Week Ahead Italy risks and Trump fatigue key risks for stocks

Are markets too optimistic on Trump? Are Italian markets relaxed or complacent? FTSE 100’s rebound cut short by anxiety on Italy Look Ahead: Crude oil […]

Are markets too optimistic on Trump? Are Italian markets relaxed or complacent? FTSE 100’s rebound cut short by anxiety on Italy Look Ahead: Crude oil […]

1, Are markets too optimistic on Trump?

Although we saw fresh record highs in the Dow Jones and S&P 500 last week, there were some signs of scepticism over the longevity of the Trump reflation trade. The S&P has shown signs of fragility at these highs, which could suggest that investors are getting nervous of pushing this rally any further. In November the S&P 500 rose by an impressive 5%, the Dow Jones jumped by 7%. At the time of writing the S&P 500 was backing off recent highs, while the Dow was still tracking higher, however, we think that the Dow could follow suit at the start of a new week as stock markets start to tread softly ahead of the key FOMC meeting next week.

The risk of buying at these highs for US stock markets is two-fold: 1, is enough ‘Trump’ optimism already priced into the market? After all, fiscal largesse is not always a panacea to growth, especially for a large and complex economy like the US. 2, The FOMC meeting is undoubtedly a risk for these markets. Although a hike next week is still 100% priced in by the market, could a signal from the Fed that they will hike interest rates at a faster pace than expected (there is already a near 20% priced in by markets that rates could rise to 1.5% by the end of 2017) next year spook stock markets, especially as we enter into the final weeks of the year?

The latter point is worth considering, a key risk for 2017 is that monetary policy tightens across the globe simultaneously, albeit at differing rates. The FOMC is expected to hike rates, the BOE is not expected to cut rates again next year, and even the ECB is said to be considering a ‘signal on eventual asset buying end’. This statement may sound opaque, however, it highlights how the major global central banks are starting to think about the end of their exceptionally loose monetary policies, which could spell the end for cheap money. While we think that tightening will be gradual, a reduction in liquidity could be significant for risky assets like stocks and emerging market assets in the coming months.

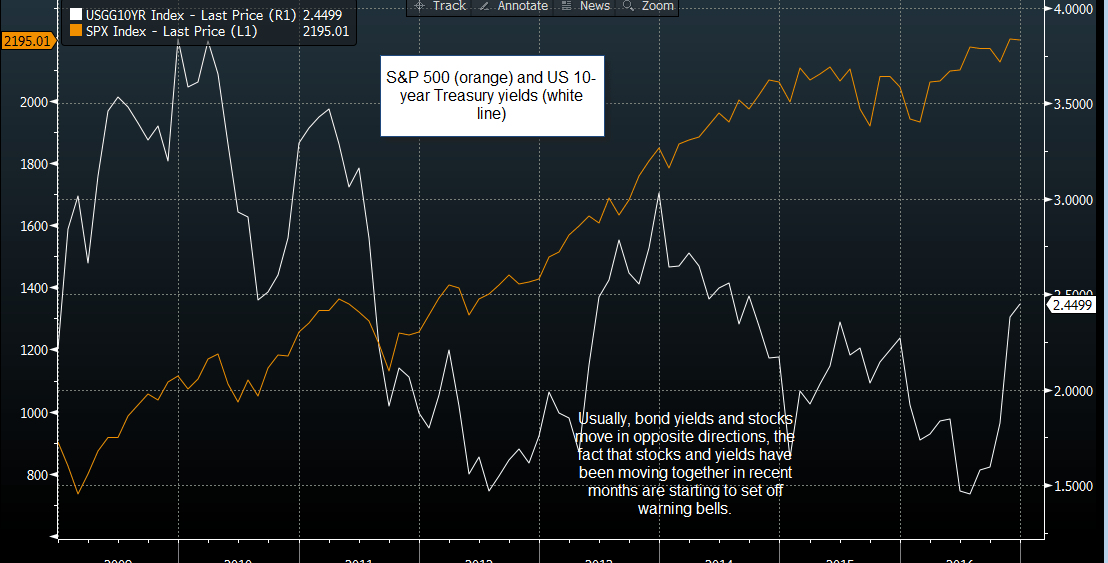

The risk from higher bond yields should also be noted. US 10-year yields surged on Thursday, making a fresh year high, the next key resistance level is 2.5%. US yields across the curve rose in tandem at the end of last week, which is also concerning for stocks as they tend to move in the opposite direction to bond yields, as you can see in the chart below.

