The last key event for this week will be Fed Chair Powell’s speech on Fri, 23 Aug during the Jackson Hole Symposium at 1400 GMT where market participants will look for clues on the latest Fed’s guidance towards its monetary policy.

There is another significant “theatrical play” that is unfolding in the financial markets right now is the movement of USD/CNH (offshore yuan) that is creeping up slowly from its 13 Aug 2019 low of 6.9900. Recall what happen on 05 Aug 2019? On that fateful day, the China central bank, PBOC has allowed the USD/CNH to breach above the key psychological level of 7.00 to counter the latest 10% U.S. tariffs imposed on China’s products that has led to a domino effect on global risk assets where we have witnessed a synchronised sell-off in stocks (click here for a recap on our previous report).

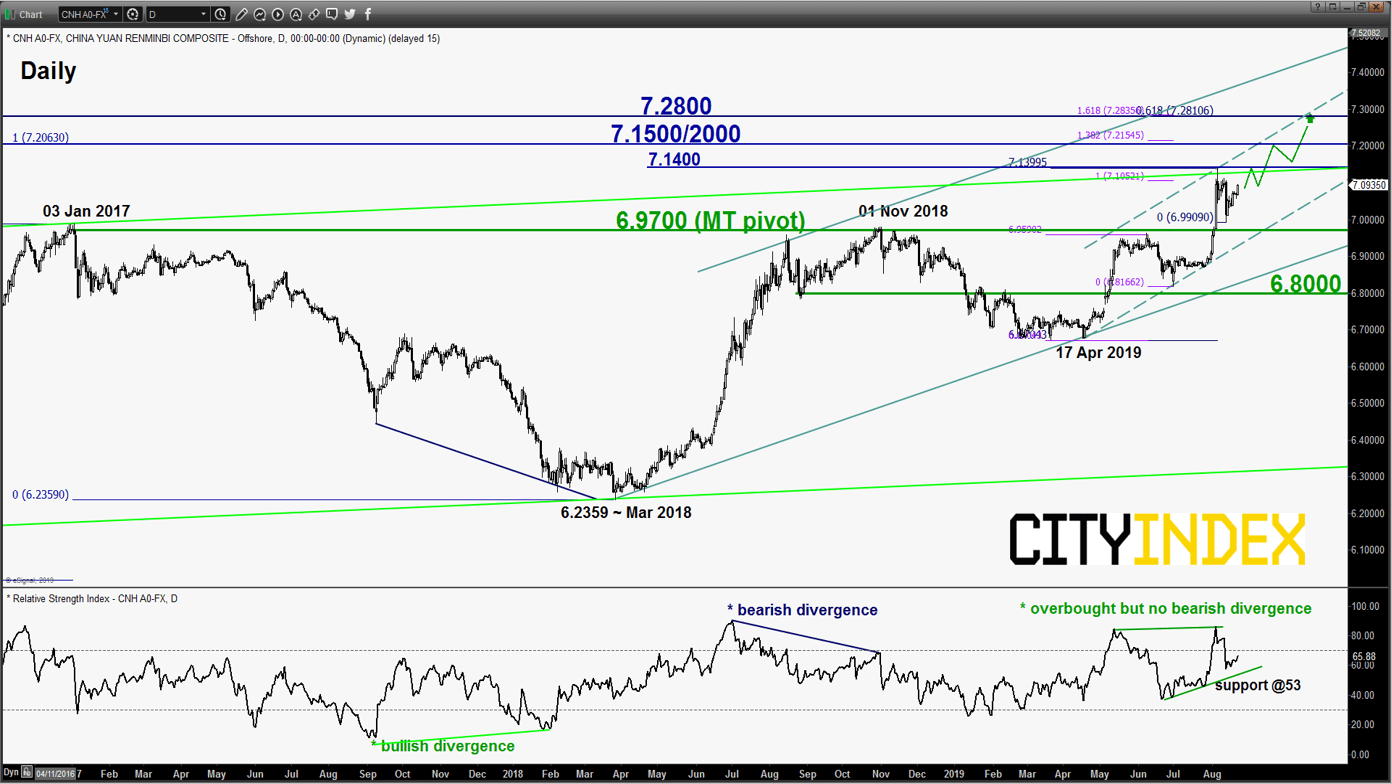

Right now, technical elements are turning positive again for USD/CNH.

USD/CNH – Upside momentum has resurfaced

click to enlarge chart

Key Levels (1 to 3 months)

Pivot (key support): 6.9700

Resistances: 7.1500/2000 & 7.2800

Next support: 6.8000

Directional Bias (1 to 3 months)

Bullish bias as the recent 2-weeks of corrective decline sequence in place since 06 Aug 2019 high area of 7.15 may have ended. If the 6.9700 key medium-term pivotal support holds, USD/CNH is likely to resume another round of potential impulsive upleg sequence to target the next resistance at 7.1500/2000 follow by 7.2800 next. On the other hand, a break with a daily close below 6.9700 invalidates the bullish scenario for a deeper corrective decline towards the next support at 6.8000 (also close to the primary ascending channel support in place since Mar 2018 low).

