The US Dollar was bullish against most of its major pairs on Friday with the exception of the GBP. On Monday, Markit's US Manufacturing Purchasing Managers' Index for the October final reading is expected to remain at 53.3 on month, in line with the October preliminary reading. Finally, Construction Spending for September is expected to rise 0.9% on month, compared to +1.4% in August.

The Euro was bearish against all of its major pairs. In Europe, the European Commission has posted Eurozone's 3Q GDP at -4.3% (vs -8.0% on month expected), October CPI at +0.2% (vs +0.2% on month expected) and September jobless rate at 8.3% (vs 8.2% expected). The German Federal Statistical Office has released 3Q GDP at +8.2% (vs +7.2% on quarter expected) and September retail sales at -2.2% (vs -0.6% on month expected). France's INSEE has reported 3Q GDP at +18.2% (vs +15.1% on quarter expected) and October CPI at -0.1% (vs +0.2% on month expected). In the U.K., the Nationwide Building Society has posted its House Price Index for October at (vs +0.4% on month expected).

The Australian dollar was bullish against most of its major pairs with the exception of the GBP.

On last week's U.S. economic data front:

Personal Income rose 0.9% on month in September (+0.4% expected), compared to a revised -2.5% in August. Personal Spending increased 1.4% on month in September (+1.0% expected), compared to +1.0% August.

Market News International's Chicago Business Barometer slipped to 61.1 on month in October (58.0 expected), from 62.4 in September.

The University of Michigan's Consumer Sentiment Index advanced to 81.8 on month in the October final reading (81.2 expected), from 81.2 the October preliminary reading.

Initial Jobless Claims fell to 751K for the week ending October 24th (770K expected), from a revised 791K in the week before. Continuing Claims declined to 7,756K for the week ending October 17th (7,775K expected), from a revised 8,465K in the prior week. GDP surged to +33.1% on quarter for the third quarter advanced reading (+32.0% expected), from -31.4% in the second quarter third reading, marking an all-time high.

Pending Home Sales slipped 2.2% on month in September (+2.9% expected), compared to +8.8% in August. The Mortgage Bankers Association's Mortgage Applications rose 1.7% for the week ending October 23rd, compared to -0.6% in the previous week. New Home Sales unexpectedly fell to 959K on month in September (1,025K expected), from a revised 994K in August.

Wholesale Inventories fell 0.1% on month in the September preliminary reading (+0.4% expected), compared to a revised +0.3% in the August final reading. Durable Goods Orders jumped 1.9% on month in the September preliminary reading (+0.5% expected), compared to a revised +0.4% in the August final reading.

Finally, The Conference Board's Consumer Confidence Index unexpectedly declined to 100.9 on month in October (102.0 expected), from a revised 101.3 in September.

This week's biggest moving major pairs were the EUR/USD which closed down 210 pips and the USD/CAD which gained 199 pips.

Looking at the EUR/USD, the pair remains in a holding pattern between 1.202 resistance and 1.1605 support with a bias to the upside.