Overall, the Santa rally may have come early for US stock markets, and December could be a more difficult month for bulls, as people assess potential challenges to economic conditions for 2017. As a caveat, we do not expect stocks to fall off a cliff, considering that global growth seems to moderately treading higher that would not be an appropriate outlook at this stage, in our view. Instead we think that the march higher in US yields could knock this rally off course and lead to an initial moderate decline of approx. 2-3% by year end. For the S&P 500, the 50-day moving average is key short-term support at 2,156, a deeper drop could see back to the 38.2% Fibonacci retracement at 2,060, however we may have to see downside momentum build for us to get back to this key level.

The FX market could also be impacted if we see a slip for risk in the coming days. USDJPY has surged some 12% in the past month, and reached its highest level since March. This has coincided with the rally in US stocks. In our view, if stocks sell-off then we could see a reversal in USDJPY, potentially back to the 110.00 level.

Of course, December traditionally can be a good month for stocks, and we can’t rule out an extension of the Santa rally. However, there are some key hurdles that could knock stock markets off of their highs as we head into the end of the year, so it is worth being prepared!

Chart 1:

Source: Bloomberg and City Index

2, Are Italian markets relaxed or complacent?

If last Wednesday’s European stock rally showed investors that they felt bearish positioning and selling had run too far, Thursday’s sell-off of stocks, global benchmark bonds and the dollar, revealed that pockets of complacency remained.

Europe’s key stock market, Germany’s DAX and the UK benchmark FTSE 100, bore the brunt of the selling at the time of writing, whilst U.S. stock index futures also pointed to a negative cash market open ahead. Ironically, the stock market at the probable root of resurgent anxiety in Europe, Italy’s FTSE MIB, was less than 0.3% lower.

The FTSE MIB also lies at the crux of difficulties in discerning how much further risk was at stake from Italy’s closely watched constitutional referendum to be held this coming Sunday (read our preview on the City Index website now). The index has, after all, already tanked more than 20% this year, easily the worst performance in the single-currency trading bloc, whilst the euro and sterling also rose.

To be sure, no one thinks chances have improved for Prime Minister Matteo Renzi’s proposals to limit the strength of Italy’s upper house and claw back powers from the regions. For the first time this year, following two political shocks, pollsters are pointing to a win by the anti-establishment vote against constitutional reform.

It could be that investors outside of the country sobered up a day after a degree of euphoria fuelled by cheer from OPEC’s hard won supply deal, which boosted STOXX’s European oil and gas index by 3%. However Italy itself also rallied, including the country’s beleaguered banks’ index, which bounced 3% on Wednesday and added about 0.8% on Thursday.

A degree of level-headedness is always welcome and one establishment view in the country, voiced by numerous economic and political institutes, that another one of Italy’s frequent political upsets would not do markets much harm.

However, with bearish open interest in benchmark Italian government bonds (BTPs) at its highest since Europe’s sovereign debt crisis, the alternative interpretation may yet prove correct—that markets are still underestimating risks from Sunday’s outcome.

Italian banks, with links to the $377bn problem loans on their books that span the globe, may still yet make their presence felt more clearly outside of the country. They own €405bn or 21.6% of all Italian government debt.

Yet Intesa San Paolo, admittedly one of Italy’s most stable lenders, is currently trading at over 80% of tangible book value, close to better capitalised and less balance-sheet heavy BNP Paribas in France.

At the same time the gap between 10-year Italian and German bond yields has latterly held at around 2 percentage points. Even after the premium on Italian paper rose about 50 basis points since the beginning of October, the spread does shows debt investors are not expecting a deeper devaluation of the euro anytime soon that would also hit the country’s predominantly domestic-focused banks.

The stable if not unconcerned picture leaves Italian assets still quite vulnerable to a short sharp shock should any of their key markets gap widely enough that broader markets are unsettled.

Volatility is likely to fan out from trading in stock of Banks Monte dei Paschi di Siena, the most vulnerable in Europe due to weight of bad loans, Genoa’s Banca Carige, trading at less than 10% of book value, and rescued lenders Banca Etruria, Banca Marche, CariFerrara and CariChieti.

