12 months ago, investors couldn’t sell out of the banks fast enough. Heading into this earning season banks could well be one of the out performers.

The US S&P 500 banking sector has outperformed the broader market threefold, up some 25% whilst the S&P 500 trades 8% higher.

Here’s what to watch for:

1. Strong earnings

Banking stocks have been supported by improving economic conditions as the vaccine programme accelerates and the US economy re-opens. The improved economic conditions are expected to be reflected in strong earnings.

2. Releasing Reserves

As the outlook continues to brighten more banks are expected to release reserves this quarter. Last year pretty much all banks set aside massive reserves, bracing for heavy losses brought on by the pandemic. However, thanks to huge fiscal stimulus packages from the US government, which banks weren’t factoring in, many of the expected losses never materialized. A number of banks are expected to release these reserves, boosting earnings.

3. NII & NIM

NII & NIM were particularly depressed across 2020 as the Fed cut rates to 0. However, the yield curve has been steepening and the economy strengthening. An economic recovery could mean greater loan volumes and whilst higher long dated yields bring the potential to earn more from those loans in interest relative to what they pay on interest for short term deposits.

4. Strong mortgage activity weak commercial loan activity

Thanks to the Fed dropping rates to near 0 mortgage and refinancing activity picked up firmly across 2020. However, with the 10 year yield now sharply higher, that could start to slow, although any slowdown in refinancing is not expected to show up in Q1.

Meanwhile, businesses struggled on keeping afloat. Given the widespread uncertainty businesses didn’t invest in operations or expanding. With the US economy set to grow 6.5% - 7% this year business lending activity is expected to pick up significantly, although mainly in H2.

5. Improved outlook

The economic outlook is now clearer than it was across the previous year and is more upbeat. A more optimistic earnings call is expected. Restrictions on capital distributions are expected to end after Q2 will which pave the way for share buybacks and dividends.

What to expect from the big banks in Q1 earnings?

JP Morgan – April 14

Last quarter JP Morgan had a blowout performance in both earning and revenues. The bank reported EPS of $3.79 against $2.72 expected on revenue of $30.1 billion against $28.7 billion. Trading revenue jumped 20% and investment bank revenue surged 37%. Meanwhile, net interest income dropped 7%. However, given the recent climb in yields this is unlikely to be repeated this quarter. JP Morgan release $2.9 billion in reserves last quarter. Given the monster Q4 earnings, Q1 is expected to come in lower, but still up on Q1 of 2019.

