Vodafone turnaround rings a little hollow

Vodafone shares added a percentage point to early gains on Tuesday, extending their rise to 3% after its CEO said the group was working to improve […]

Vodafone shares added a percentage point to early gains on Tuesday, extending their rise to 3% after its CEO said the group was working to improve […]

Vodafone shares added a percentage point to early gains on Tuesday, extending their rise to 3% after its CEO said the group was working to improve UK customer service.

It might have been a signal investors were hoping to hear—the group now holds the ignominious title of Most Complained About UK Pay-Monthly Mobile Operator—but it was more likely to be a nod to good PR on Vittorio Colao’s part than one borne out of anxiety about customer experience.

That’s because the world’s cell phone Number Two this morning broke 7 years of keeping investors on hold for annual underlying earnings growth, with ‘organic’ EBITDA of £11.6bn.

It was a fraction below even our sub-consensus call (£11.62bn) and compared with Vodafone’s guidance of £11.7bn-£12bn.

But shareholders didn’t seem particularly perturbed.

They were eyeing the positive percentage change for the year, +2.7%, something not seen around these parts since 2008.

Such underlying achievements are certainly a milestone worth marking; though don’t look at the 11% fall shown by a more conventional earnings measure, operating profit.

And so much for ‘organic’ too: net debt ballooned 31% to £29.9bn, underlining the real cost of Vodafone’s Project Spring investment programme to improve networks and customer experience (in Europe.)

Note total expenditure on capex, networks and ‘inorganic growth’ has been £47bn over three years.

Whilst the shares had remained aloft for all of Tuesday, although well off their best at the time of writing, the overall response to what was arguably VOD’s most important milestone this decade, was muted.

Little detective work would be required to discover why.

For one thing, Vodafone’s much vaunted European growth apparently flattened at 0.6% quarter-on-quarter, though on balance it’s fairer to reserve judgment on Europe.

After all, Vittorio Colao, the essential architect of this not particularly sharp turnaround said “I am confident we will sustain our positive momentum in the coming year, allowing us to maintain attractive returns for our shareholders.” This momentum was detailed in guidance calling for between £12.4bn-£12.8bn organic EBITDA in financial year 2017. That compares with Thomson Reuter’s weighted-average consensus of 8 forecasts which currently foresees £12.5bn.

And tardy progress in return for multibillion outlays isn’t Vodafone’s fault, of course.

Europe has got to be one of the most expensive mobile services markets in the world. And it will get tougher as the European Union pushes through plans to totally phase-out roaming charges over the next few years.

Not to mention that almost £50bn later, Vodafone is still not quad-play.

Rivals—which will soon include Sky—are fighting over broadcast rights, pushing the average cost Vodafone will face, when it catches up, higher.

Of course it may not have to catch-up.

Some sort of comprehensive European tie-up—over a much bigger batch of assets than Liberty’s Ziggo—still makes the most sense for a more comfortable Vodafone future.

Little new info about the proposed 50-50 JV on Tuesday though, which was somewhat worryingly reminiscent of VOD’s radio silence during the last set of discussions with Liberty over the type of Greater European tie-up mentioned above. Those talks collapsed.