The rest of Europe’s banking sector will then be eyed. Deutsche Bank, already hobbled this year by a demand for a massive U.S. Dept. of Justice fine and doubts about its strength as a counterparty, would be back in the frame for more sell-offs. Britain’s RBS, one of the FTSE’s worst-performing shares this year and the only lender to outright fail the Bank of England’s stress test this week, will also be eyed. Stronger lenders like Barclays, Lloyds and UBS, with ties to Europe are unlikely to escape pressure.

Banks aside, assuming anxieties similarly to Brexit-flavoured worries about free movement from an upswing in Eurosceptic sentiment in Italy, the already low-flying shares of airlines like Lufthansa, easyJet and British Airways owner ICAG may also take part in any stock market dive on the back of an adverse outcome to this weekend’s referendum.

All this said, the riskiest scenario to market performance, is still the one that appears the least likely to transpire –Renzi’s exit, and failure of the President to cobble together a new administration from the remnants of his government. A ‘No’, will probably lead to the formation of a new government. The colour of the new administration will resemble Renzi’s if his coalition partners support a new pick for PM by Italy’s President.

If so, market dislocation will quickly be corrected. Like the Brexit vote, , if Italy votes ‘No’ on Sunday then volatility will be difficult to put back in the bottle in the months ahead.

3, FTSE 100’s rebound cut short by anxiety on Italy

The FTSE 100’s bounce following OPEC’s hard won supply agreement on Wednesday was short-lived. The index bore the brunt of a global stock market sell-off triggered by the resumption of a near-parabolic surge in benchmark borrowing costs just days before the latest in a string of difficult-to-predict political risk events.

On Thursday, whilst shares of oil majors and BP and Shell continued to advance on the back of the rebooted outlook for oil prices, all other sectors declined, led by consumer groups and banks. There was also a touch of recent concerns over the future of globalisation stoked by President elect Donald Trump reiterating protectionist rhetoric in recent days. The worst blue-chip performer on Thursday was South Africa-based packaging group Mondi, which has more than 24,000 employees around the globe.

The impact of a strengthening pound added weight to the benchmark. Sterling’s devaluation this year has left investors rubbing their hands in expectation of top-line effects in predominantly overseas-generated FTSE revenues.

From a technical perspective, selling has sliced through this year’s rising trend, undermining the validity of the line further after an earlier violation from the sharp whipsaw on June 24th.

At the time of writing, the index was testing the lower bound of a support (6695/6728) established in September. For bulls, the speed of the market’s breakdown will be alarming enough to trigger lightening-up, lest a stronger band of support between 6675-6615 breaks too. Further downside undoubtedly lies beyond the latter barrier, with few viable strong supports before the 5788 kickback low on 24th June that followed the Brexit vote collapse.

More positively, it’s worth noting that the FTSE 100 has historically had a lot of shakeouts, after which the particular uptrend in place at the time has often resumed. If the support zones outlined above hold, the optimistic pattern may prevail again.

4, Look Ahead: Crude oil

The OPEC put its differences to the side and got its act together to resume its traditional role as a price fixer on Wednesday. The cartel agreed to cut its oil output by a good 1.2 million barrels per day to 32.5 million bpd. The agreement is subject to key non-OPEC members reducing their own output by 600 thousand barrels per day, half of which will be taken care of by Russia. The changes will take effect from the first day of next year.

This is very bullish for oil, make no mistake about it. Yes, oil prices did rally massively already on Wednesday, but that was the unwinding of the downward move from the summer. There’s so much upside potential left in the rally in my view because the market will now be in balance earlier than would have been the case without a deal. Yes, US shale producers will most likely ramp up production again which will ultimately keep a ceiling on prices in the long-term. But in the short to medium term, we expect to see significantly higher oil prices now. What’s more, on top of the now-favourable supply-side dynamics, the global economic recovery is continuing at a steady pace, especially in the US. So rising demand for oil from the US – and China – could be additional factors that could help fuel a rally in oil.

Now up until Wednesday, most people were probably waiting for the OPEC meeting to be over before returning to the oil market. Well, now that we have had that, there is really no reason in our view why they should wait to come back into the market. So, to be clear, we are expecting a bullish breakout above the recent highs now.

