February 14, 2020 10:49 AM

Week Ahead: More Downside for the Euro?

This past week, markets seemingly have pushed past the number of new “adjusted” number Coronavirus cases. Although the number increased dramatically, these were cases that were under suspicion already, but could not be verified due to lack of testing equipment. Once the WHO arrived, they were able to verify these cases. Now that most of the suspected cases have been verified, China began pumping stimulus into the economy to try and get things back to “normal”. US stock indices traded to new highs this week; they don’t seem worried about contagion of the Coronavirus.

Fed’s Powell stayed the course during his Humphrey Hawkins testimony this week. Lower for longer, which made his testimony relatively uneventful.

The Euro, on the other hand, had quite and eventful week. Whether you blame it on poor data out of Europe, the unwind of the carry trade, or the Coronavirus, the Euro was under serious pressure this week. EUR/USD is down over 2% over the last 2 weeks, while EUR/JPY and EUR/GBP played catchup this week, both down .8% and 1.83%, respectively. There looks to be more downside in the Euro ahead for this week.

As far as the primary elections in the US are concerned, there are no primaries or caucuses until next Saturday, February 22nd, when the Nevada caucuses will be held. However, candidates are gearing up for Super Tuesday on March 3rd, when 15 primaries will be held. The race for the Democratic nomination is currently neck and neck between Bernie Sanders and Pete Buttigeg, however Michael Bloomberg will first appear on ballots on Super Tuesday. His entrance into the race is expected to disrupt the current leaderboard. There are already heated exchanges between Bloomberg and President Trump, and Bloomberg hasn’t even been on a ballot yet!

Earnings reports next week include WMT, DE, HSBC and LLOY

Expected economic highlights include:

Monday

- Japan: GDP

- US Holiday – President’s Day **markets closed**

Tuesday

- Australia: RBA Minutes

- UK: Claimant Count Change

- Germany: ZEW Economic Sentiment Index

- EU: ZEW Economic Sentiment Index

Wednesday

- UK: Inflation Data

- Canada: Inflation Data

- US: Housing Starts

- US: Building Permits

- US: PPI

- US: FOMC Minutes

Thursday

- Australia: Employment Change

- Germany: GKF Consumer Confidence

- Germany: PPI

- UK: Retail Sales

- Canada: New Housing Price Index

- US: Philly Fed Manufacturing

- Crude Oil Inventories

Friday

- Global Flash PMIs

- EU: Inflation Rate

- Canada: Retail Sales

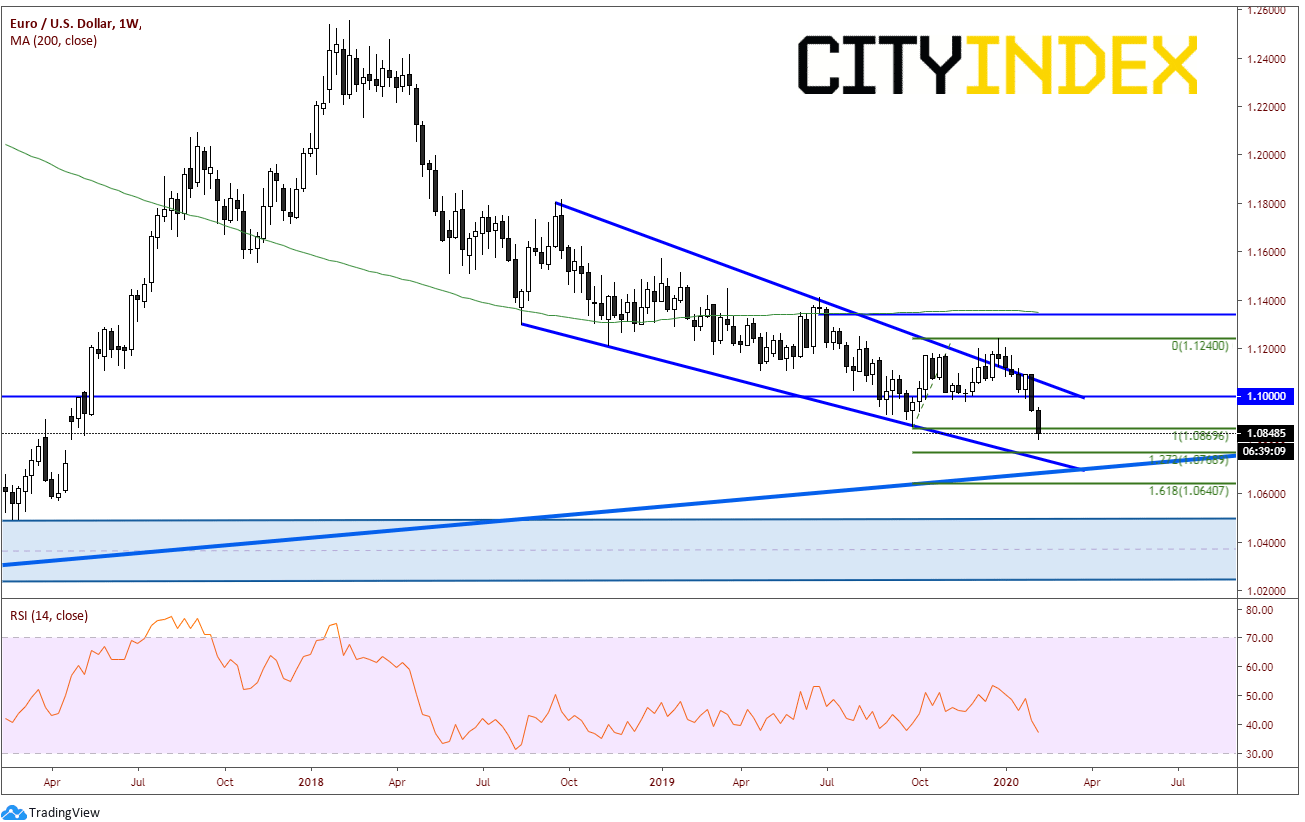

Chart to Watch: Weekly EUR/USD

Source: Tradingview, City Index

EUR/USD has been in a falling wedge since the summer of 2018. In December 2019, price tried to breakout to the upside, only to fail to move higher during the last week of 2019. In 2020, price reversed course and began trading lower back inside the wedge. Often, we see that when price fails to breakout of one side of the wedge, it tries to retest the other side of the wedge. EUR/USD has currently taken out prior lows at 1.0879. First support is a gap from 2017, between 1.0775 and 1.0820. Below there is a strong cluster of support between 1.0700 and 1.0750, which includes:

- The 127.2% extension from the September 2019 lows to the December 2019 highs

- The bottom trendline of the falling wedge

- An upward sloping trendline dating back to 2000!!

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Latest Dollar articles

April 23, 2024 11:09 PM

April 18, 2024 06:20 AM

February 16, 2024 11:30 AM

February 7, 2024 03:30 PM