USD JPY falters amid safe haven yen strength

USD/JPY initially surged on Thursday morning as the safe-haven yen pulled back on well-supported equity markets and hopes for a long-awaited OPEC deal to limit […]

USD/JPY initially surged on Thursday morning as the safe-haven yen pulled back on well-supported equity markets and hopes for a long-awaited OPEC deal to limit […]

USD/JPY initially surged on Thursday morning as the safe-haven yen pulled back on well-supported equity markets and hopes for a long-awaited OPEC deal to limit oil production and stabilize crude oil prices. This calm would not last into afternoon trading, however, as doubts about the solidity of the oil deal emerged and financial stocks took a hit due to fall-out from Deutsche Bank’s woes. These concerns helped pressure equity markets, boosting the safe-haven yen and weighing on USD/JPY once again.

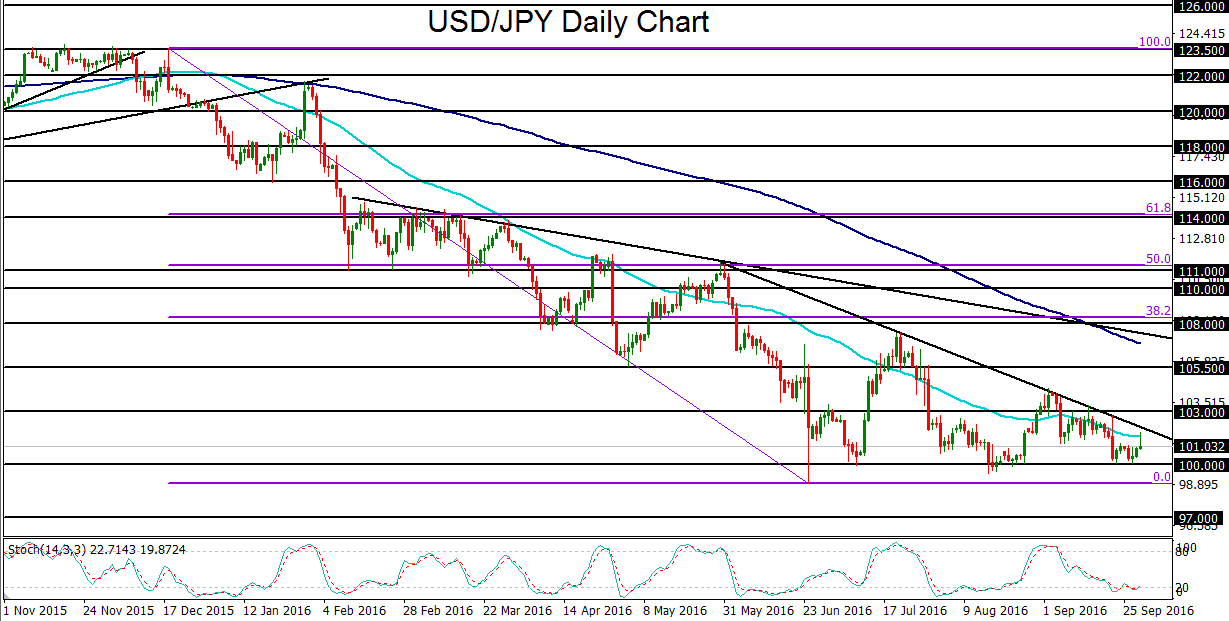

The past few days this week have seen a clean rebound for USD/JPY off the major support area around 100.00. This level has served as key technical and psychological support since June’s brief post-Brexit dip below 100.00. Thursday’s initial surge provided some hope for a continuation of the recent USD/JPY rebound off this level, but the yen’s incessant strength continued to weigh on the currency pair.

With key risk conditions on the horizon, including the US presidential elections, new developments in the battered banking sector, and further details regarding the reported OPEC oil agreement, USD/JPY could be subject to significantly more upcoming volatility.

USD/JPY continues to be entrenched in a clear bearish trend from both long-term and short-term perspectives. The currency pair is currently following a clear descending trend line extending back from late-May’s 111.00-area highs. With any exacerbation of market risk factors, the yen could rise even further, potentially pressuring USD/JPY below the 100.00 level and towards the next major downside support targets at 97.00 and 95.00.