USD CAD maintains resilience near new 11 year high

Having reached up to a new 11-year high on Tuesday after rallying for more than a week, USD/CAD pulled back modestly on Wednesday morning due […]

Having reached up to a new 11-year high on Tuesday after rallying for more than a week, USD/CAD pulled back modestly on Wednesday morning due […]

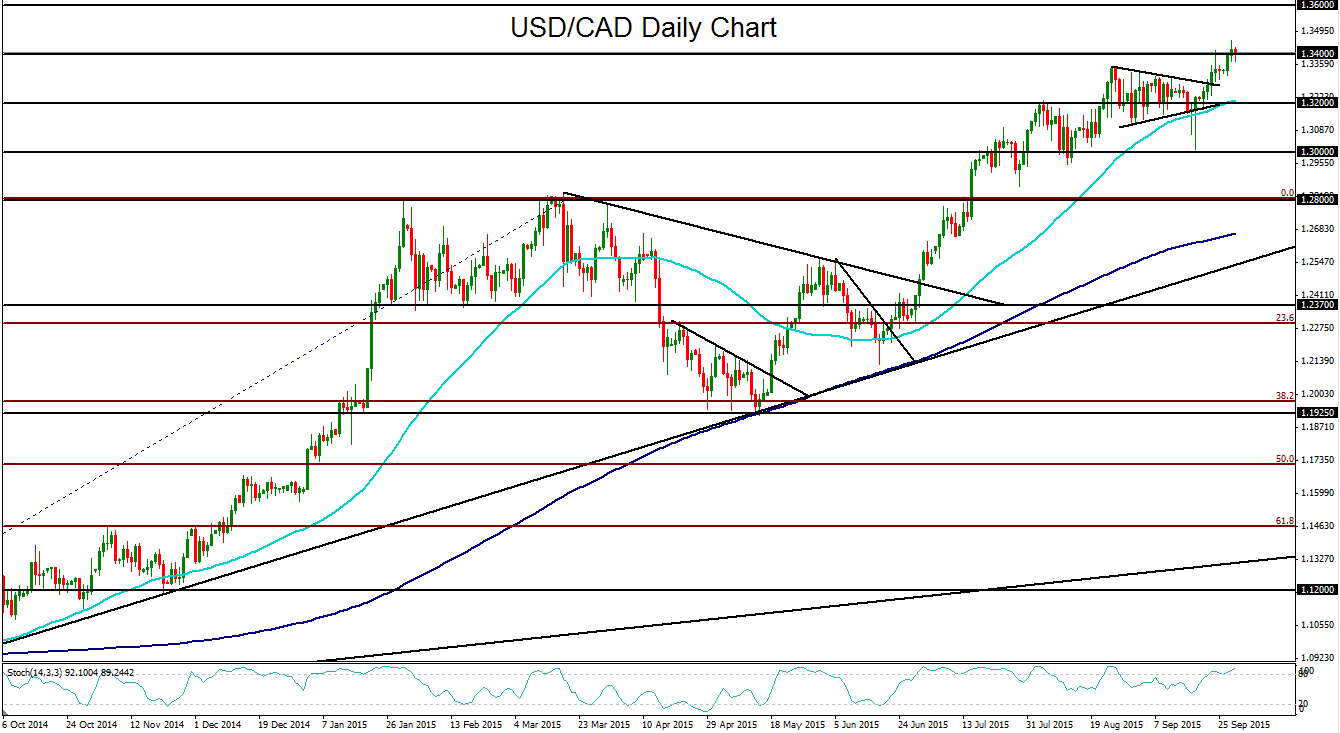

Having reached up to a new 11-year high on Tuesday after rallying for more than a week, USD/CAD pulled back modestly on Wednesday morning due in part to a slightly better-than-expected GDP reading out of Canada that gave a brief lift to the Canadian dollar.

A surge in US dollar strength on Wednesday, however, served to support USD/CAD and kept the currency pair trading around the key 1.3400 level, just below Tuesday’s noted multi-year high at 1.3456.

Last week saw a breakout of the currency pair above a prolonged triangle consolidation pattern. That breakout extended a sharp bullish trend that has been in place since the May lows just above 1.1900. From a longer-term perspective, however, USD/CAD has been entrenched in a strong uptrend since the late-2012 lows below parity.

A persistently strong US dollar and weak crude oil prices, along with a consistently dovish Bank of Canada, have been the primary driving forces behind the rather spectacular rise of the USD/CAD currency pair.

With the US dollar benefiting from market expectations of an initial Fed rate hike sometime this year, and crude oil continuing to pressure the Canadian dollar as it suffers from persistent over-supply and under-demand concerns, the overall prospects for USD/CAD remain significantly bullish.

However, having over-extended up to an 11-year high and facing key resistance around the 1.3400 level, bullish momentum could be slowed on a short-term basis with a pullback. Key support on such a pullback currently resides around the 1.3200 level.

With any continuation of the current bullish run and sustained trading above 1.3400, the primary upside target remains around the 1.3600 resistance level.