Utility shares bounce in post election relief rally

In theory, now that much uncertainty over the UK stock market is likely to pass, following an unexpectedly large share of the vote for the […]

In theory, now that much uncertainty over the UK stock market is likely to pass, following an unexpectedly large share of the vote for the […]

In theory, now that much uncertainty over the UK stock market is likely to pass, following an unexpectedly large share of the vote for the Conservatives, many market sectors that were sold-off severely in the run-up to last night’s election could bounce.

In practice of course, many of their recoveries will depend on factors unrelated to their sectors.

Here is a list of the ten worst-performing stocks in the UK’s broad FTSE 350 index over the last 3 months.

| COMPANY | LAST PRICE | 1-DAY CHG (%) | 1D NET CHG | PREV CLOSE | 3-MTH % FALL | SECTOR |

| BWIN.PARTY | 86.95 | 2.656 | 2.25 | 84.7 | -16% | Consumer discretionary/online services |

| IP GROUP | 212 | 4.418 | 9 | 203.7 | -17% | Financials/investment |

| BK OF GEORGIA | 1818 | 0.664 | 12 | 1806 | -17.3% | Financials |

| HIKMA | 2005 | 2.036 | 40 | 1965 | -19.7% | Pharmaceutical |

| POUNDLAND | 322.1 | 3.303 | 10.3 | 311.8 | -23.8% | Consumer discretionary/retail |