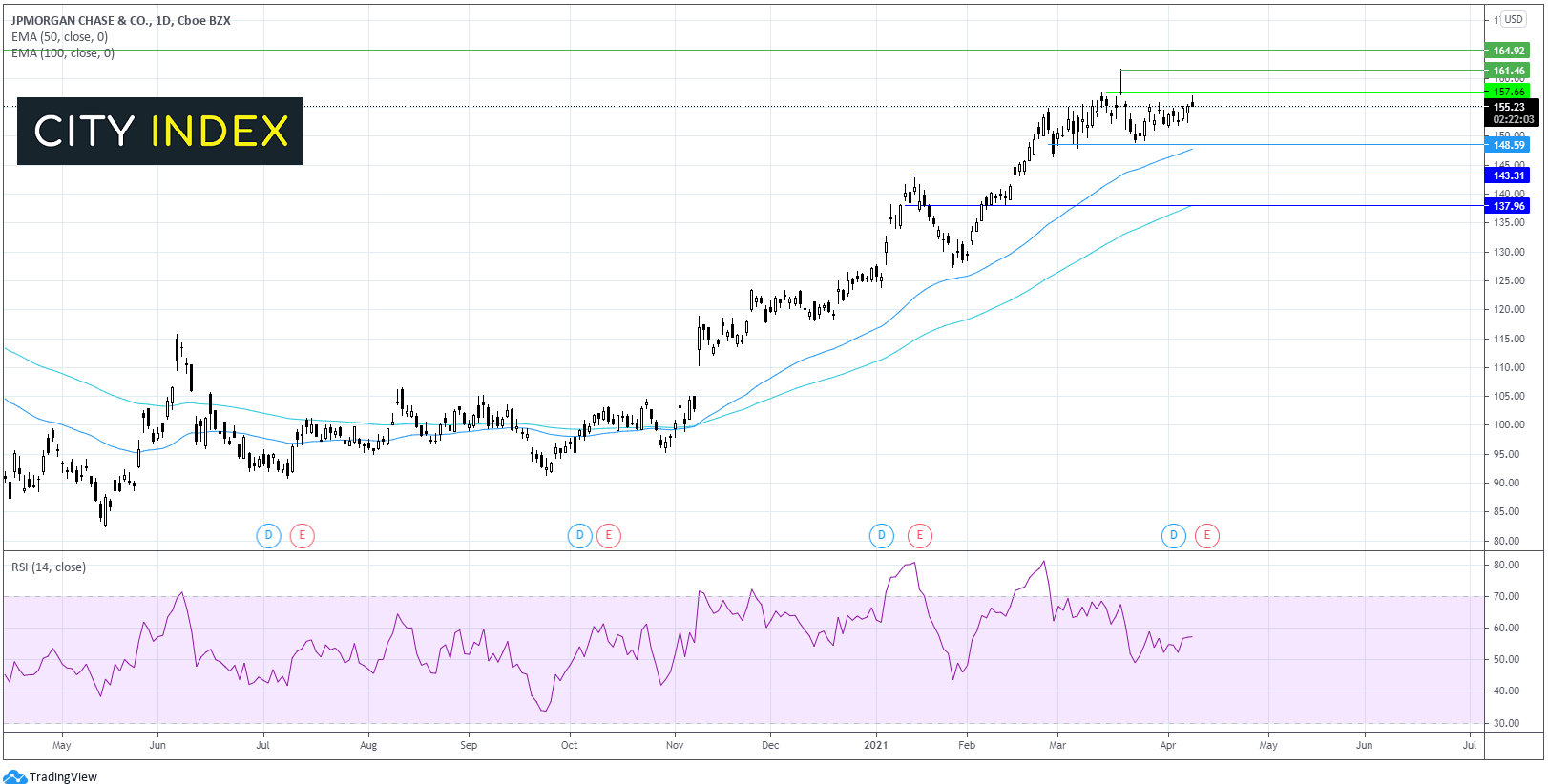

Where next for JP Morgan shares?

After a strong run up over the past 4 months, the bullish momentum has run out of steam. The share price has been range bound over the past three weeks capped by $157.50 on the upper band and 148.50 on the lower band. The RSI also shows a neutral bias as the share price awaits its next catalyst- earnings. A post earnings break out trade set up would see bulls looking for a break above 157.00 to look back towards the all time high of 161.70 and on to 165.00. Seller might look for a break below 148.50 lower band and 50 EMA towards 143.30 high Jan 13.

Goldman Sachs – April 14

Back in January GS reported EPS$12.08 on revenues of $11.74 billion. The equities division was the star performer with revenues surging 40% YoY. The investment banking division also performed well with 27% growth. Attention is likely to remain on the equities division this quarter amid the fallout out from the collapse of Archegos Capital, and what the hit to GS amounts to. Expectations are for EPS $8.28.

