Week Ahead Dutch election risks and FOMC set the agenda for risk

It’s a key week for global risk appetite, the FOMC meeting, where a rate hike is a virtual certainty, is likely to set the tone […]

It’s a key week for global risk appetite, the FOMC meeting, where a rate hike is a virtual certainty, is likely to set the tone […]

It’s a key week for global risk appetite, the FOMC meeting, where a rate hike is a virtual certainty, is likely to set the tone for risky assets like stocks in the coming weeks. Meanwhile in Europe, the Dutch election on Wednesday kicks off a year of political risks for the Eurozone. Here we assess the potential outcomes that these two major events could have on global financial markets.

Political risks in Europe: Dutch election sets the tone

The Dutch election take place on Wednesday 15th March, the results won’t be known until the early hours of Thursday morning, however, exit polls at 2000 GMT on Wednesday evening could give us a good idea of the performance of the PVV party led by far-right Geert Wilders. Until recently when his popularity has taken a bit of a dip, he was expected to win the largest number of votes, and beat centre-right candidate and current PM Mark Rutte. While a large share of the vote for Wilders’ PVV party would send a signal to the world that populism is spreading to Europe, it does not guarantee that Wilders will get into power.

The Dutch political system of Proportional Representation means that coalition governments are usually the norm in Holland, especially when 28 parties are competing for votes on Wednesday. Thus, it could take weeks, if not months, to form an actual government in the Netherlands. Currently Rutte’s liberal party is in the lead, after Wilders’ far-right PVV party started to slip in the polls in recent days. If Wilders’ party does fall back into second place then it is unlikely that he will make it into government, as none of the major parties have said they will form a coalition with the PVV. Thus, power for the PVV seems like a remote possibility with a matter of hours to go before the election.

Dutch outcome could have ramifications for France

The outcome of the Dutch election, by itself, is not a market-moving event, however, it maters because of what it could herald about other, larger elections taking place in Europe this year. If Wilders does not do as well as expected on Wednesday then we could see the markets start to reduce expectations of a victory for the French National Front leader Marine Le Pen in France’s Presidential elections in May.

Thus, the impact on the euro from the Dutch elections could be linked to how the Dutch vote and what this could mean for the outcome of the French election in two months’ time. The euro has had an inverse correlation with Marine Le Pen’s chances of winning the second round of France’s Presidential election. As her chances of winning started to rise in late January, the euro started to decline, however, the euro has outperformed in the last two weeks, as her chances of victory have fallen. This has also coincided with a sharp narrowing of the French – German 10-year yield spread, as French political risks have started to fall.

Of course, a last-minute burst of support for Geert Wilders on Wednesday could be bad news for the euro, especially if it looks like he may get a say in a coalition government. This is something we see as a low probability event. As long as Wilders’ PVV party doesn’t outperform the Liberals then we think that the euro could be unaffected by Europe’s political risks, at least in the short-term.

