USD JPY Ahead of Non Farm Payrolls

Going into tomorrow’s release of the US January jobs report, the bitter taste of the unexpected 0.1% contraction in Q4 GDP may continue to linger. […]

Going into tomorrow’s release of the US January jobs report, the bitter taste of the unexpected 0.1% contraction in Q4 GDP may continue to linger. […]

Going into tomorrow’s release of the US January jobs report, the bitter taste of the unexpected 0.1% contraction in Q4 GDP may continue to linger. But things could change to the benefit of USD/JPY in the case of an upside surprise in NFP, downside in unemployment rate and stronger than expected release in the manufacturing ISM due 90 minutes after the jobs report.

US January’s NFP is expected at 165K, adding on to December’s upside surprise of 155k, which defied low forecasts stemming from Hurricane Sandy. Such a forecast may be sufficient for USD/JPY to maintain its three-month run, especially if the unemployment rate does not rise above 7.9%. Bearing in mind that the unemployment rate drifts at four-year lows and jobless claims are near five-year lows, the downtrend is clearly intact.

In fact, there is emerging chatter that the jobless rate will come in at 7.7%, which would be the lowest since November 2008. If such a figure does materialise, then USD/JPY will most likely leap higher along with stocks- for as long as non-farm payrolls do not come in below 110K-120K.

Another potentially positive report is the January release of the ISM manufacturing report (10 am ET, 3 pm GMT), expected to edge up to 50.6 from 50.2. One reason to expect an upside surprise in the ISM is today’s unexpectedly large five-point jump in the January Chicago PMI to 55.6, the best in nine months. Considering the relatively high correlation between Chicago PMI and manufacturing ISM (correlation at 0.54 from 0.65 three months ago), there is a decent chance of a print above 51.5.

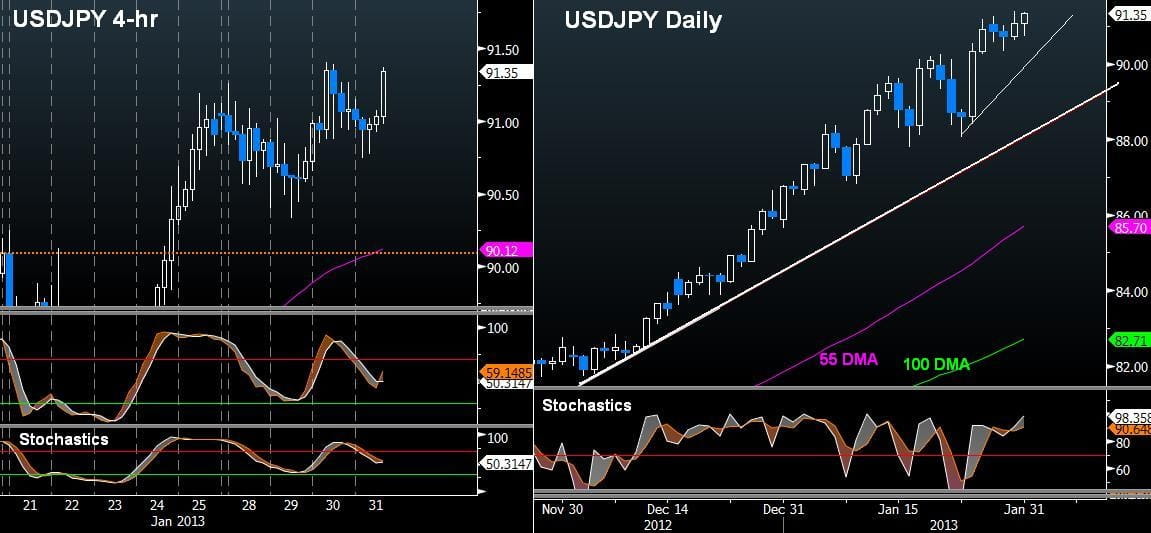

USD/JPY should maintain its 17-week rally even if we do not see a double positive surprise in the unemployment rate and the ISM as long as 88.70 is maintained. Higher support stands at 89.50. USD/JPY posted four consecutive monthly gains—matching the pattern of summer 2008. 92.90 in USD/JPY is seen as a near term resistance. FX traders should keep an eye on US-10 year yields, whose support stands at 1.90 in the event of disappointing figures before gains extend towards 2.09%.

All of the aforementioned factors are US-driven. We have not touched upon the Japanese side of USD/JPY, which continues to prove all the more powerful regarding a change in the inflation target of the Bank of Japan.