Key elements

- There is no bearish divergence seen in the daily RSI oscillator even though it has hit an overbought condition on 05 Aug 2019 versus a prior bearish divergence signal that has formed in 30 Oct 2018 that led to a significant decline in the price action of USD/CNH.

- The above-mentioned observations on the daily RSI suggest that medium-term upside momentum has resurfaced for USD/CNH.

- The significant medium-term resistances stand at 7.1500/2000 and 7.2800 which are defined by the upper boundary of the medium-term ascending channel in place since 17 Apr 2019 low and Fibonacci expansion clusters.

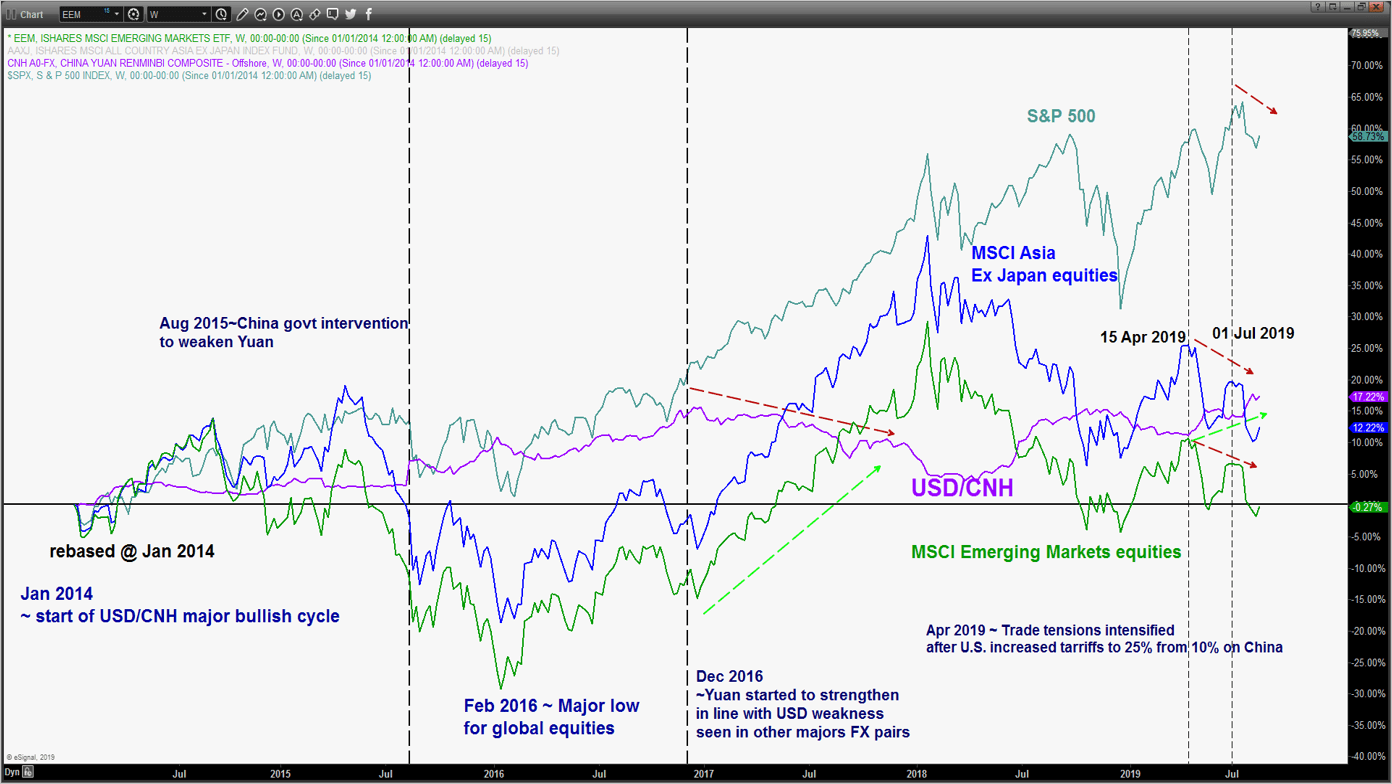

A strong USD/CNH is not good for Asia ex Japan & emerging markets equities and even S&P 500

click to enlarge chart

- Since the shock devaluation of the Chinese Yuan in Aug 2015, the movement of the USD/CNH has a significant negative correlation with the MSCI Asia Ex Japan and MSCI Emerging markets stock indices. Based on past observations, a rally in USD/CNH tends to lead to an opposite movement (a decline) in the MSCI Asia Ex Japan and MSCI Emerging markets stock indices. On the reverse, a decline in USD/CNH is likely to see an upward movement in the MSCI Asia Ex Japan and MSCI Emerging markets stock indices.

- Since Apr 2019, the USD/CNH has been on a “slow upward” trajectory which has added downside pressure in Asia Ex Japan and Emerging Markets equities.

- The S&P 500 has started to catch the “flu bug” from a strong USD/CNH. Since its all-time high printed in July 2019, the Index has declined in line with an upward movement seen in the USD/CNH.

Therefore, stock traders should start to pay very close attention to the movement of USD/CNH at this juncture.

Charts are from eSignal

Latest market news

Today 08:18 AM

Yesterday 10:40 PM

Latest Indices articles

April 18, 2024 04:46 PM

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM