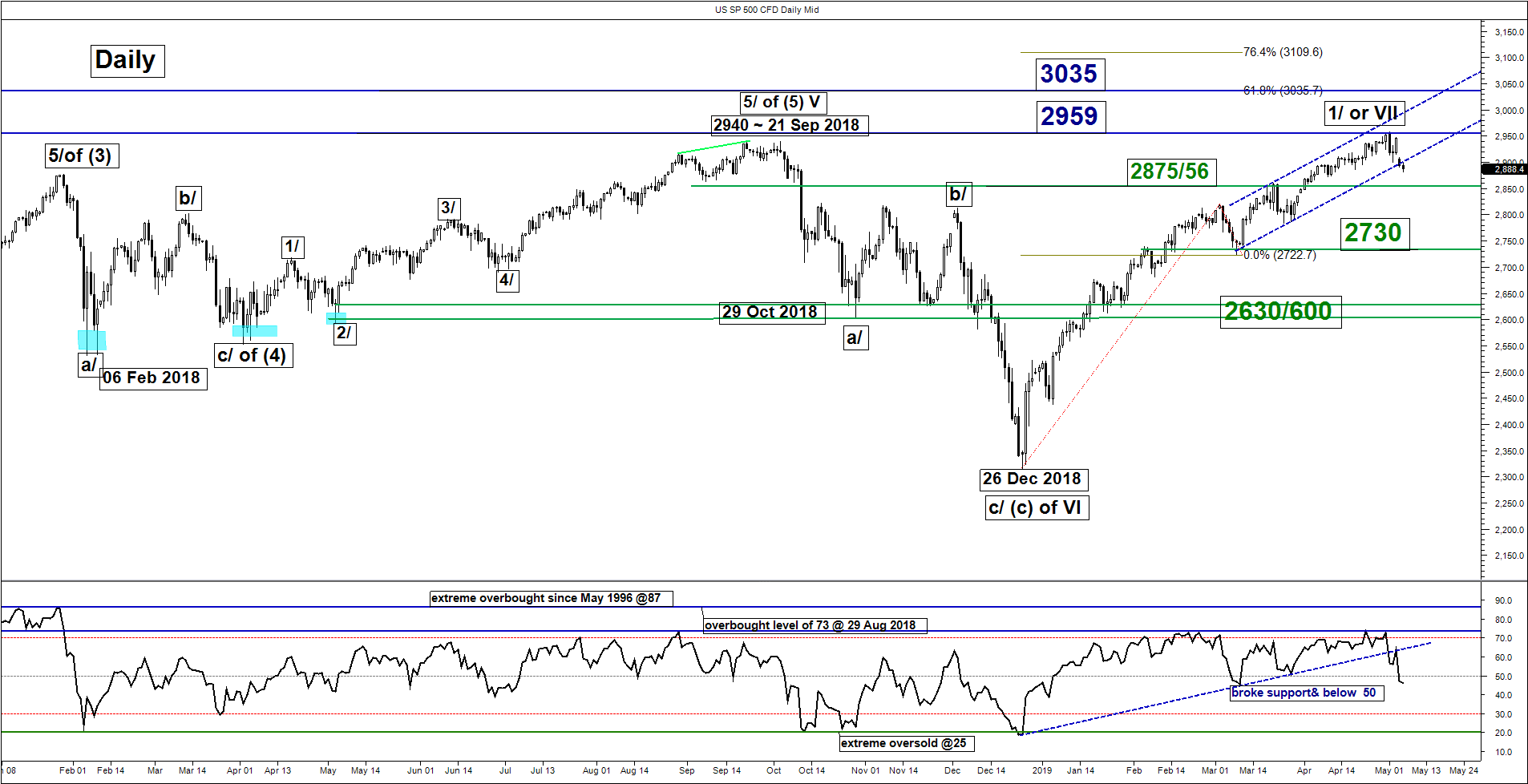

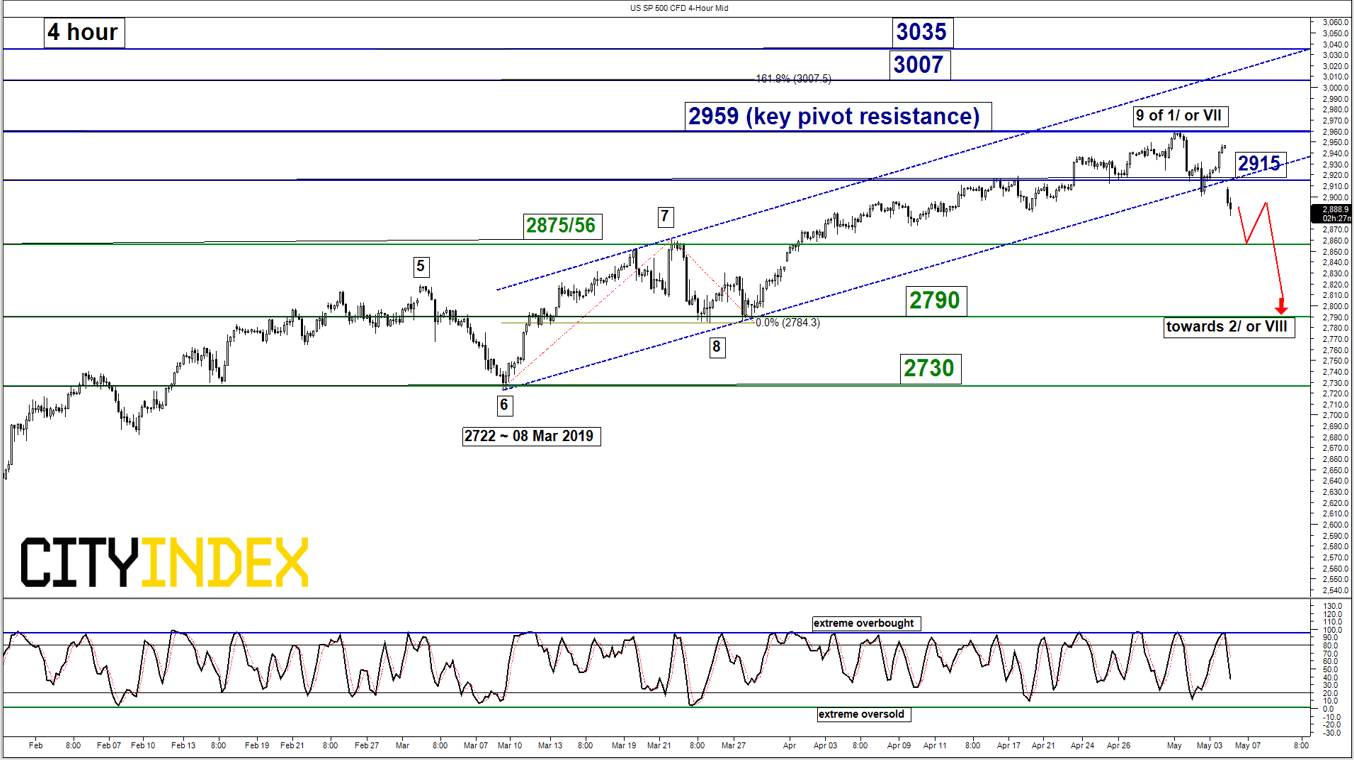

S&P 500 – Risk of undergoing multi-week corrective decline

click to enlarge charts

Key Levels (1 to 3 weeks)

Intermediate resistance: 2915

Pivot (key resistance): 2959

Supports: 2875/56 & 2790

Next resistance: 3007 & 3035

Medium-term (1 to 3 weeks) Outlook

In today’s Asian session 06 May, the SP 500 Index (proxy for the S&P 500 futures) has broken below the 2908 key medium-term pivotal support after it managed to test and staged rebound from 2908 in the middle of last week post FOMC. Today’s drop has been attributed by U.S. President Trump’s trade tariffs rhetoric on Sunday where he has threatened to increase tariffs on US$200 billion of Chinese imports to 25% from 10% on this coming Fri citing disappointment over the slow progress of the trade negotiation talks.

In our previous weekly report, we have mentioned that the Index is in the “residual push” stage with an expected target/resistance set at 2972/90 where the Index printed a high of 2959 (0.4% short of 2972) before it reversed down by 2% from last Fri, 03 May U.S. close of 2946 to print a current intraday low of 2882 in today’s Asian session. Click here for a recap on our previous weekly outlook report.

Technical elements have turned negative where the risk of undergoing a multi-week decline has increased;

- Medium-term momentum has turned negative with the daily RSI oscillator that has broken below a significant ascending support in place since 26 Dec 2018 low (in parallel to the price action low of the Index that kickstarted the 4-month+ rally).