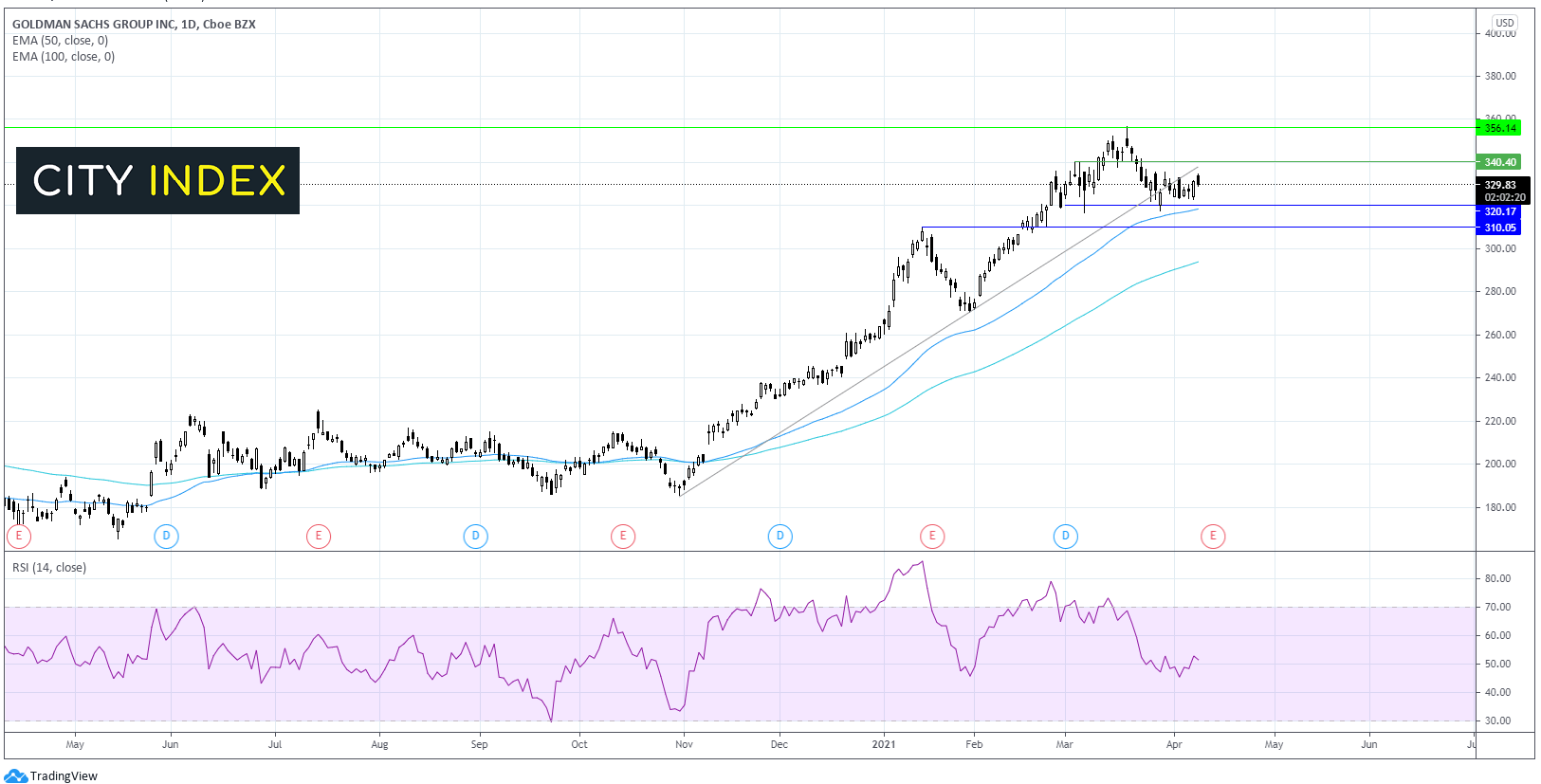

Where next for Goldman Sachs share price?

GS like its peers has been trending higher since November. After hitting an all time high of 356 March 18, the share price has slipped lower. GS share price slipped below the ascending trendline and has been range bound in ahead of earnings. Bulls should look for a meaning close above 340 the ascending trendline support turned resistance and the upper band of the holding pattern. A move above here could see the all time high of 356 retested. On the flip side, a move below 320 the lower band of the channel and the 50 sma could point to a deeper selloff towards 310.

Wells Fargo & Co - 14th April

Watch here what to expect from Wells Fargo & Co when they report.

Citigroup – 15th April

These will be the first earnings released under new CEO Jane Fraser who took over in February. So far the reports have been favourable so this could be her moment to cement a good name. In the previous quarter Citigroup reported EPS $2.07 beating forecasts of $1.35. This quarter Citigroup are expected to post earnings significantly ahead of Q4.

