USD JPY heads back down on sliding stocks and oil

USD/JPY began to retreat again on Thursday as crude oil prices failed to maintain recent gains and stock markets felt renewed pressure after nearly a […]

USD/JPY began to retreat again on Thursday as crude oil prices failed to maintain recent gains and stock markets felt renewed pressure after nearly a […]

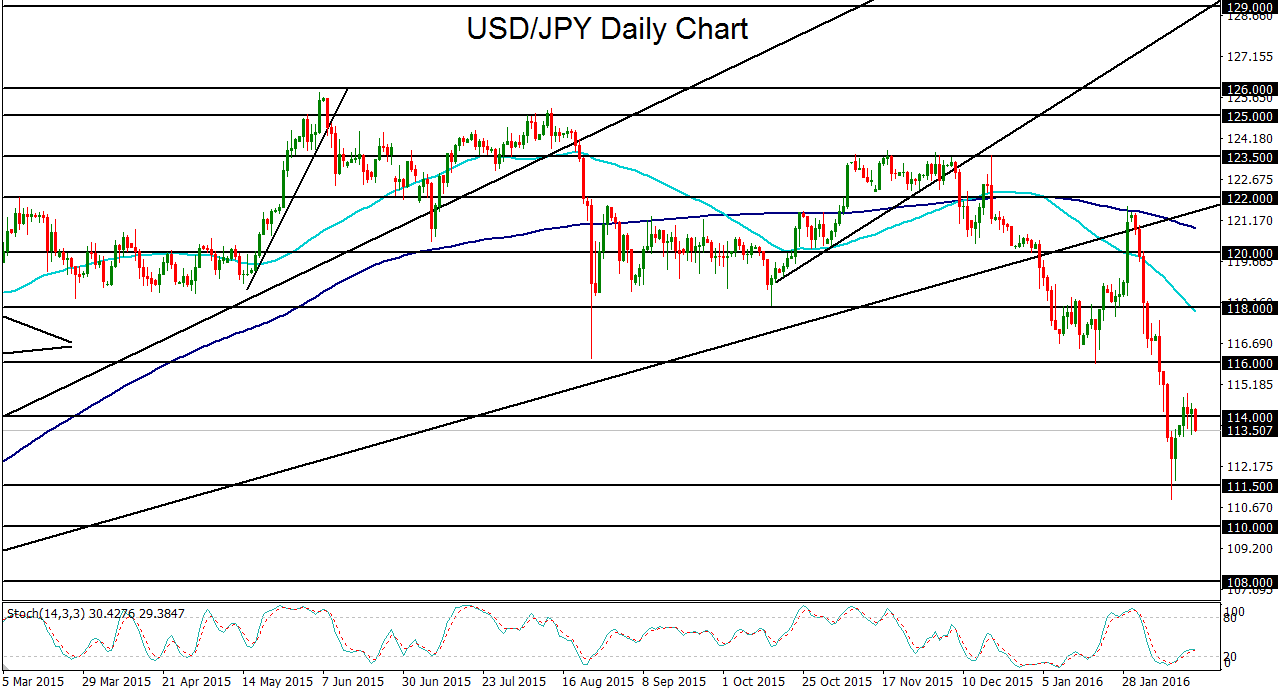

USD/JPY began to retreat again on Thursday as crude oil prices failed to maintain recent gains and stock markets felt renewed pressure after nearly a week of sharp recovery.

Equity markets were weighed down Thursday as crude oil suffered a blow from US Energy Information Administration data reporting that crude inventory rose by 2.1 million barrels last week, which was less than expected but refuted an earlier report of a sizable draw in inventories.

With stock market fluctuations having recently followed crude oil prices closely, and the Japanese yen continuing to benefit from its safe haven status when equity markets fall, USD/JPY retreated further from this week’s 114.86 high to drop below the key 114.00 level once again. Yen strength took center stage in this USD/JPY retreat on Thursday, as the US dollar was relatively flat.

From a broader price perspective, USD/JPY spent most of the first half of February plunging precipitously from above 121.00 all the way down to a new long-term low below 111.00, largely due to falling crude oil and stock markets fostering a “risk-off” flight back to the safe havens of gold and the yen.

Though equities have since recovered most of the losses from earlier in the month, any major return of market volatility may likely boost the yen even further, which could send USD/JPY to new lows. Declines for the currency pair could be even further pronounced if the US Federal Reserve continues to be seen as increasingly dovish and unlikely to raise interest rates again this year, which could further weigh on the US dollar.

In this event, sustained pressure under the noted 114.00 level could begin to target further downside objectives at the key 110.00 and 108.00 support levels.