US futures

Dow futures -0.06% at 35442

S&P futures +0.01% at 4520

Nasdaq futures +0.07% at 15422

In Europe

FTSE -0.15% at 7213

Dax -0.17% at 15500

Euro Stoxx +0.03% at 4169

Learn more about trading indices

Supply chains issues reflected in results

US stocks are expected to hold steady on the open as investors digest earnings and the impact of supply chain disruptions on corporate America. The latest releases have helped to distract from stagflation fears but have diverted attention towards supply chain bottlenecks which look set to plague Q3 earnings. Whilst the banks impressed, this is one of the sectors least affected by supply chain bottlenecks. This week have seen more evidence of supply chain issues feeding through into results. For example, Proctor & Gamble yesterday and Accrol today.

Netflix is set to open lower despite beating subscriber numbers and on earnings. Thanks to the draw of “Squid Games” subscribers topped 4.4 million and EPS came in at $3.19 ahead of $2.56 forecast. However, EPS for the current quarter was $0.80 below forecasts and 32% lower YoY. The stock trades lower pre-market.

Looking ahead

Tesla is due to report after the close and show supply chain resilience. The EV makers is poised for a record quarter with deliveries already announced at 241,300.

The economic calendar is quiet. However, Fed speakers will be under the spotlight for further clues and insight as to when the Fed could move to tighten policy.

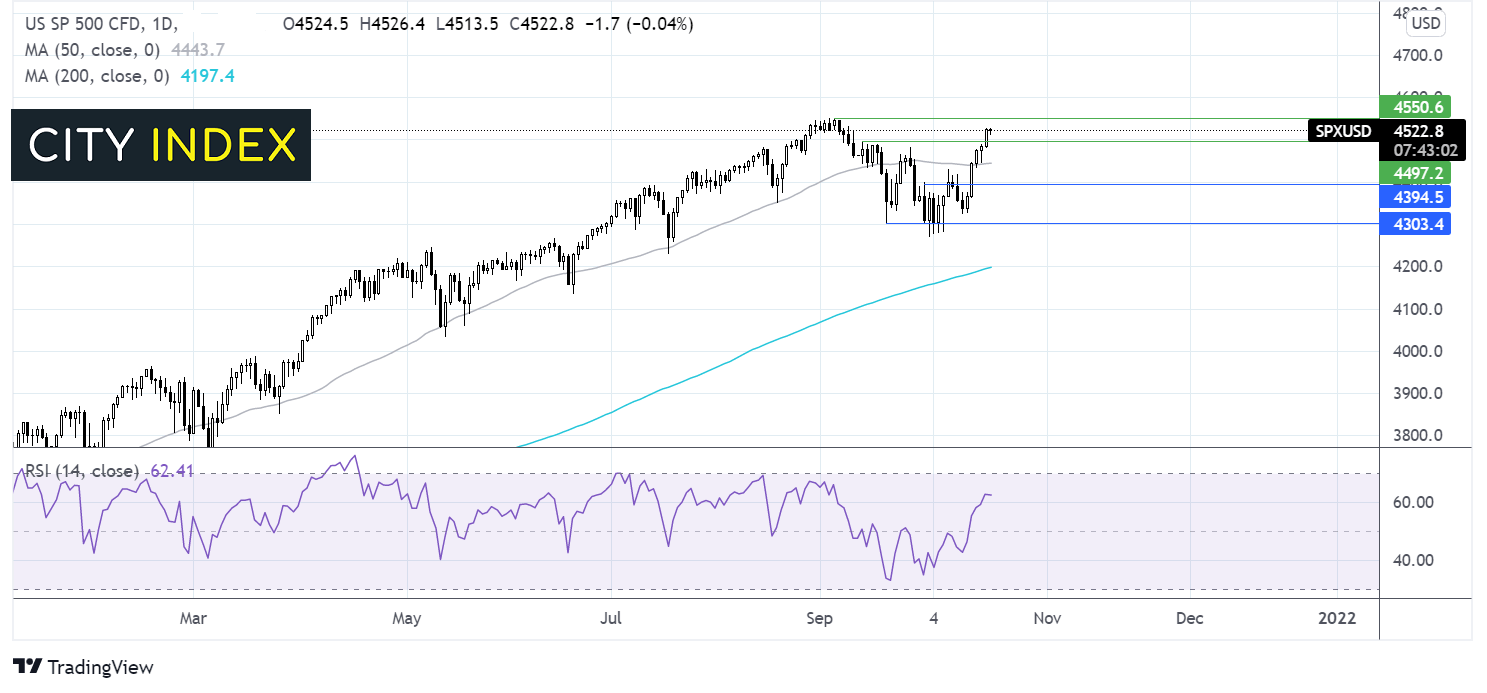

Where next for the Dow Jones?

The bullish RIS combined with the break above 4500 resistance is keeping the bulls optimistic of a move towards 4550 and fresh all time highs. Sellers could look for a move below the 50 sma at 4445 to negate the near term uptrend towards 4400.

FX – USD steady, GBP pares losses after CPI miss

The US Dollar is steadying after losses across the week. The greenback has been out of favour amid expectations that the Fed could be outpaced by other central banks with hiking interest rates.

GBP/USD has pared earlier losses after UK CPI came in slightly weaker than forecast at 3.1% in September, down from 3.3%. This is unlikely to deter the BoE from their more hawkish path given that inflation is set to rise further.

GBP/USD -0.13% at 1.3777

EUR/USD +0.4% at 1.1640

Oil eases as China considers taming coal market

Oil prices are coming under mild pressure after a higher than expected rise in crude stocks and as the Chinese government looks to tame the coal market.

The Chinese government is reportedly considering stepping up efforts to control coal prices which has spiraled higher, showing few signs of slowing. The China National Development and Reform Commission said it would bring coal prices back within a reasonable range. Any such move by Chinese authorities would likely to reverse the fuel switch to oil which has bolstered oil demand in recent weeks.

Data from API revealed that crude stock piles rose by 3.3 million barrels

EIA inventory data is due later today.

WTI crude trades -1.04% at $81.50

Brent trades -0.94% at $83.80

Learn more about trading oil here.

Looking ahead

15:30 EIA Crude oil inventories

16:00 Fed Evans Speaks

18:00 Fed Quarles Speaks

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Indices articles

Yesterday 03:30 PM

April 18, 2024 04:46 PM