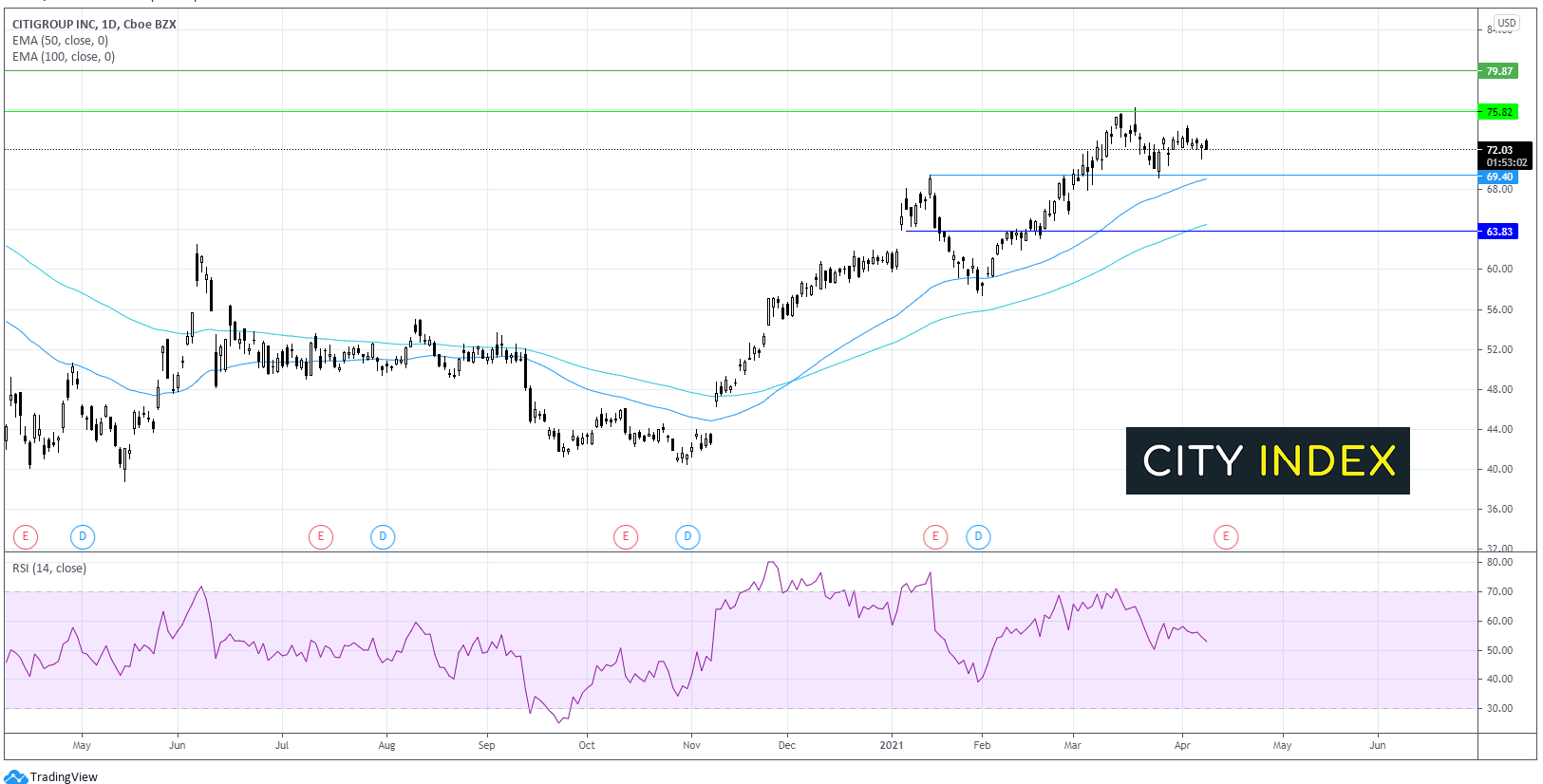

Where next for Citigroup share price?

After rallying for much of the end of last year and picking up that rally again in February, Citigroup is now trading with a neutral bias, in a holding pattern ahead of earnings. The RSI is neutral. A strong report and upbeat outlook could see a break towards 75 to 79 a level last seen pre-pandemic. Any weakness and a downbeat outlook could see the share price fall below lower band support at 69.50.

Bank of America – April 15

BAC is well positioned to outperform. BAC is heavily tilted towards retail banking meaning to stands to perform particularly well in a strong economic growth and steepening yield environment. Costs have been carefully controlled. Given its focus BAC stands to benefit the most from rising interest rates.

