USD JPY drops as dollar pulls back and equities extend slide

USD/JPY dropped well below the 120.00 level on Thursday morning as the dollar pulled back, stocks extended their slide, and gold continued to surge. Increased […]

USD/JPY dropped well below the 120.00 level on Thursday morning as the dollar pulled back, stocks extended their slide, and gold continued to surge. Increased […]

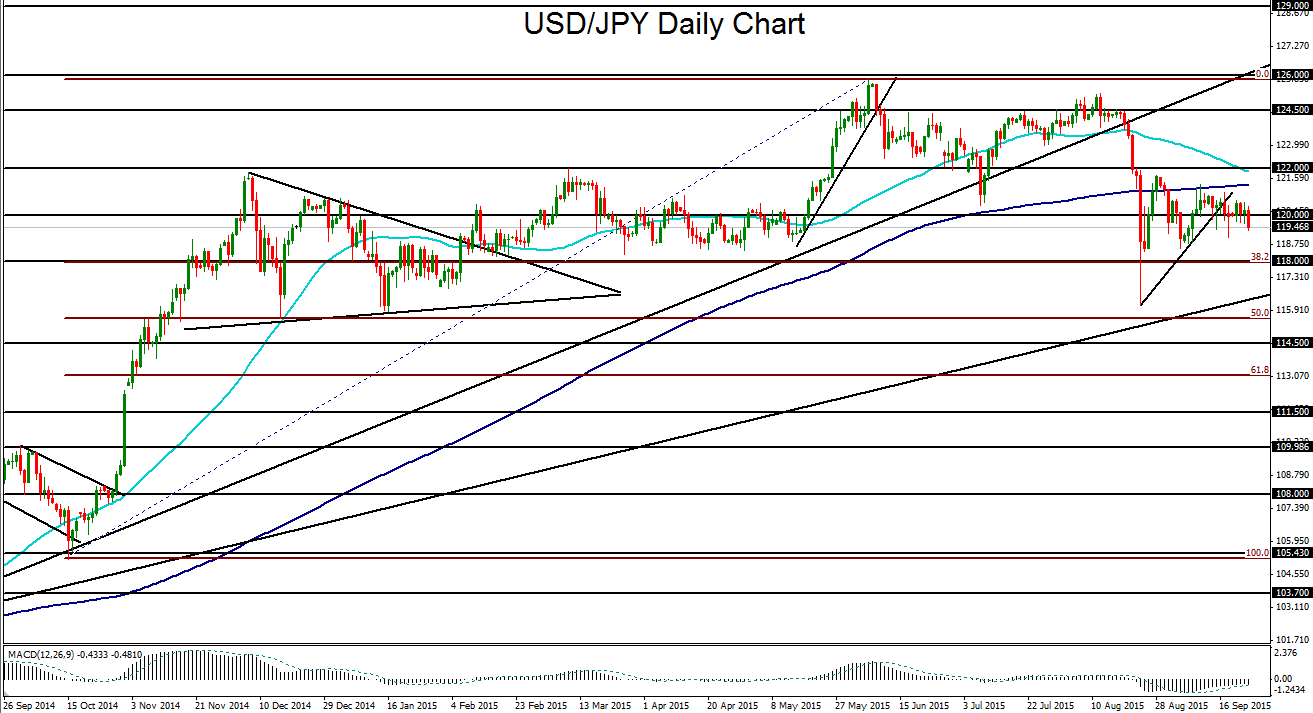

USD/JPY dropped well below the 120.00 level on Thursday morning as the dollar pulled back, stocks extended their slide, and gold continued to surge.

Increased anxiety and uncertainty in the markets have contributed to a flight towards traditional “safe haven” assets like gold and the Japanese yen, while stock markets continue to get pummeled. Investors eagerly awaited a speech on inflation by Fed Chair Janet Yellen later in the day on Thursday, which could potentially provide some clues as to the timing of an initial rate hike in the US.

The dollar pullback combined with increased yen buying pressured USD/JPY back down towards the 119.00 level, which was last approached late last week.

While any further hints of a Fed rate hike this year should continue to support the dollar in the short-term, any continued trouble in global equity markets could lead to more yen buying and a resulting plunge for USD/JPY. This occurred in late August when stock markets plummeted over a period of just a few days, sending USD/JPY tumbling down with them.

Last week, the currency pair broke down below a large triangle consolidation pattern that had been in place since after the noted August plunge.

Any continued fear over the global economy as reflected in the equity markets has the potential to place further pressure on USD/JPY as a flight-to-safety mentality potentially continues.

As the currency pair is currently trading well below the 120.00 level, any significant continuation of market volatility could prompt USD/JPY to fall back towards the 118.00 support level, with a further near-term breakdown targeting the 115.50 support objective.