| IMAGINATION | 198 | 2.222 | 4.3 | 193.5 | -23.9% | IT |

| N BROWN | 337 | 2.988 | 9.8 | 328 | -27% | Consumer discretionary/retail |

| SOCO INTL | 193 | 2.754 | 5.2 | 188.8 | -33% | Energy/oil & gas Production |

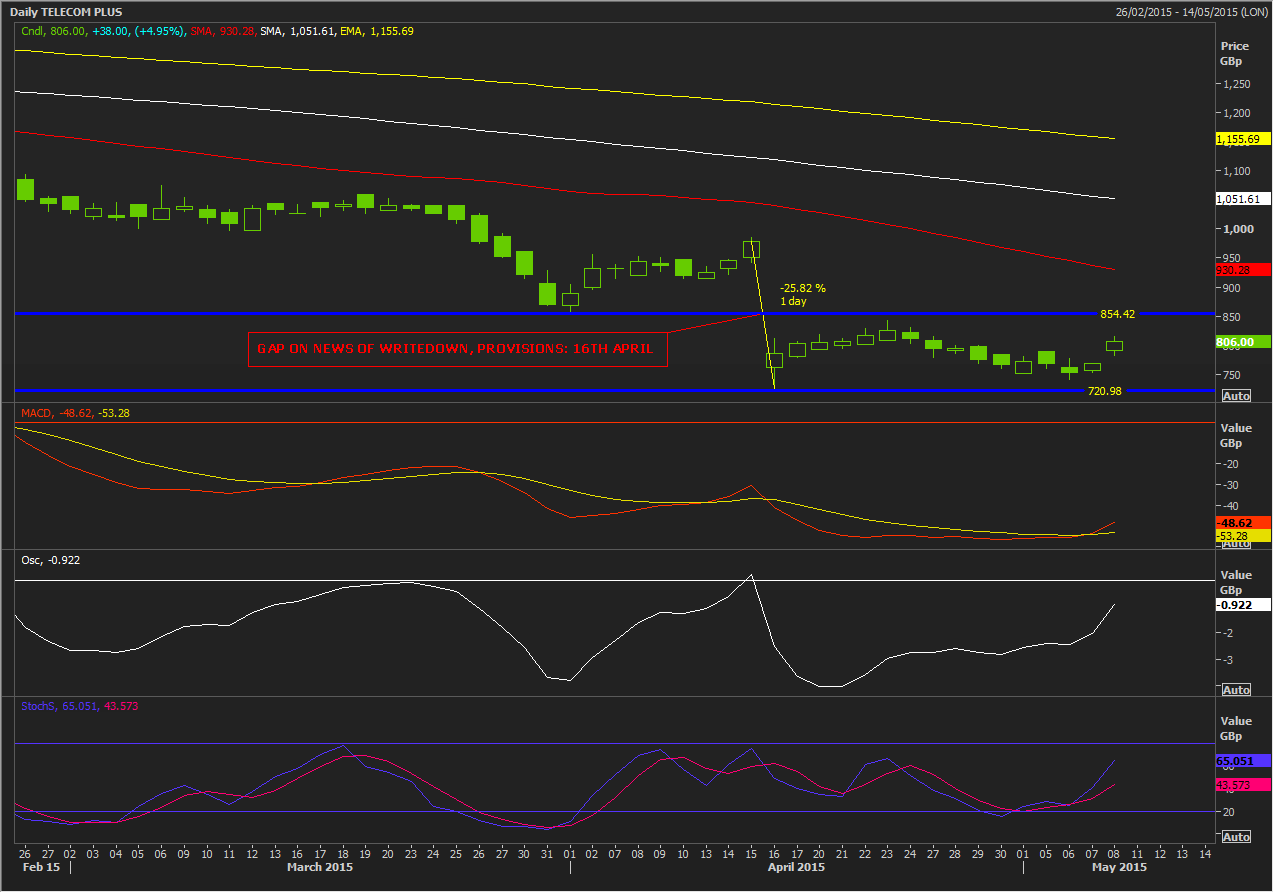

| TELECOM PLUS | 802 | 4.427 | 34 | 768 | -34.8% | Utilities |

| AO WORLD | 173 | 1.941 | 3.3 | 170 | -47% | Consumer discretionary/retail |

For instance, online electrical appliances retailer AO World, which has lost the better part of 50% over the last three months, still appears to face a challenging year.

The firm claimed it had been the “victim” of an overhyped float in 2014 and subsequently downgraded full-year profit forecasts in February.

Last month its chairman, Richard Rose, sold 89% of his shares.

The company now has a market value of £715m compared with £1.6 billion at its peak soon after it listed in February.

A closer representative of a larger sector that fell out of favour ahead of the election is utility Telecom Plus.

But even this small UK-based, telephone, gas and electricity services provider has a story of its own which has weighed on its shares.

It supplies 500,000 customers in the UK working with around 40,000 independent distributors who gain commission from their own customers and customers of their secondary distributors.

This makes the Telecom Plus perhaps the only utility that operates by a multi-level marketing model.

Whilst it once garnered plaudits from independent consumer groups for the quality of its service, it has latterly faced tougher times.

On 16th April it was forced to write off millions of pounds in unpaid bills and set aside further millions as provisions to cover leakage and theft of gas.

It was the effect of Telecom Plus shares having performed so badly that skewed the 3-month total for the rest of the UK utilities sector, even though its small size and unusual operational structure mean it is hardly representative of the large UK listed utilities.

