USD JPY disparity between US and Japanese policies grow

It has been a relatively quiet day so far as investors await the 13:30 GMT release of US Consumer Price Index. The CPI is expected […]

It has been a relatively quiet day so far as investors await the 13:30 GMT release of US Consumer Price Index. The CPI is expected […]

It has been a relatively quiet day so far as investors await the 13:30 GMT release of US Consumer Price Index. The CPI is expected to have increased to 1.6% year-over-year in October from 1.5% the month before, while core CPI is seen steady at 2.2%. We’ll also have a few other second-tier US macro pointers and Fed’s Janet Yellen will have her testimony later. The market appears almost certain that a US rate will be forthcoming next month: according to the CME’s FedWatch tool, a December rate hike is around 90% likely now. That view is not likely change today, unless the inflation figures disappoint expectations really badly or Yellen delivers surprisingly dovish remarks – both unlikely in my view.

While the dollar rally could extend far beyond anyone’s imaginations one has to consider the possibility that a rate rise is priced in now. If so, the dollar could at the very least pause for breath. However, it is not just about December. The market will want to know what will happen afterwards. Looking around, nearly all other major central banks are still dovish, not least the Bank of Japan. Overnight, the BOJ announced that it would be snapping up an unlimited amount of five-year and two-year bonds at fixed rates in the wake of the global bond market sell-off. The Japanese central bank is keen to cap the 10-year yield at or around zero. Thus, the BoJ remains pretty much dovish as the Fed grows more hawkish by the day.

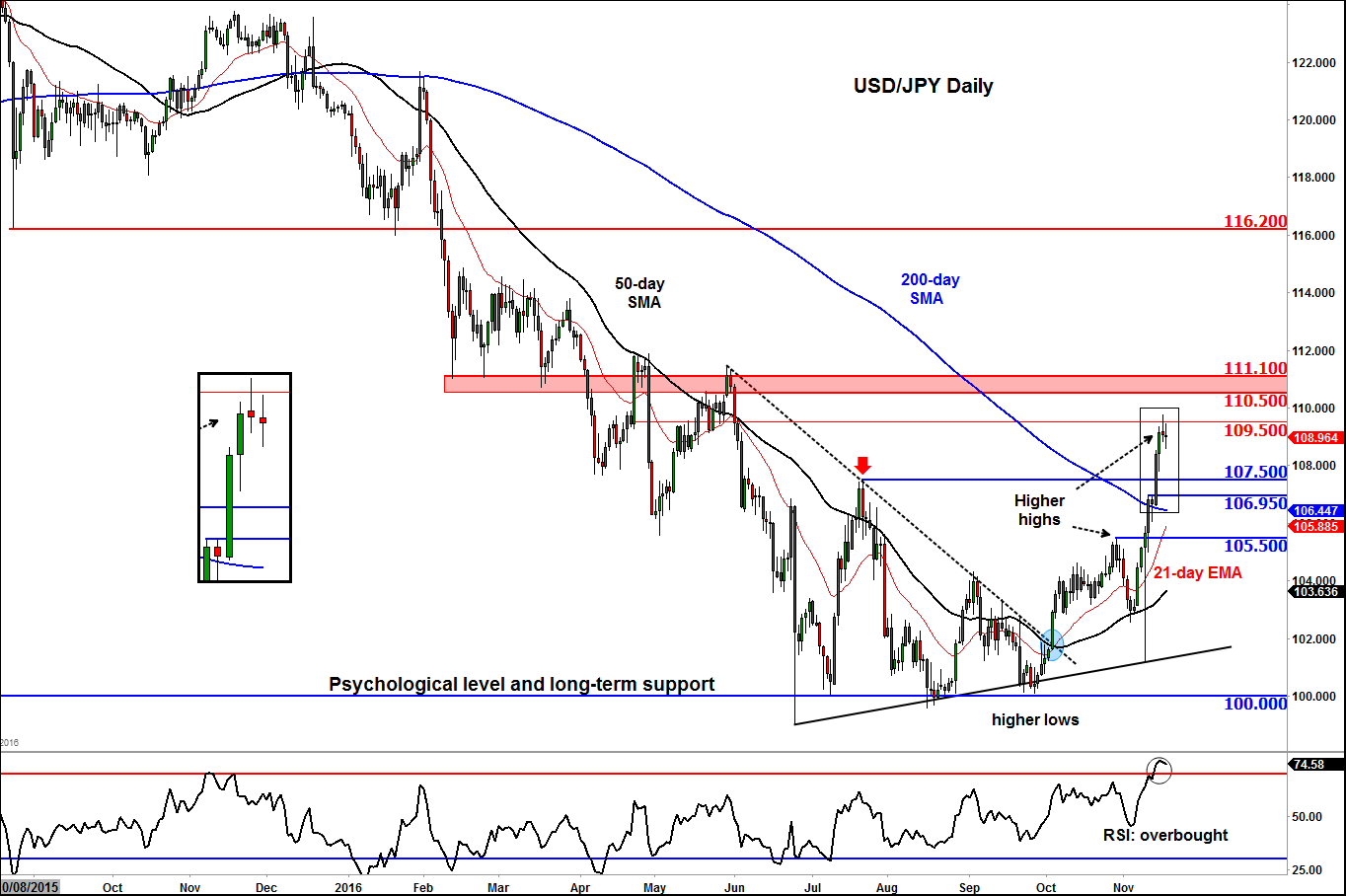

Given this growing disparity between monetary policies of the US and Japan, the USD/JPY remains fundamentally supported. However in the short-term, the prospects of profit-taking could limit the upside for this popular pair, especially when you consider the fact that the Dollar Index has reached its own key 100.00-100.50 resistance range.

Still, our long-term outlook on the USD/JPY remains bullish. We have been banging on about the prospects of a rally in USD/JPY from around 100, even before it dropped to test that key long-term support and psychologically-important level in the summer. Our bullish bias was confirmed when it broke above a bearish trend line at the start of October, when its faster moving 21-day exponential moving average also crossed above the now-rising 50-day simple moving average. The gap between these moving averages have since been expanding, which is bullish. In another bullish development, the 200-day SMA was also taken out as price made its second distinct higher high, having already created several higher lows. So you get the picture: the trend is technically bullish. This means, expect the dips to be bought as the path of least resistance is to the upside.