USD JPY breaks out as bond yields surge higher

The US dollar has turned higher after a weaker start and following two down days, as measured by the Dollar Index. The dollar rebound has […]

The US dollar has turned higher after a weaker start and following two down days, as measured by the Dollar Index. The dollar rebound has […]

The US dollar has turned higher after a weaker start and following two down days, as measured by the Dollar Index. The dollar rebound has been supported by a strong rise in US Treasury yields, with the benchmark 10-year yield rising to around 1.85 percent. We think that it is the rising expectations about tighter monetary policy conditions in the US which is behind the government bond sell-off. Supporting this view was today’s stronger US data in the form of pending home sales, which grew 1.5% month-over-month in September, and jobless claims, which fell to 285,000 applications last week from 261,000 the previous week.

With both the US Federal Reserve and Bank of Japan scheduled to announce their monetary policy decisions next week, the USD/JPY – which has been rather quiet in recent days – will be in focus. But I am expecting to see a big expansion in the USD/JPY’s range next week as the two central banks announce their policy decisions and as we have some very important economic data coming up from the US, namely the October jobs report, which could influence the Fed’s decision at its next meeting in December, when it is widely expected to raise rates again.

Ahead of next week’s busy economic schedule, there are some important economic numbers that could impact the USD/JPY as we approach the end of this week: the Japanese data dump tonight and the US third quarter GDP tomorrow. From Japan we will have, among other things, various measures of inflation, including Tokyo CPI, as well as household spending and the unemployment rate. Meanwhile, the US economy is expected to have advanced 2.5% in the third quarter on an annualized basis, versus 1.4% in Q2. Clearly, these economic pointers have the potential to cause noticeable moves in the USD/JPY.

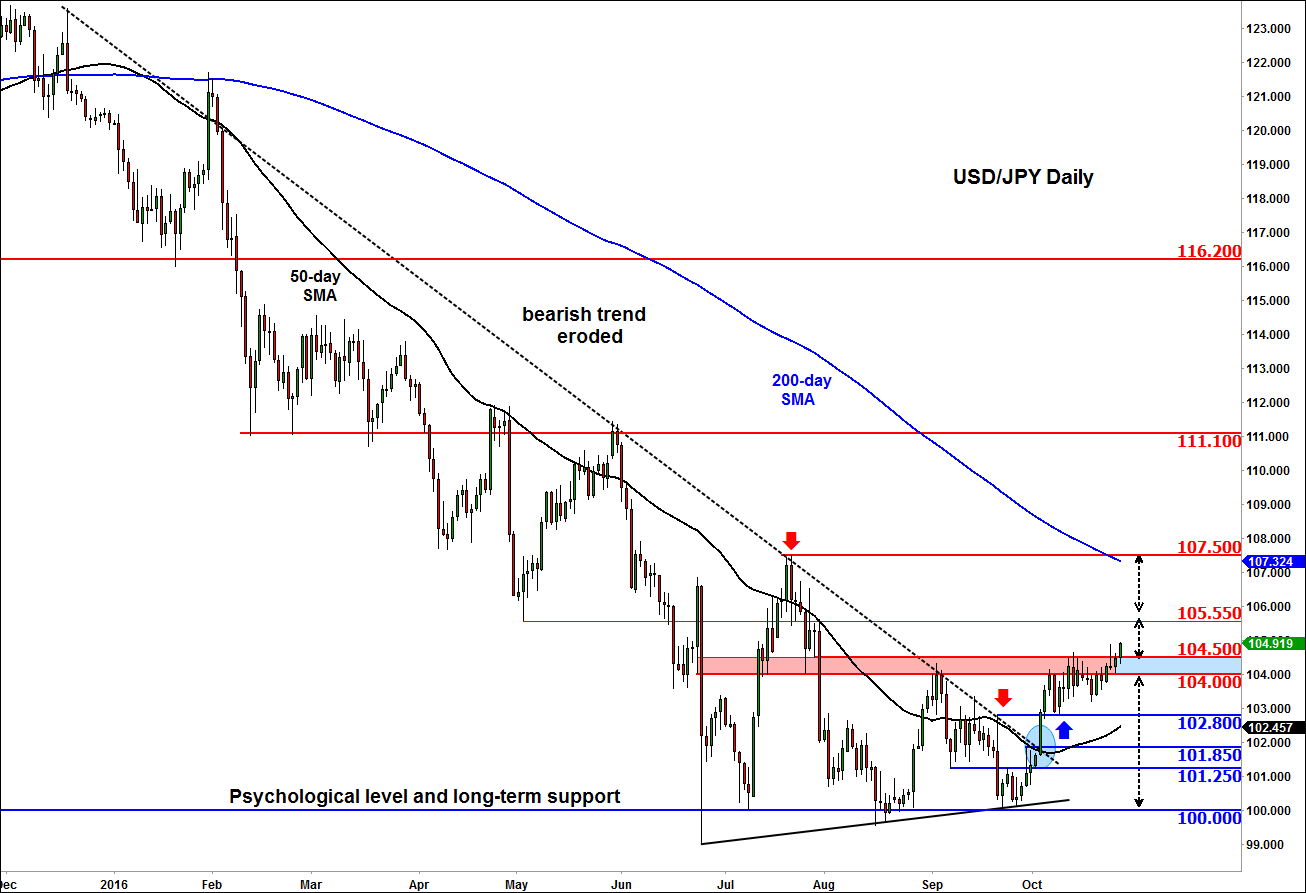

Technically, the trend is still looking strong for the USD/JPY following its breakout above the bearish trend line and the subsequent rally and consolidation near the next resistance area between 104.00 and 104.50. With the 50-day moving average also pointing higher now, we favour further bullish than bearish price action, possibly towards the next swing high at 107.50, which comes in just above the 200-day moving average at 107.30/5 area. A more near-term bullish objective is at 105.55, previously support and resistance. Meanwhile if the USD/JPY moves back below the 104.00 support level then all bets are off. In this potential scenario, the sellers may then aim for the next support at 102.80 next, followed by the levels shown on the chart in blue. For now though, the path of least resistance is to the upside.