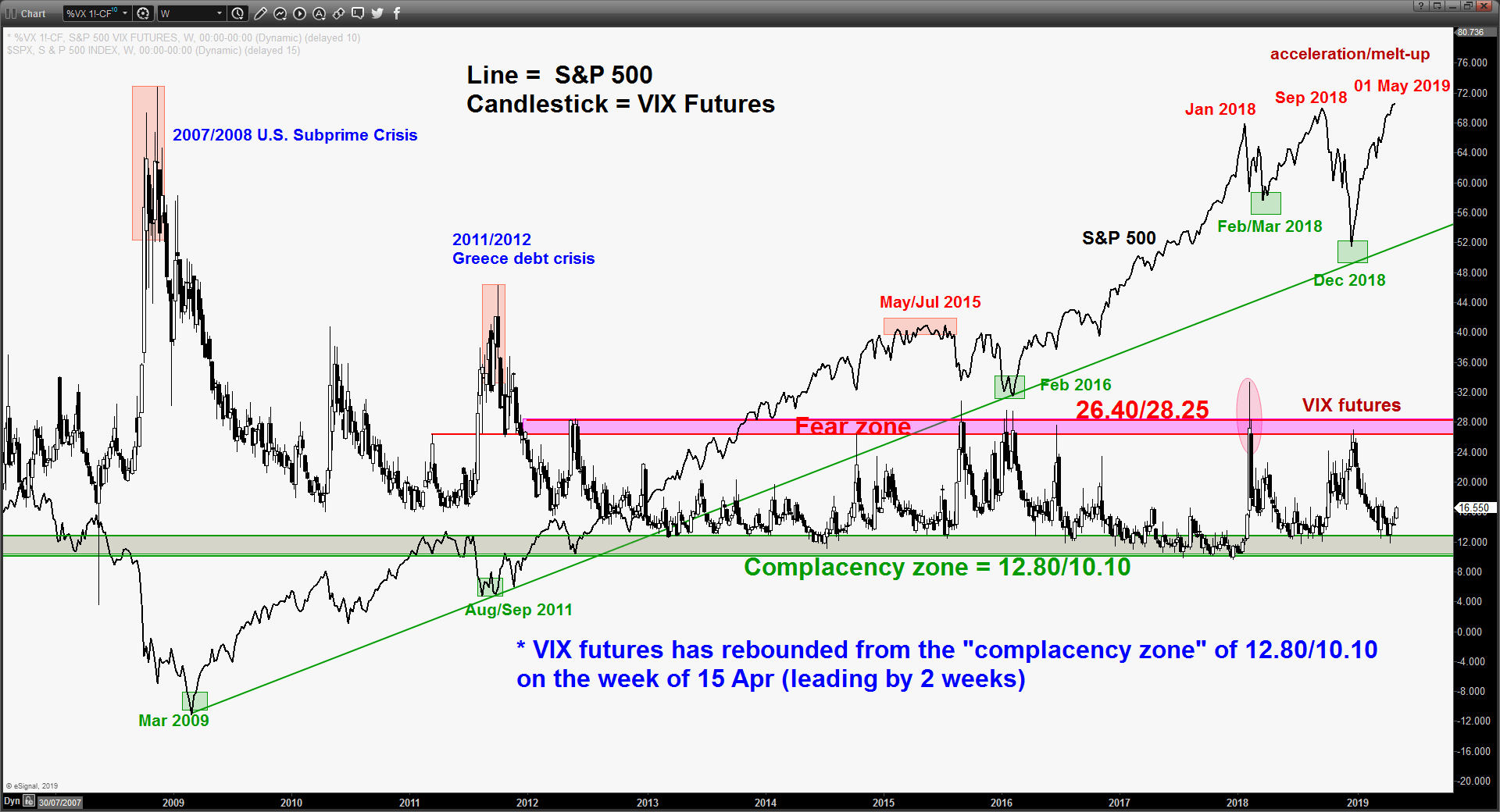

- The VIX futures has started to rebound since 2 weeks ago in the week of 15 Apr 2019 from the “complaceny zone” of 12.80/10.10 where it has led to the significant declines of 10% to 20% in the S&P 500; the most recent being Jan 2018 to Mar 2018 and Sep 2018 to Dec 2018.

- The Index has broken below the medium-term ascending channel support from 08 Mar 2019 low now turns pull-back resistance at 2915.

- The next significant medium-term support rests at 2790 defined by the swing low area of 25/28 Mar 2019 and close to the 23.6% Fibonacci retracement of the entire up move from 25 Dec 2018 low to 01 May 2019 high.

Thus, we turn bearish below 2959 key medium-term pivotal resistance and look for the start of a potential multi-week corrective decline to target the next supports at 2875/56 and 2790 in the first step.

However, a clearance above 2959 invalidates the bearish scenario for the continuation of the impulsive up move towards 3007 and even 3035 next (Fibonacci expansion levels).