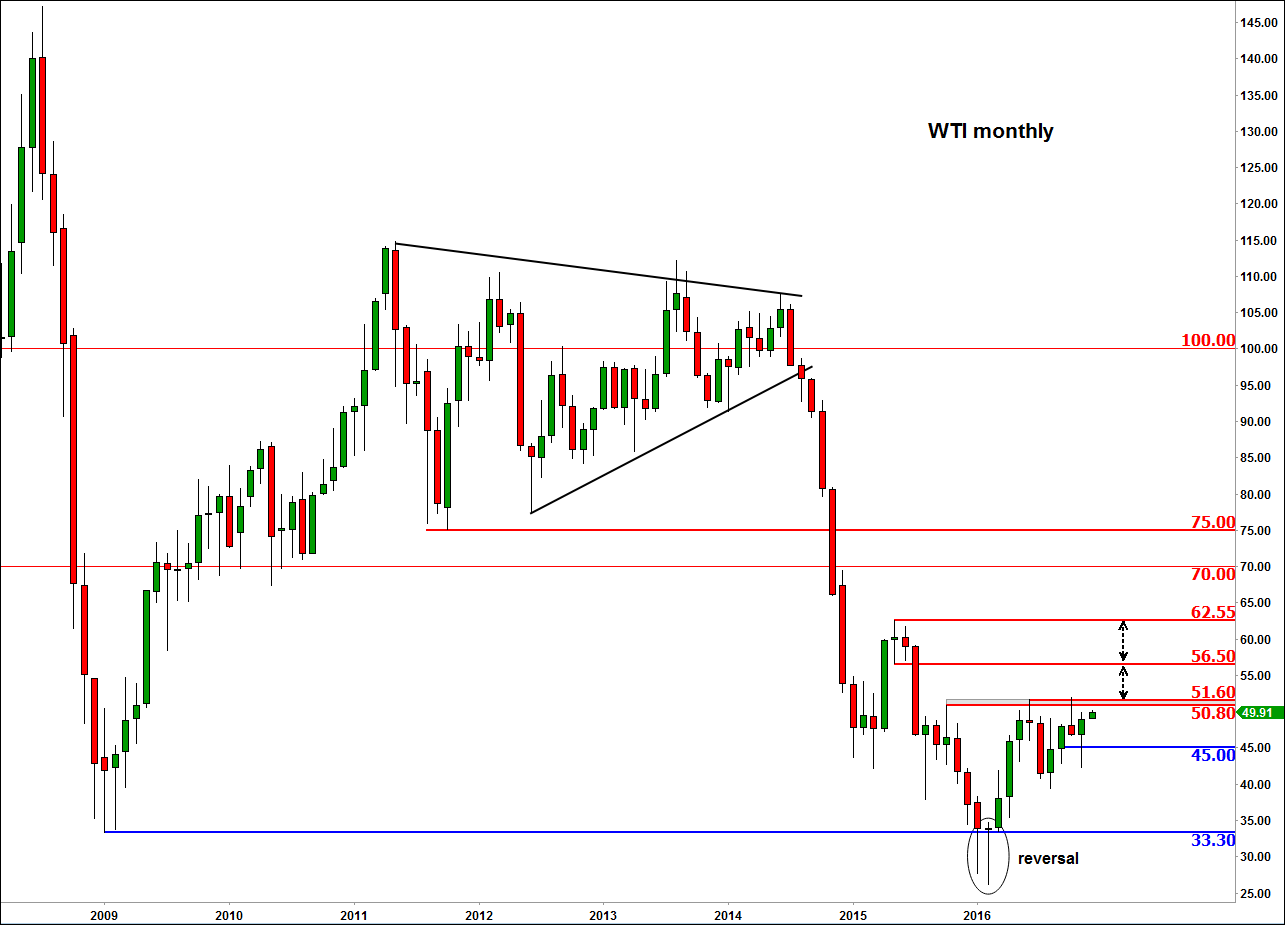

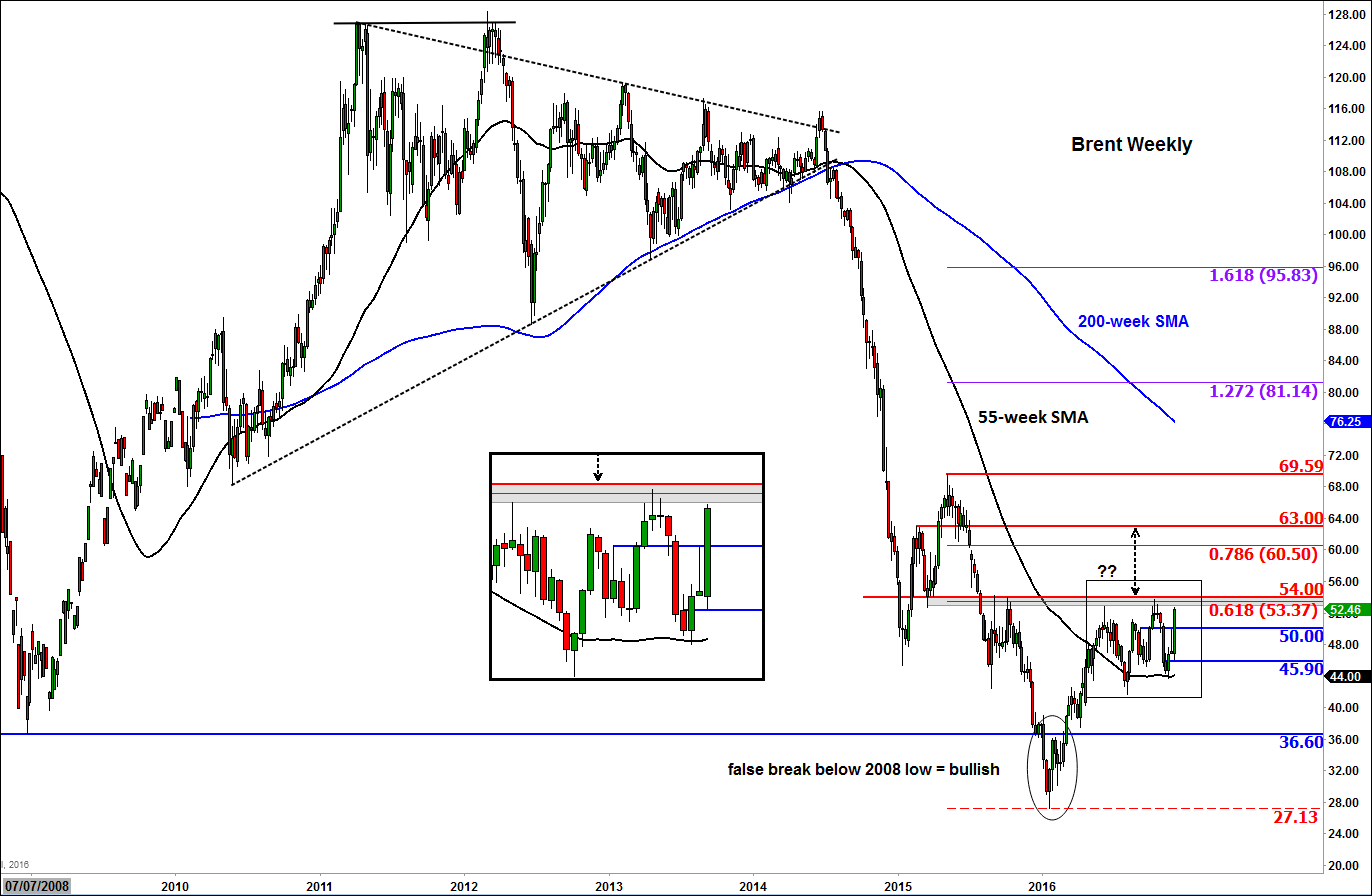

For this view to be confirmed by price, we do need to see a speedy breakout above the recent range highs of around $53.00-$54.00 for Brent and $50.00-51.00 for WTI. If seen, the next objective price move for Brent is at $60, a psychologically-important level, followed by $63, the last support level prior to the down move in the summer of 2015. For WTI, the last support prior to its breakdown was at $56.50 with the 2015 high coming in around $62.55. Those are among the objectives that we are expecting oil prices to rally towards. Our bullish view would technically become void should we see a false breakout scenario around the above-mentioned range highs.

Figure 2:

Source: eSignal and City index

Figure 3:

Source: eSignal and City index