January 19, 2020 11:27 AM

Week Ahead: Now that US-China Trade Deal is Signed, What’s Next?

Aside from the ceremonial signing of “Phase One” of the US-China Trade Deal, this past week was seemingly uneventful. The US Senate passed the United State- Mexico-Canada Agreement (USMCA) and it is currently waiting President Trump’s signature. Things between the US and Iran in the Middle East have calmed down, and stocks have continued their climb to all time highs on the back of better bank earnings.

The World Economic Forum’s annual meeting will be held next week in Davos, beginning on Wednesday. Many world leaders and large companies attend this event, including large oil companies, and it may be good for some potentially market moving soundbites.

With many of the political and geo-political events on the sidelines (for now), the markets next week are likely to begin focusing once again on central banks, macro-economic data and earnings.

There are three Central Bank meetings next week, which include the Bank of Japan, the Bank of Canada, and the European Central Bank.

Earnings season kicks into high gear next week, with such notables reporting as HAL, NFLX, TXN, JNJ, and AXP.

In addition, macro-economic data highlights for next week are as follows:

Monday

- Martin Luther King Jr. Day – US Markets closed

- ECB President Lagarde Speech

Tuesday

- BOJ Interest Rate Decision and Quarterly Outlook Report

- UK Employment data (DEC) Claimant Count expecting +26,000 vs +28,800 last

- German and EU ZEW Economic Sentiment Index (JAN). Expectations are for 15 and 6, respectively.

Wednesday

- Canada Inflation Rate (YoY) (DEC) Expectations are for 2.2% vs 2.2% last

- (MoM) expectation is for 0% vs -0.1% last

- BOC Interest Rate Decision and Monetary Policy Report

Thursday

- Australian Consumer Inflation Expectations (JAN) Expecting 3.7% vs 4% last

- Australian Employment Change (DEC) Expecting +16,000 vs +39,900 last

- ECB Interest Rate Decision, Press Conference, and Strategic Review

- Crude Oil Inventories

Friday

- BOJ Monetary Policy Meeting Minutes

- Worldwide Flash PMIs – In particular, for the US this will be the first piece of manufacturing data since the US-China trade deal was agreed. Markets participants will look closed to watch for an uptick in US PMIs.

- ECB President Lagarde Speech

- Canadian Retail Sales (MoM) (NOV) Expecting 0.4% vs -1.2% last

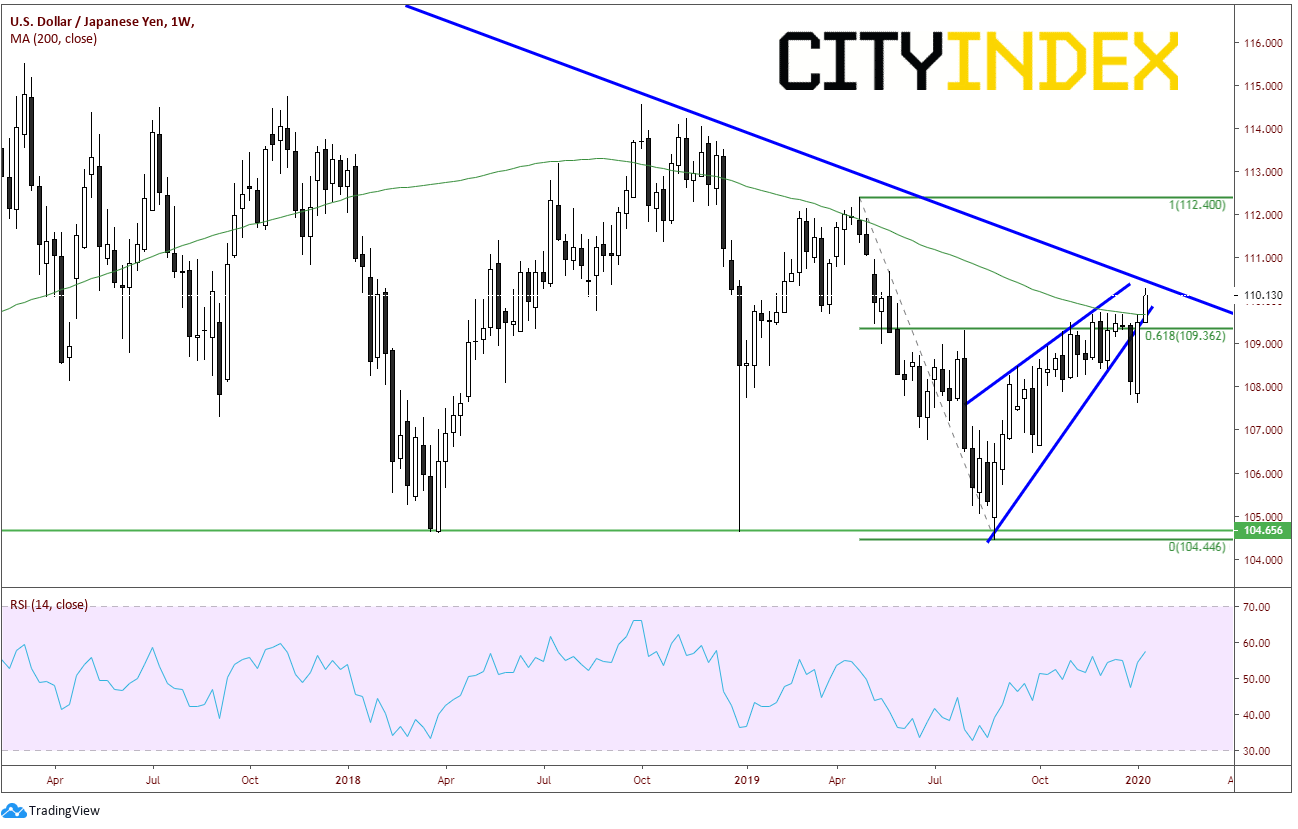

Chart to Watch: USD/JPY

Source: Tradingview, City Index

As stocks continue to put in new all-time highs, USD/JPY is moving right along with them. During the first week of the year, price put in a bullish engulfing candle after a false breakout out of the rising wedge. Last week, USD/JPY squeezed above strong horizontal resistance and the 200-week moving average near 109.70. The pair is currently approaching a long term downward sloping trending dating back to mid-2015. If price breaks above the trendline, it will look to fill the gap from the first week of May 2019 near 110.90/111.00.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

Latest Crude Oil articles

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM

April 10, 2024 06:07 AM