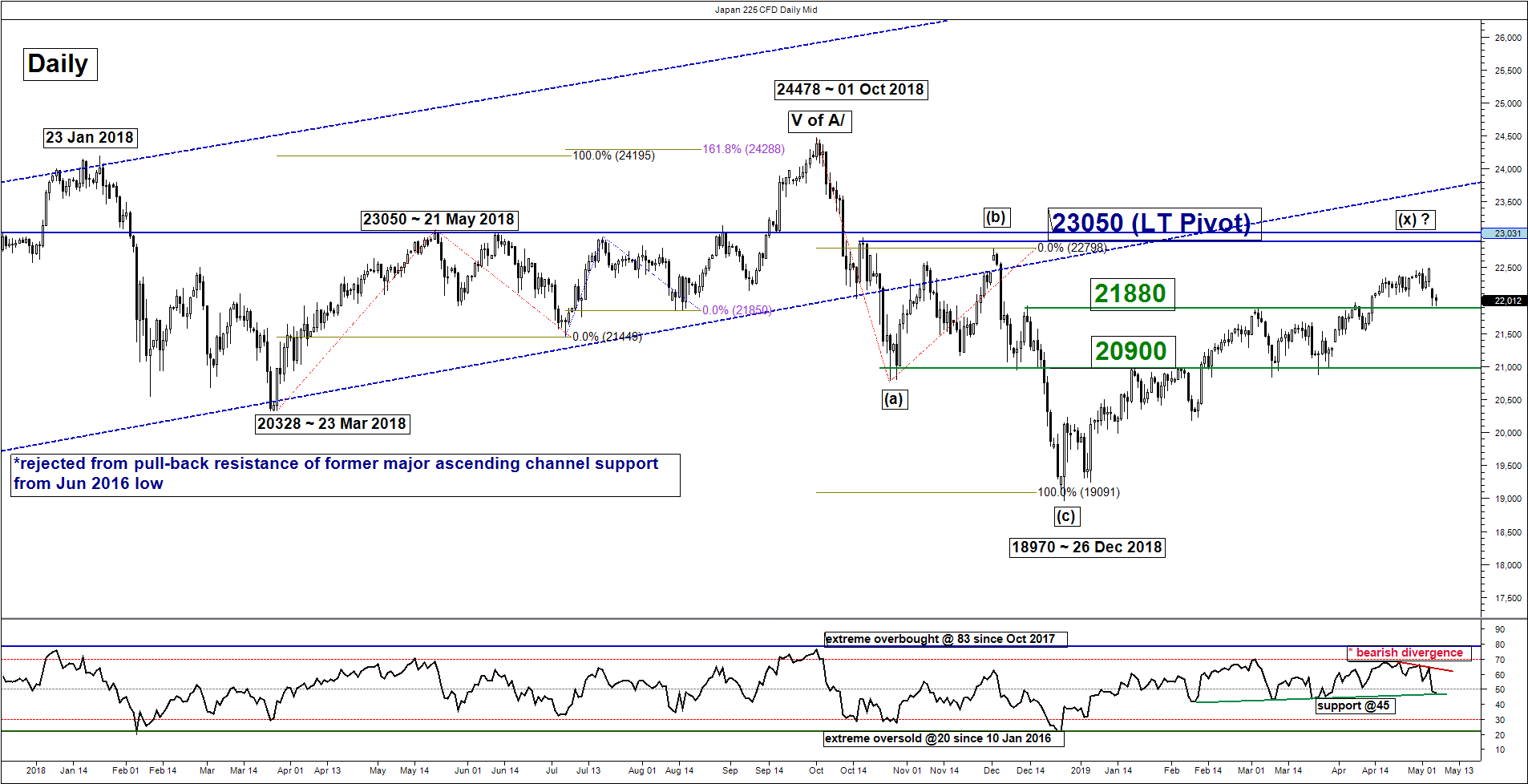

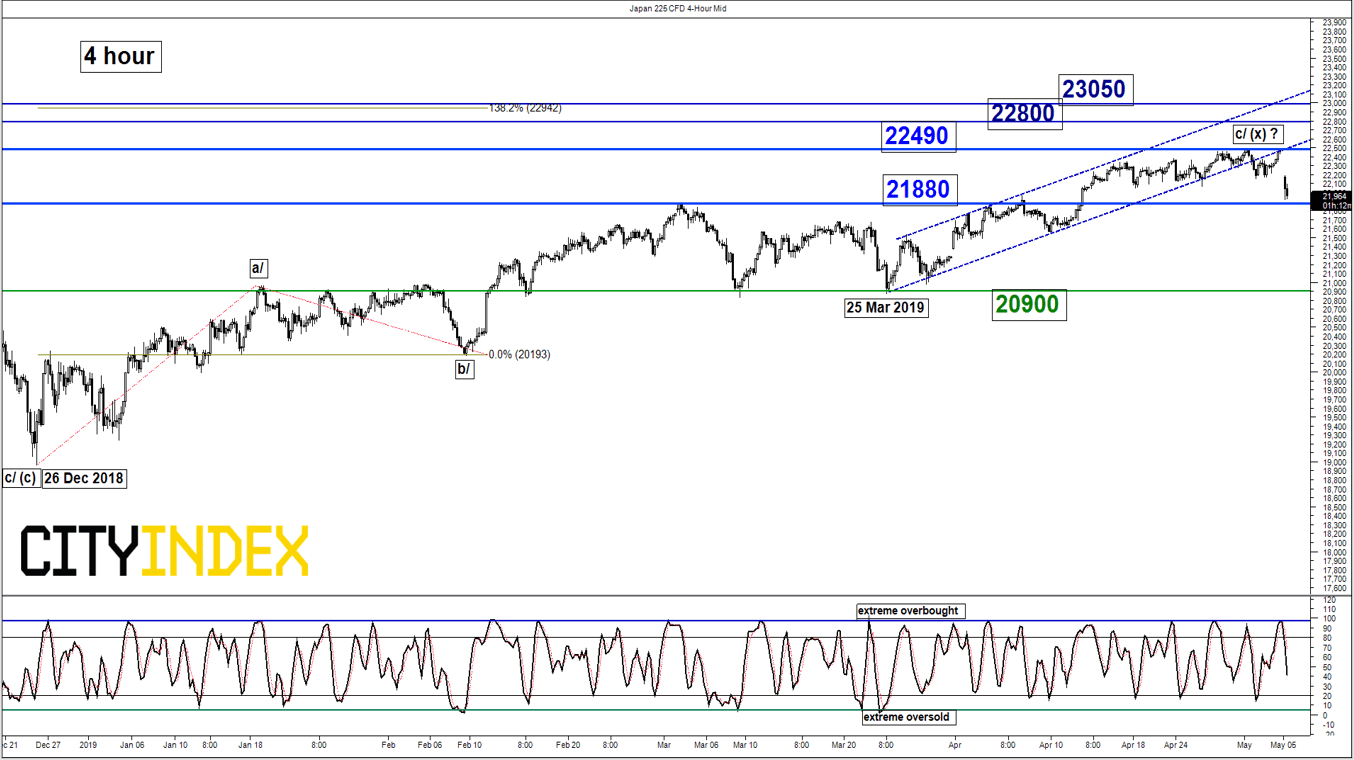

Nikkei 225 – Uptrend at risk, watch 21880 support

click to enlarge charts

Key Levels (1 to 3 weeks)

Supports: 21880 & 20900

Resistances: 22490, 22880 & 23050 (long-term pivot)

Medium-term (1 to 3 weeks) Outlook

Last week, the Japan 225 Index (proxy for the Nikkei 225 futures) has managed to inch higher and ended last week on a retest on the minor range resistance on 22430/490 in place since 29 Apr 2019. In today’s Asian session, it reversed down by 2.5% from last Fr, 03 May U.S. session close of 22482 to print a current intraday low of 21992.

Right now, it is now hovering right above the 21880 key medium-term pivotal support but medium-term momentum has weakened as the daily RSI oscillator has now challenging a significant key corresponding support at the 45 level with a prior bearish divergence signal.

Thus, we decide to turn neutral now between 21880 and 22490. A break below 21880 opens up scope for a potential decline to target the next support at 20900. On the flipside, a clearance above 22490 revives the bulls for a push up towards 22800 and 23050. Do expect an increase in volatility tomorrow, 07 May when the Japan cash stock market opens after its Golden Week holidays.