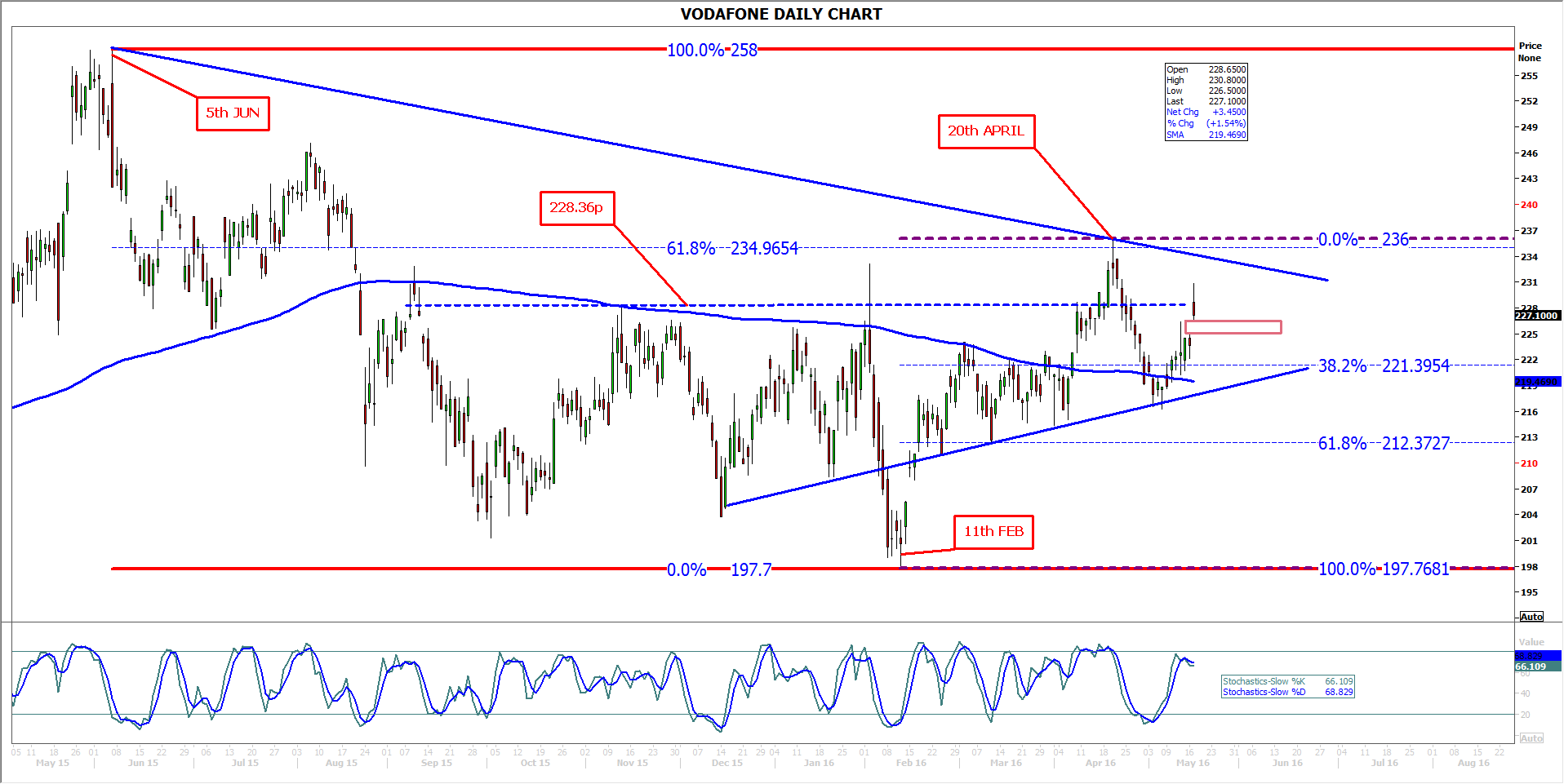

The shares didn’t quite follow, but they did slide as much as 23% off 15-year highs last June, before bottoming in February.

Tuesday’s polite share price rise also probably reflected the nod to shareholders from the group in the form of 2% uplift in the final dividend.

At least the divi is unlikely to become technically ‘uncovered’ again, for the next year at least, with Colao pledging growth in the range of 3%-6%, and free cash flow guided at £3.2bn, from £1.13bn in 2015.

OK, it’s not quite ‘free’ free cash flow; it was stated after capex, before M&A, spectrum and restructuring.

From a technical basis, the shares seem to be off the ropes from late 2015, though (and this is the final Vodafone kink I’ll ask you to overlook in this article) the fearsome spike down to 2016 lows in February could, strictly speaking have invalidated the uptrend that has developed since 15th December. Even so, momentum has been sufficient to lift prices up to an umpteenth test of the 228.36p/233.67p region, below which investors have concluded, for now, the stock is too cheap.

Sustaining prices above that band hasn’t been easy though, including on Tuesday. The shares have gapped at least a penny ha’penny, using Monday’s high and Tuesday’s low as reference points but of course more, on a close-to-open basis.

Tuesday’s candle doesn’t look particularly solid either, suggesting there won’t be much of a wait before the inevitable gap fill.

Our chosen momentum gauge had already turned tail intraday, though wasn’t quite overbought (see Slow Stochastic Oscillator sub-chart).

The shares may have support composed of 38.2% (221p) of VOD’s 11th February-20th April advance, even if a potentially much stricter Fibonacci interval (61.8%: 235p) is overhead; it’s from the share’s more memorable slide from June 2015 highs.

In the slightly longer term, developing triangulation should settle the market’s ‘discussion’, if it results in breakout. That may conclude negotiation around the c. 230p level, with a setback for bulls to at least 212p, or a boost that’s strong enough to surpass peaks for the year so far on 20th April (236p).

All told though, those inclined to buy can probably do better than current prices.

Please click image to enlarge