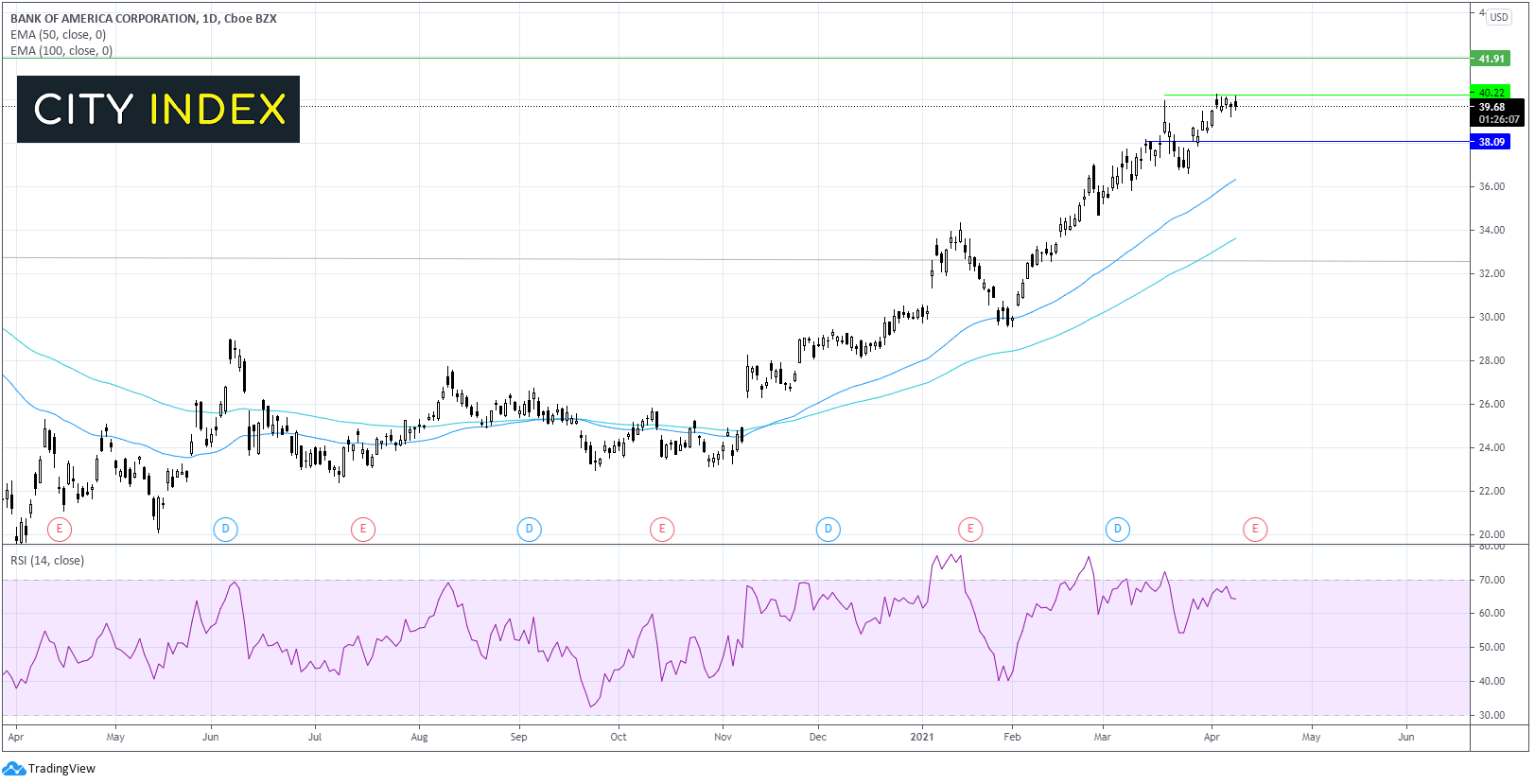

Where next for BAC share price?

The Bank of America share price has rallied hard since early November, hitting an all time high at the beginning of the month. The price continue to hover around that all time high heading towards earnings. BAC trades above its 50 & 100 EMA and the RSI is supportive of further gains.

Strong earnings would propel the price towards 41.00 and on to 42.00. Meanwhile any weakness could see the price slip towards 38.00. Only a move below 36 would negate the bullish trend.

Latest market news

Today 08:18 AM

Yesterday 10:40 PM

Latest Bank Stocks articles

October 10, 2023 09:31 AM

October 6, 2023 02:28 PM

July 17, 2023 04:03 PM

July 11, 2023 02:28 PM