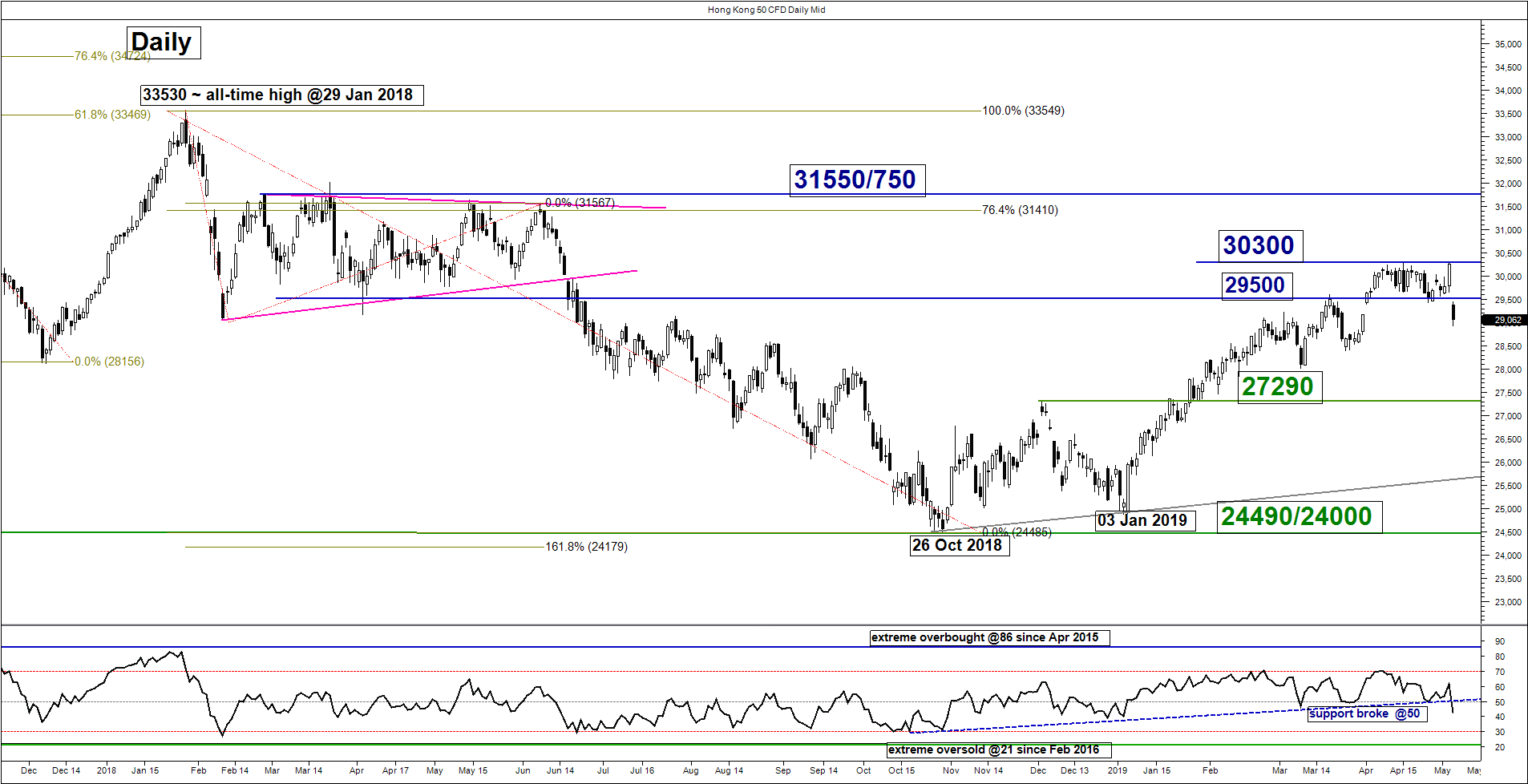

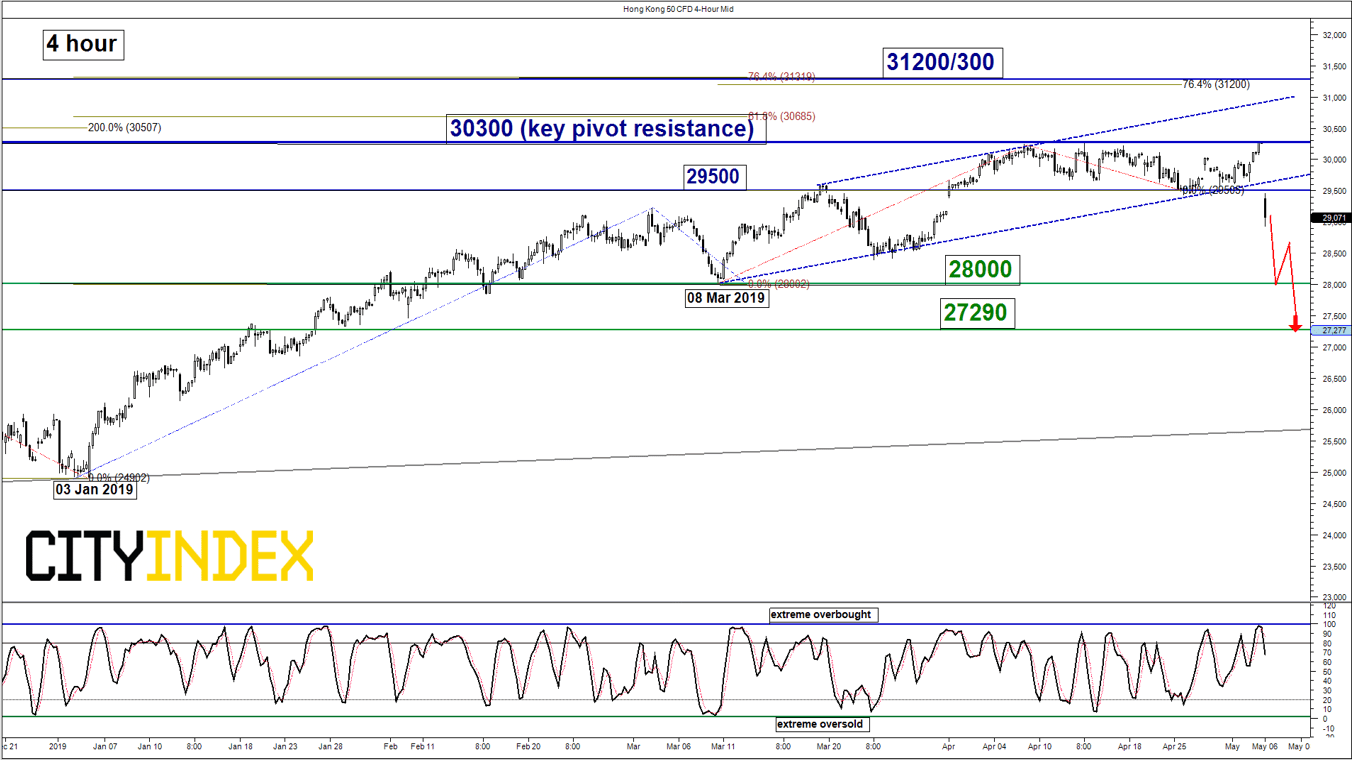

Hang Seng – Broke below 29500, further potential downside

click to enlarge charts

Key Levels (1 to 3 weeks)

Intermediate resistance: 29500

Pivot (key resistance): 30300

Supports: 28000 & 27290

Next resistance: 31200/300

Medium-term (1 to 3 weeks) Outlook

Last week, the Hong Kong 50 Index (proxy for Hang Seng Index futures) has managed to stage the expected push up ended last Fri, 03 May U.S. session with a high of 30293 (0.6% away from the resistance/target of 30500/650).

