USD JPY traders venturing out from safe haven harbours

“A ship in harbor is safe, but that is not what ships are built for.” – John A. Shedd For the last couple of weeks, […]

“A ship in harbor is safe, but that is not what ships are built for.” – John A. Shedd For the last couple of weeks, […]

“A ship in harbor is safe, but that is not what ships are built for.” – John A. Shedd

For the last couple of weeks, threatening storm clouds emanating from Greece and China have prompted speculators to keep their “ships” (capital) protected in “harbour” (safe-haven currencies). With today’s news that Greece and its creditors were able to pound out a deal in all-night emergency talks and the continued stability in China’s stock market, traders are finally starting to see the sun peeking through the storm clouds. As a result, traditional safe haven currencies like the Japanese yen are on the back foot heading into today’s US trading session.

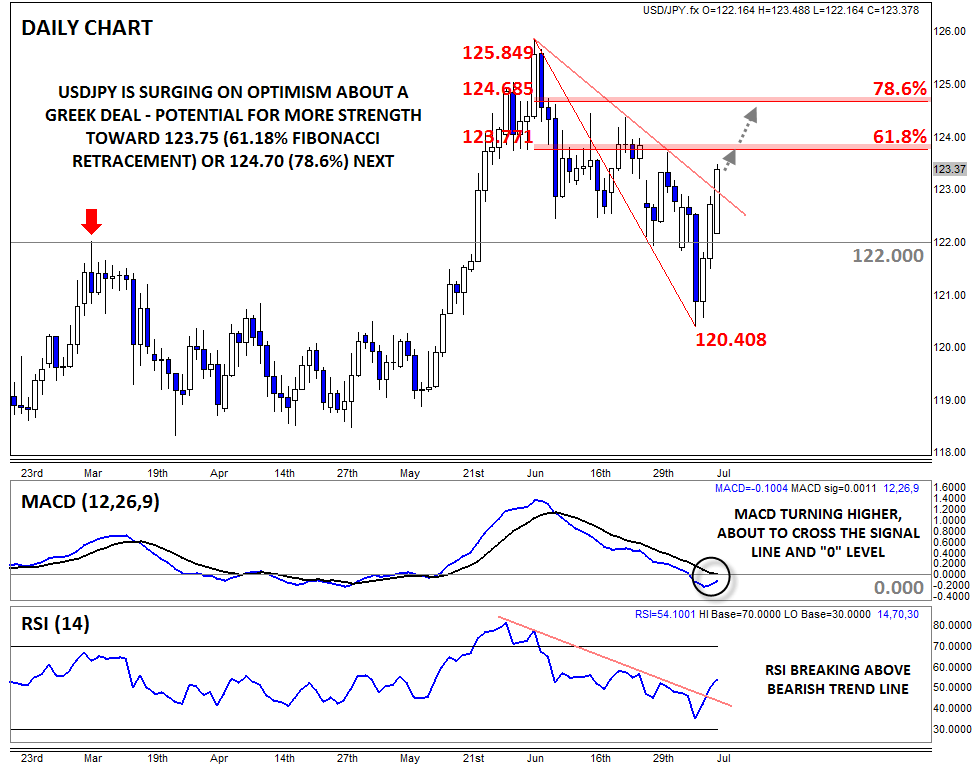

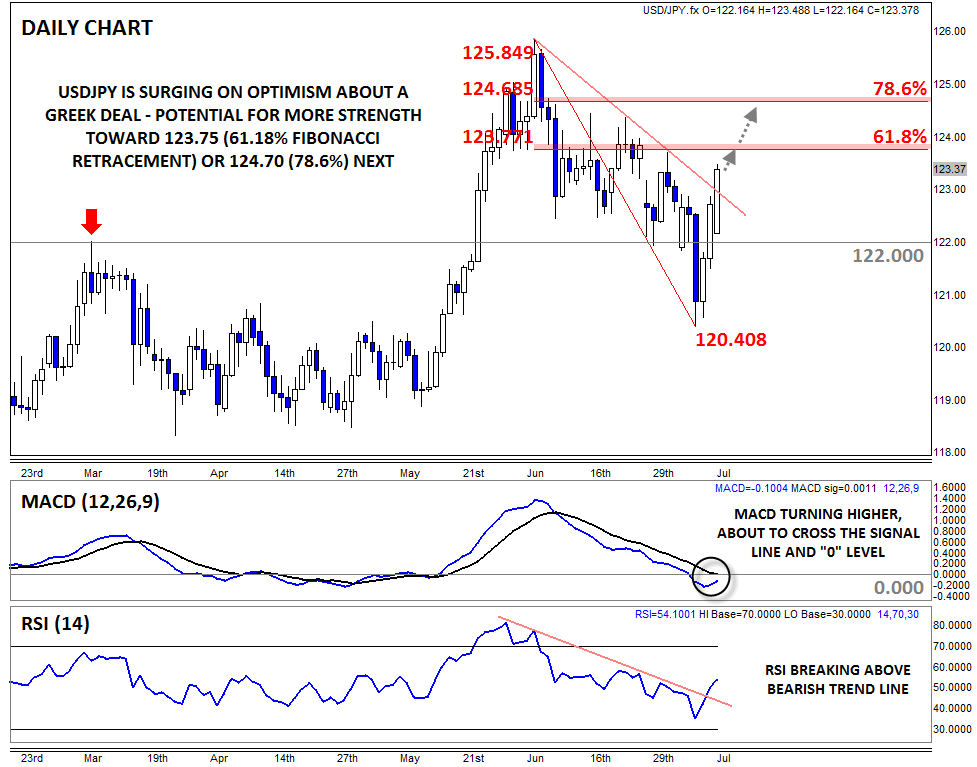

Looking at USD/JPY specifically, rates have surged all the way up to 123.50, fully 300 pips from Wednesday’s “peak Grexit panic” trough under 120.50. More notably, the pair has edged above the bearish trend line off the early June high at 125.85, showing a change in the generally bearish sentiment that has dominated over the last five weeks. At the same time, the secondary indicators are showing signs of improving: the MACD is turning higher and about to cross both the “0” level and its signal line, while the RSI indicator has conclusively broken its own bearish trend line.

Of course, today’s optimistic market sentiment remains fragile; any setback in the approval of the Greek debt deal or a resumption of bearish momentum in China’s stock market could bring back the safe-haven bid for yen. That said, the current technical outlook on USD/JPY is bullish for a possible continuation up to 123.75 or 124.70, the 61.8% and 78.6% Fibonacci retracements of the recent pullback respectively.

Beyond general risk appetite, there are a number of US- and Japan-specific economic announcements to monitor this week (all times GMT):

{kind=link}