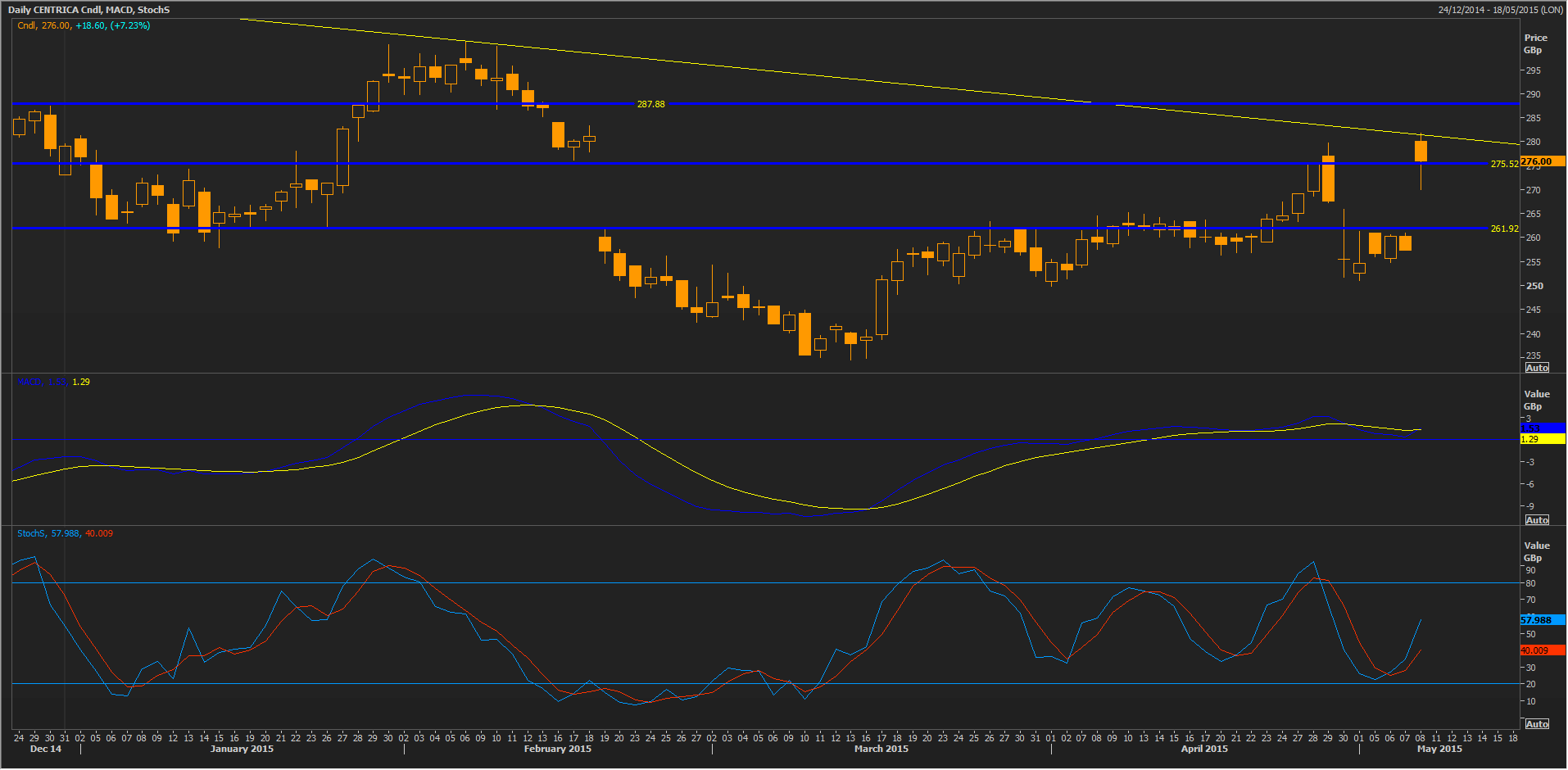

Whilst shares of Centrica Plc., United Utilities, Severn Trent have certainly underperformed the wider market spanning the range between a rise of 4% to a fall of 13%, none lost anywhere near as much as the 35% collapse of Telecom Plus stock.

| COMPANY | LAST PRICE | 1-DAY CHG (%) | 1D NET CHG | PREV CLOSE | 3-MTH % FALL |

| DRAX GROUP | 413.5 | +3.8 | +15 | 386.6 | +4% |

| PENNON GROUP | 880 | +3.1 | +26.5 | 853.5P | +0.65% |

| SEVERN TRENT | 2132 | +3.2% | +66 | 2066 | -1.4% |

| SCOTTISH & SOUTHERN | 1643.25 | +5.1 | +80 | 1564 | -3.9% |

| UNITED UTILITIES | 989 | +4% | +38 | 951 | -4.3% |

| NATIONAL GRID | 896.2 | +2.9% | +25 | 870 | -4.3% |

| INFINIS ENERGY | 189 | 0% | 0 | 189 | -5.4% |

| CENTRICA | 277.4 | +7.8% | +20 | 257.4 | -13% |

| TELECOM PLUS | 802 | 4.427 | 34 | 768 | -34.8% |

Centrica had already rallied more than 20% this year despite a multi-whammy hit in February from the oil price fall (it is also an oil & gas producer) legal penalties and of course, the expectation of deeper regulatory scrutiny that led it to slash its dividend.

Ahead of the election, the fear that the Labour Party might be able to enact its manifesto pledge to Freeze energy bills until 2017 and give the energy regulator new powers to cut bills, was one of the few which appeared to be clearly manifested in a sector’s shares.

Regulatory caps on revenue were already evident on return on asset profiles of most large utilities that operate in the UK, with Centrica’s a meagre 3% on a trailing 12-month basis, close to that of water utility Severn Trent, but below its peer Pennon, which managed 4%, and United Utilities on 7.1%.

With the overhang implied by the risk of further effective caps to revenues now removed from the sector, the diversified revenue streams and assets of many of this group, especially United Utilities, might now begin to be priced back in.