In today 06 May Asian session, it has plummeted by 4.3% to print a current intraday low of 28935 that broke below the 29500 key medium-term pivotal support reinforce by U.S. President Trump’s trade tariff threats on China imports.

We flip to a bearish bias in any bounces below the 30300 key medium-term pivotal resistance for a further potential corrective decline to target the next supports at 28000 and 27290 (former swing high of 03 Dec 2018 & 50% Fibonacci retracement of the entire up move from 06 Oct 2018 low to 15 Apr 2019 high).

However, a clearance above 30300 revives the bulls for a further impulsive up move towards the next resistance at 31200/300 (Fibonacci expansion cluster).

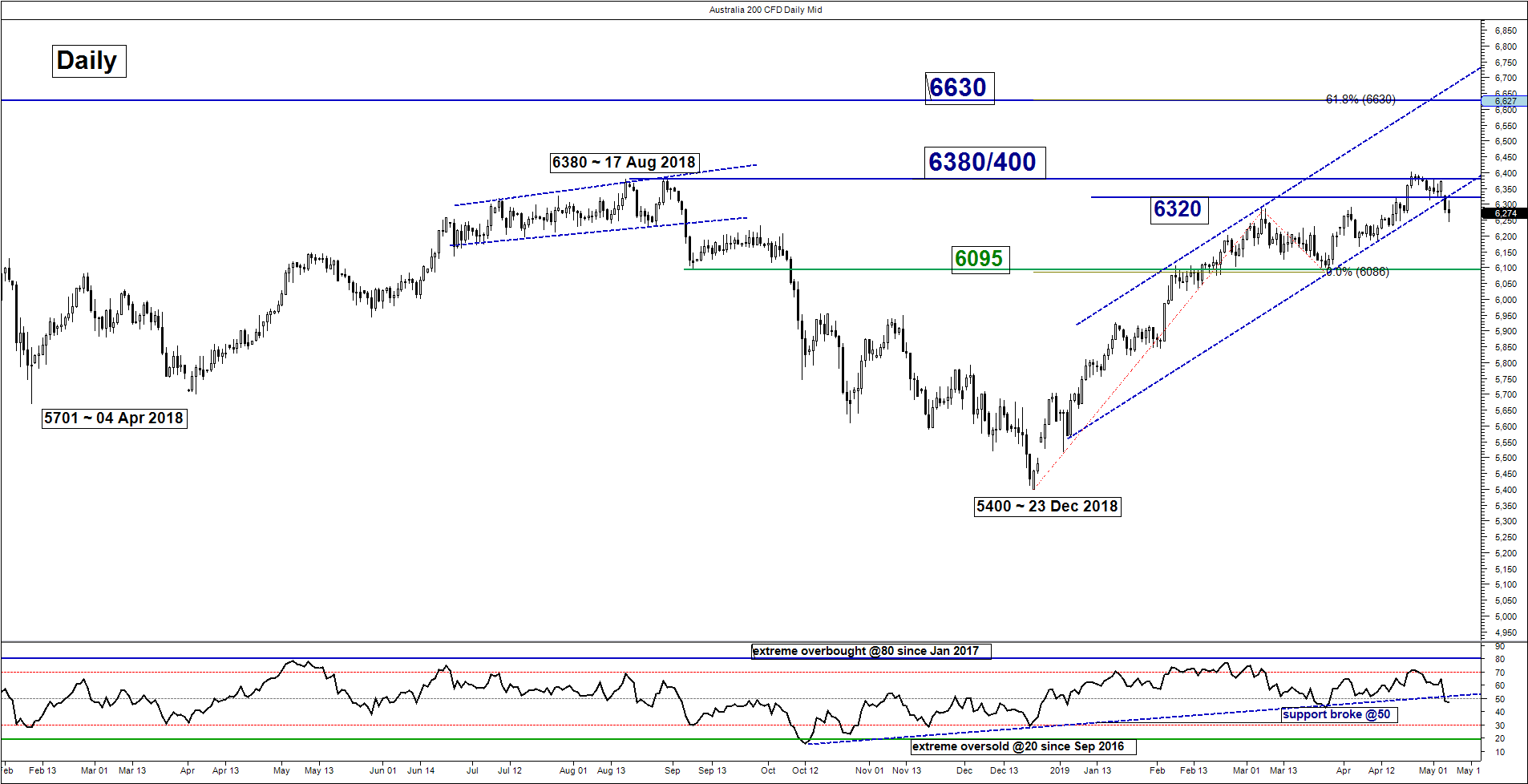

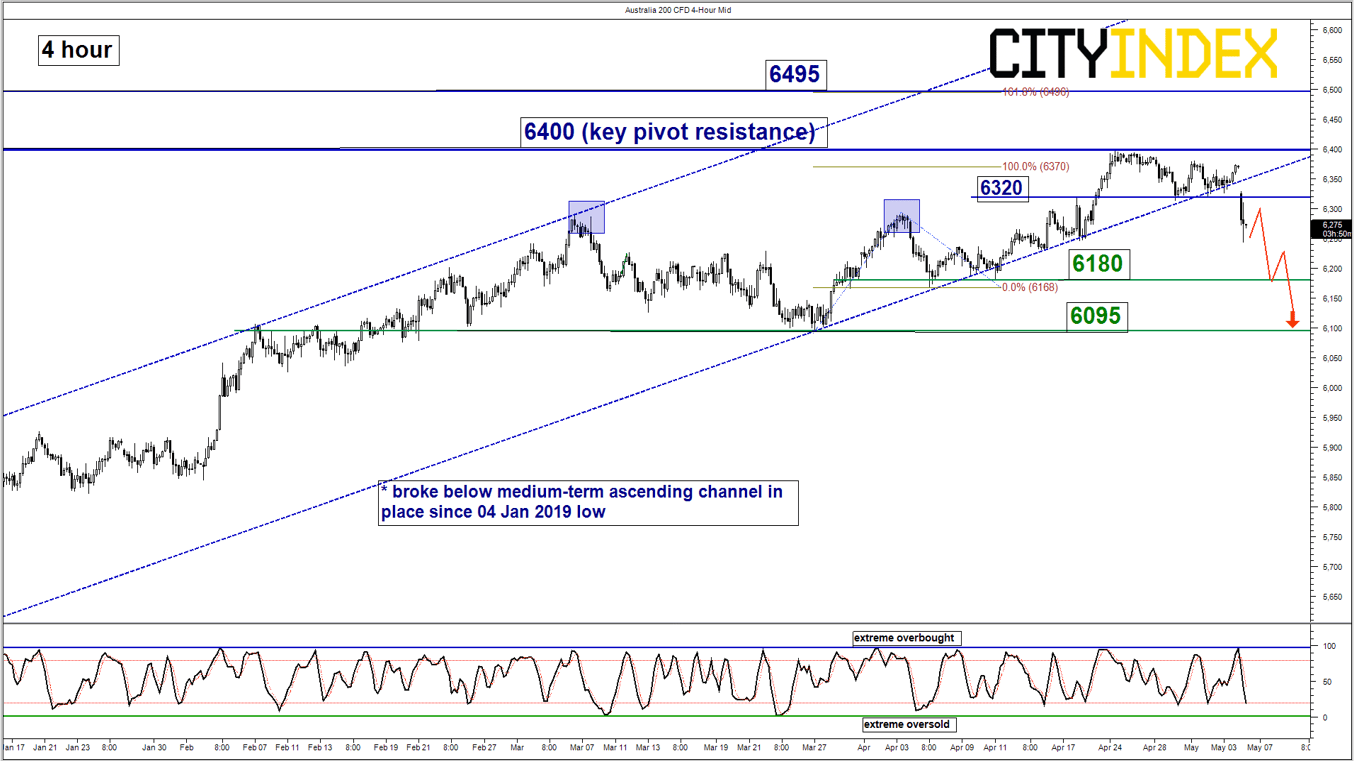

ASX 200 – Broke below 5-month ascending channel support

click to enlarge charts

Key Levels (1 to 3 weeks)

Intermediate resistance: 6320

Pivot (key resistance): 6400

Supports: 6180 & 6095

Next resistance: 6495

Medium-term (1 to 3 weeks) Outlook

The Australia 200 Index (proxy for the ASX 200 futures) has broken below its medium-term ascending channel support in place since 04 Jan 2019 low now turns pull-back resistance at 6320. Our earlier bullish scenario has been invalidated. We turn bearish with 6400 as the key medium-term pivotal resistance for the start of a potential multi-week corrective decline to target the next supports at 6180 and 6095 in the first step.

However, a clearance above 6400 invalidates the bearish scenario to revive the bulls for a push to towards the next resistance at 6495.