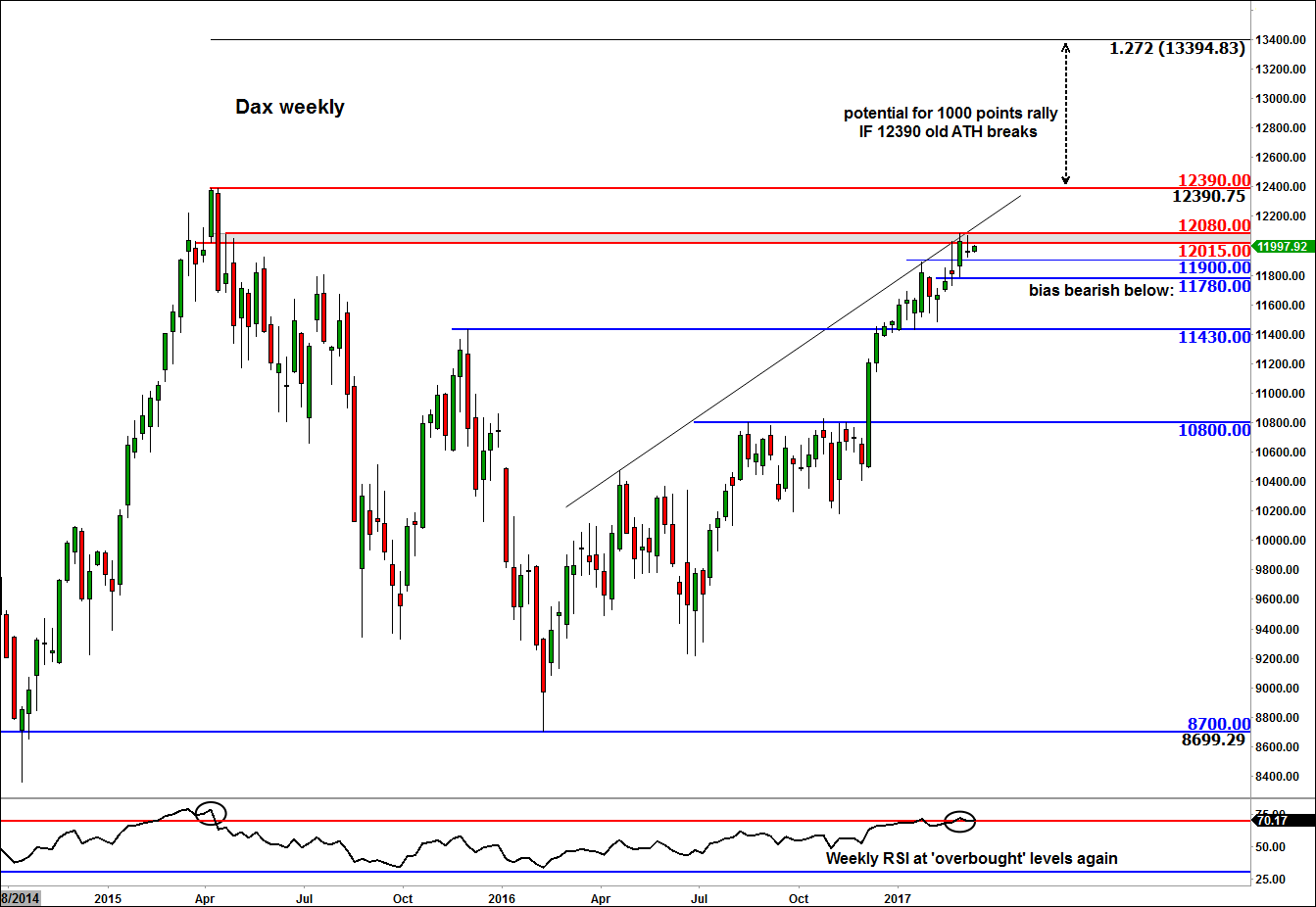

We don’t look closely at the Dutch stock index; instead here is our house view of the Dax index. The short-term technical outlook on the DAX is not very clear, but the German index has reached an important long-term area around 12015-12080. This was the last support and later a resistance zone prior to the breakdown back in April 2015. We are on the lookout for a potential correction here, but so far haven’t seen any bearish price action. A potential break below the 11780 support level could trigger long side liquidation, especially when you consider the fact that the RSI is at ‘overbought’ levels of 70 and above. Alternatively, a potential break above the 12015-12080 area may pave the way for a re-test of the old all-time high at 12390, a decisive break above which may lead to a significant continuation in the rally.

Figure 1:

Source: City Index

Will Janet Yellen puncture Trump’s reflation trade?

This Wednesday 15th March the FOMC will announce its latest interest rate decision at 1800 GMT, soon after we will get a press conference from Janet Yellen. The market is now fully priced for a 25 basis point rate hike from the FOMC on Wednesday, which would see rates rise to 1% from 0.75%; the Fed Fund Futures market now expects a 96% chance of a rate hike. The more important information from the meeting will be the prospect for future rate increases from the Fed for the rest of this year.

To gauge what these prospects are we will need to analyse the latest dot plot, which shows Fed members current expectations’ for Fed rate increases this year. The last dot plot showed that FOMC members expected 3 rate increases in 2017, if this is revised higher then expect the market reaction to be big. We would expect a sharp pricing in of a rate hike in June; currently the market expects a 53% chance of a hike. This could push Treasury yields higher, boost the dollar and weigh on US equity indices, which have recently backed away from record highs.

It’s all about the pace, the pace, the pace of rate hikes…

Essentially, a faster pace of rate hikes is likely to be a major threat to the “Trump” rally, and could seriously impede further gains for US equity indices over the coming weeks as US Treasury yields and the dollar make a comeback.

Why wage data may not stop a hawkish slant from the Fed

So what are the chances of a faster pace of rate hikes from the Fed? We think that the chances are relatively even at the moment. The wage data included in the February jobs report was relatively muted at 2.8%, which doesn’t suggest inflationary pressures just yet. However, wage data is a lagging economic indicator, and other indicators suggest that the US economy continues to do well, even without any sign of the Trump administration’s fiscal stimulus. For example, Citibank’s US economic surprise index is close to its highest level since 2014, so the Fed has genuine reason to worry about getting behind the curve.

While European election risks and the triggering of Article 50 in the UK are key global political risks, the Fed meeting is by far the most important event for global financial markets. The US dollar is still the world’s most traded currency, US Treasury yields are still the world’s interest rate benchmark, and US stock markets set the tone for global risk appetite. If the Fed does rock the boat this week then we could see shock waves across global financial markets, with US asset prices and emerging markets particularly badly hit. A faster pace of rate rises for the Fed could see a 2-3% decline in global stock markets, and a move back above 2.6% in the 10-year Treasury yield, along with a quick return back to the 104.00 early January highs in the dollar index.

Of course, our analysis only predicts a 50/50 chance of a faster pace of rate hikes. If the Fed confirms that it only expects to hike rates three times this year then we could see a sigh of relief from risky assets, leading to a resumption of the Trump rally, weaker Treasury yields and a lower dollar. All eyes will be on Yellen and co. on Wednesday.