Source: GAIN Capital, TradingView

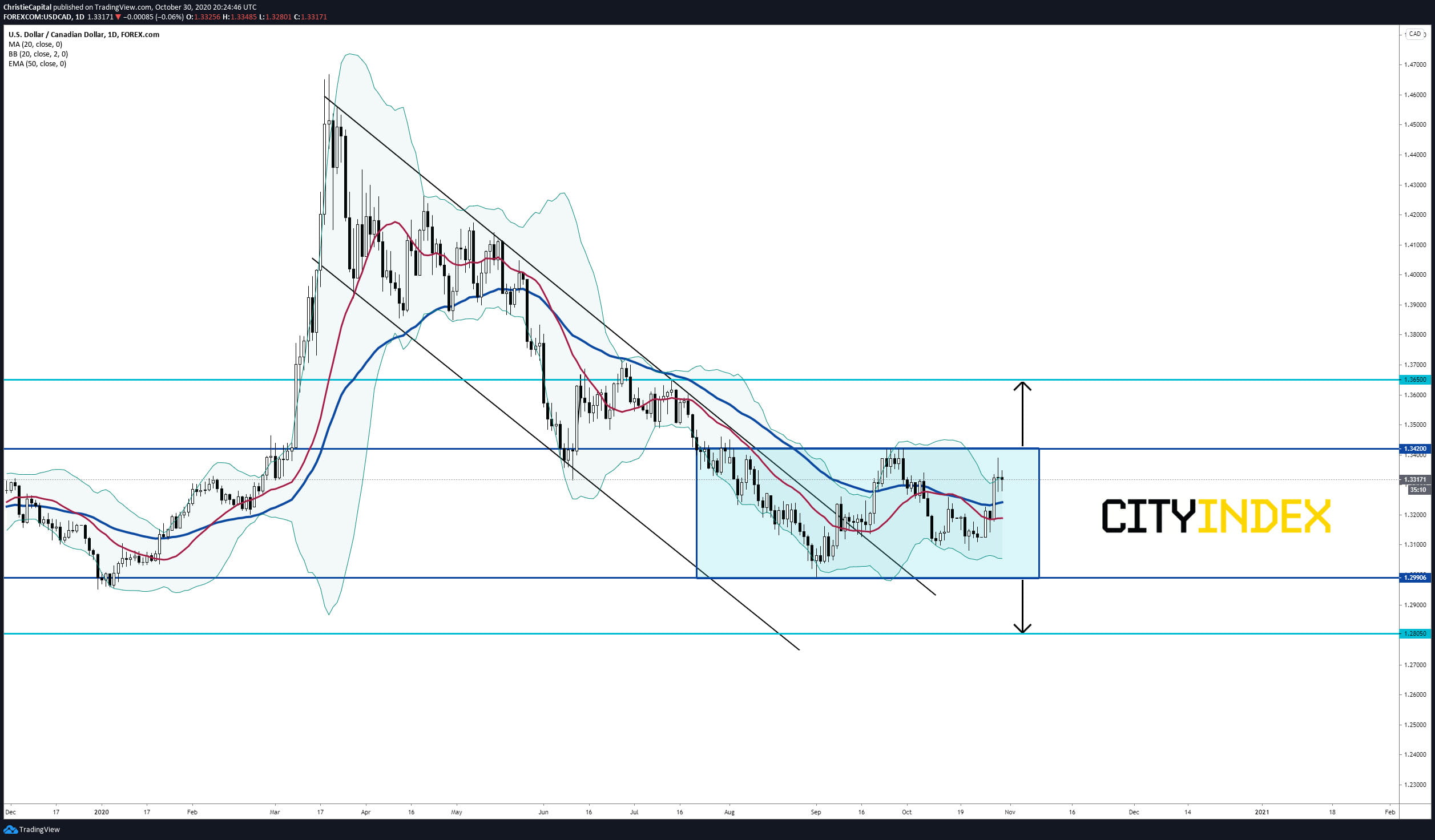

The USD/CAD also remains in a consolidation zone between 1.342 resistance and 1.30 support. The bias is to resume the prior trend lower if a break below 1.30 takes place.

Source: GAIN Capital, TradingView

Have a great weekend.

The Euro was bearish against all of its major pairs. In Europe, the European Commission has posted Eurozone's 3Q GDP at -4.3% (vs -8.0% on month expected), October CPI at +0.2% (vs +0.2% on month expected) and September jobless rate at 8.3% (vs 8.2% expected). The German Federal Statistical Office has released 3Q GDP at +8.2% (vs +7.2% on quarter expected) and September retail sales at -2.2% (vs -0.6% on month expected). France's INSEE has reported 3Q GDP at +18.2% (vs +15.1% on quarter expected) and October CPI at -0.1% (vs +0.2% on month expected). In the U.K., the Nationwide Building Society has posted its House Price Index for October at (vs +0.4% on month expected).

The Australian dollar was bullish against most of its major pairs with the exception of the GBP.

On last week's U.S. economic data front:

Personal Income rose 0.9% on month in September (+0.4% expected), compared to a revised -2.5% in August. Personal Spending increased 1.4% on month in September (+1.0% expected), compared to +1.0% August.

Market News International's Chicago Business Barometer slipped to 61.1 on month in October (58.0 expected), from 62.4 in September.

The University of Michigan's Consumer Sentiment Index advanced to 81.8 on month in the October final reading (81.2 expected), from 81.2 the October preliminary reading.

Initial Jobless Claims fell to 751K for the week ending October 24th (770K expected), from a revised 791K in the week before. Continuing Claims declined to 7,756K for the week ending October 17th (7,775K expected), from a revised 8,465K in the prior week. GDP surged to +33.1% on quarter for the third quarter advanced reading (+32.0% expected), from -31.4% in the second quarter third reading, marking an all-time high.

Pending Home Sales slipped 2.2% on month in September (+2.9% expected), compared to +8.8% in August. The Mortgage Bankers Association's Mortgage Applications rose 1.7% for the week ending October 23rd, compared to -0.6% in the previous week. New Home Sales unexpectedly fell to 959K on month in September (1,025K expected), from a revised 994K in August.

Wholesale Inventories fell 0.1% on month in the September preliminary reading (+0.4% expected), compared to a revised +0.3% in the August final reading. Durable Goods Orders jumped 1.9% on month in the September preliminary reading (+0.5% expected), compared to a revised +0.4% in the August final reading.

Finally, The Conference Board's Consumer Confidence Index unexpectedly declined to 100.9 on month in October (102.0 expected), from a revised 101.3 in September.

This week's biggest moving major pairs were the EUR/USD which closed down 210 pips and the USD/CAD which gained 199 pips.

Looking at the EUR/USD, the pair remains in a holding pattern between 1.202 resistance and 1.1605 support with a bias to the upside.

Source: GAIN Capital, TradingView

The USD/CAD also remains in a consolidation zone between 1.342 resistance and 1.30 support. The bias is to resume the prior trend lower if a break below 1.30 takes place.

Source: GAIN Capital, TradingView

Have a great weekend.

Latest market news

Today 08:18 AM

Yesterday 10:40 PM

Latest CAD articles

March 23, 2023 07:33 PM

March 13, 2023 02:54 PM

February 21, 2023 02:21 PM

February 17, 2023 04:05 PM