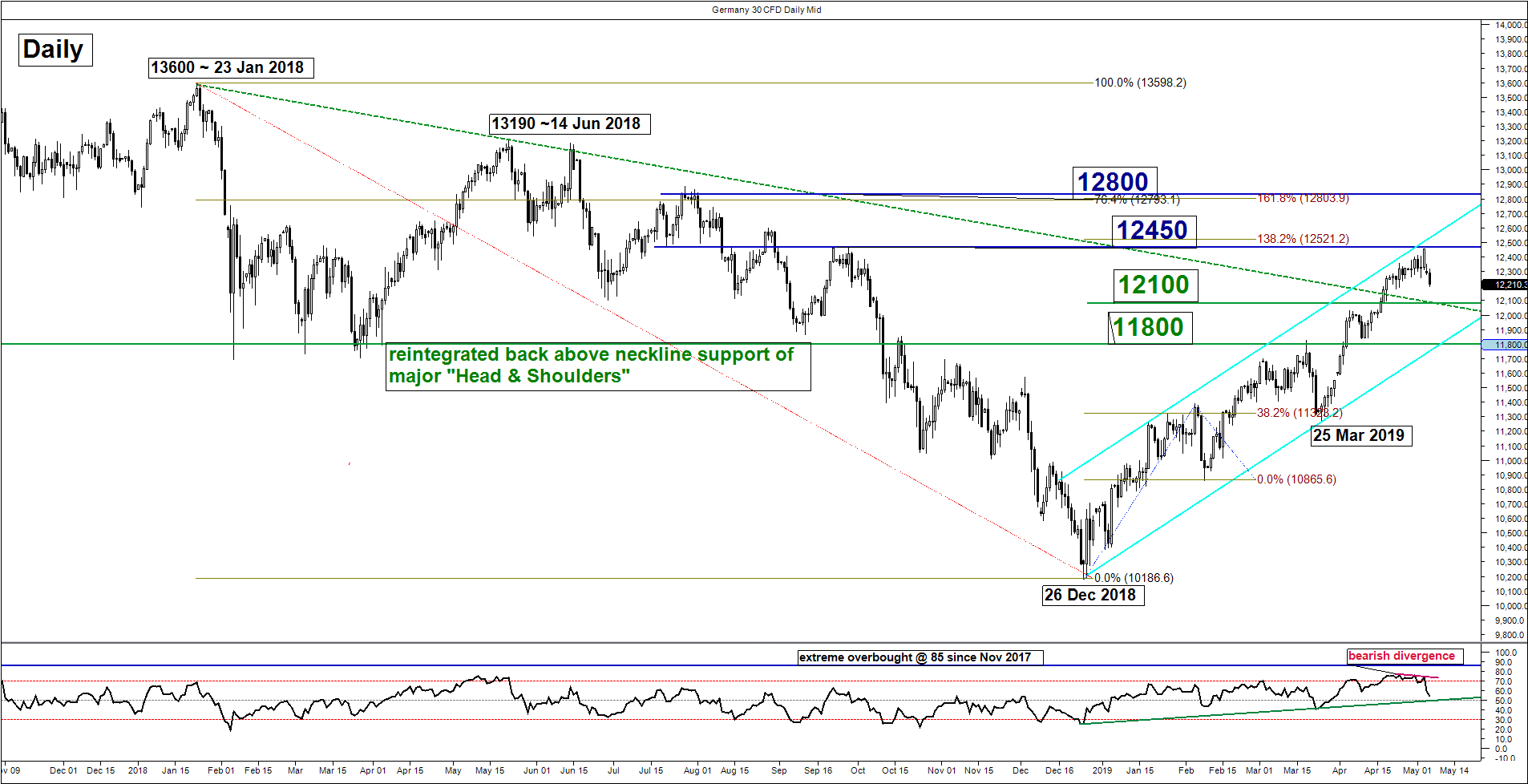

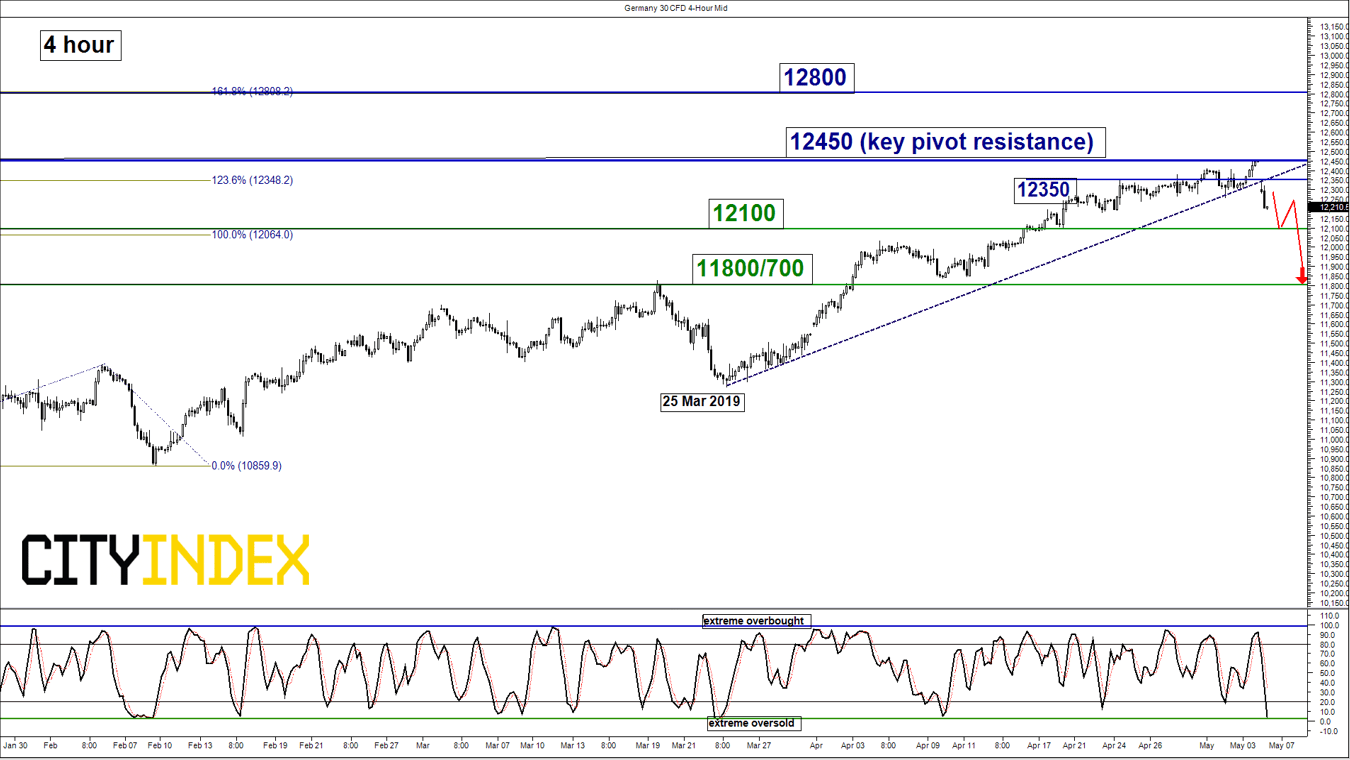

DAX – At risk of staging further corrective decline

click to enlarge charts

Key Levels (1 to 3 weeks)

Intermediate resistance: 12350

Pivot (key resistance): 12450

Supports: 12100 & 11800/700

Next resistance: 12800

Medium-term (1 to 3 weeks) Outlook

Last week, the Germany 30 Index (proxy for the DAX futures) has staged a further push up to test the 12450/520 upper limit of the neutrality zone as per highlighted in our previous report which is also the upper boundary of the major ascending channel from 26 Dec 2018 low.

In today 06 May Asian session, it has staged a decline of 1.9% to print a current intraday low of 12195 on the backdrop of a heightened trade tension between U.S and China after U.S. President Trump’s latest threat to increase additional tariffs on China imports.

Medium-term momentum has started to weaken as the daily RSI oscillator is now testing a significant correspond ascending support at the 50 level (in parallel to the 26 Dec 2018 low of the Index that kickstarted the 4-month+ rally) with a bearish divergence signal. We turn bearish below 12450 key medium-term pivotal resistance and an hourly close below 12100 is likely to open up scope for a further potential corrective decline to target the next support at 11800/700 (the lower boundary of the major ascending channel in place since 26 Dec 2018 low & the former swing high area of 15/19 Mar 2019).

However, a clearance above 12450 invalidates the bearish scenario for a continuation of the impulsive up move to towards the next resistance at 12800 (swing high of 27/31 Jul 2018 & Fibonacci expansion/retracement cluster).

Charts are from City Index Advantage TraderPro & eSignal

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Indices articles

Yesterday 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM