USD SEK Post Riksbank bounce only lasted a SEK

Global markets went into a panic overnight as oil (WTI) took a tumble all the way down to the lower-26.00s, USD/JPY collapsed below 111.00 before […]

Global markets went into a panic overnight as oil (WTI) took a tumble all the way down to the lower-26.00s, USD/JPY collapsed below 111.00 before […]

Global markets went into a panic overnight as oil (WTI) took a tumble all the way down to the lower-26.00s, USD/JPY collapsed below 111.00 before an apparent “rate check” by the BOJ, and gold soared to 1240. Meanwhile, lost in the admittedly exciting roller coaster ride of volatility, the world’s oldest central bank surprised traders by cutting interest rates deeper into oversold territory.

In today’s European session, Sweden’s Riksbank lowered its main repurchase rate to -0.5% from -0.35% in an effort to incentivize banks to lend more money out, rather than keep funds as deposits. The central bank also opted to leave its quantitative easing program unchanged at 200B kronor. In justifying the decision, the Riksbank statement noted that “The upturn in inflation is still not on a firm footing, as is illustrated by the unexpectedly weak outcomes in recent months” and warned that there was “still scope to cut the repo rate further” if required.

While hardly out of the blue, this was a more aggressive move than many traders and analysts expected; out of the 11 analysts surveyed by the Wall Street Journal before the decision, six anticipated some sort of cut, though only two forecast that we’d see the 15bps cut that actually came to pass. Even within the central bank’s monetary policy board, two of the six members voted against the decision in favor of leaving interest rates unchanged. In addition to the rate cut, the Riksbank also updated its economic forecasts. The central bank now expects consumer price inflation to rise at only a 0.7% rate this year, down from the previous forecast of 1.3% and well below the bank’s 2% inflation target.

Market Reaction: Only lasted a SEK…

The market’s initial reaction to the extremely dovish decision and outlook was, not surprisingly, to sell the Swedish krone aggressively. However, that move was relatively short-lived and as of writing, the krone has recovered to trade essentially unchanged against both the euro and the US dollar.

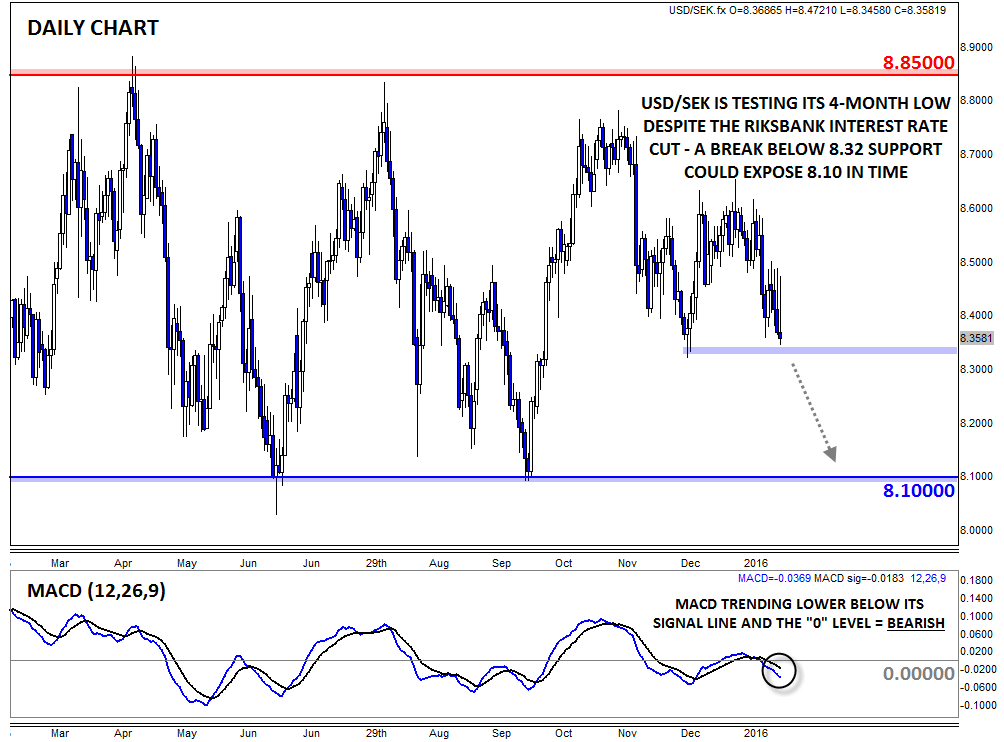

Looking at the longer-term view for USD/SEK, rates are holding within the middle of the broad sideways range from 8.10 up to 8.85 that has contained rates for fully 13 months. Given the short-lived nature of today’s spike and general dollar weakness of late, we wouldn’t be surprised to see USD/SEK drop below its 4-month low in the 8.32 region and potential head back down to revisit support in the lower 8.00s as we move through the rest of Q1. On the other hand, a bounce from the 8.32 support zone could lead to a short-term bounce back into the mid-8.00s, but we remain skeptical that the pair will retest the top of its range in the upper-8.00s any time soon.