US futures

Dow futures +0.5% at 34288

S&P futures +0.36% at 4456

Nasdaq futures +0.25% at 15128

In Europe

FTSE +0.3% at 7109

Dax +0.32% at 15837

Euro Stoxx +0.58% at 4170

Learn more about trading indices

Sentiment improves at the start of a key week

US stocks are set to start the week on the front foot with oil stocks leading the charge after last week’s losses. Bargain hunters are on the prowl after last week’s steep selloff.

Bonds declined as safe haven demand eased, pulling the US Dollar lower. The knock-on effect of a weaker US Dollar and improved risk sentiment has been a rebound in commodity prices. Oil is trading over 3% higher lifting energy stocks which were serial underperformers last week.

Whilst delta concerns remain very much in focus, China reported zero locally transmitted cases, boosting sentiment. Cases are still on the rise with the US seeing the 7 day average covid deaths pass 1000 for the first time since March. Rising cases come as the Fed, according to the latest FOMC minutes, are increasingly comfortable with easing support this year.

Bets appear to be easing that Jerome Powell will use the economic forum as a platform to lay the groundwork for reining in bond purchases, particularly now the Jackson Hole Symposium is going virtual due to rising covid cases.

Looking ahead PMI data and existing homes figures will be in focus.

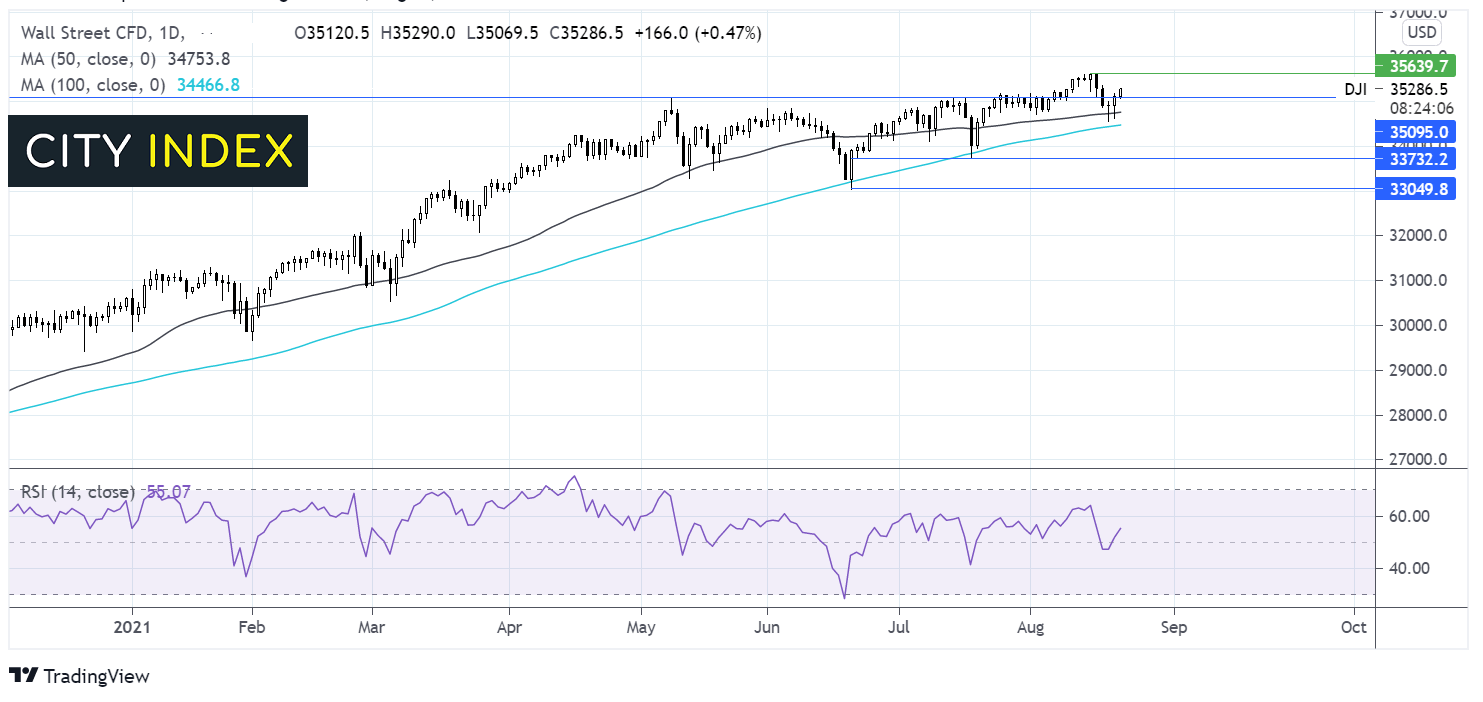

Where next for the Dow Jones?

The Dow Jones is pushing higher again after bouncing off the 50 sma support. The price has pushed over the key 35000 negating the recent downtrend and opening the door to 35600 and fresh all-time highs. The RSI is supportive of further upside, pointing higher and in bullish territory. On the downside, support can be seen at 34750 the 50 sma ahead of 34450 the 100 sma. A break below here could see the sellers gain traction.

FX – USD eases, GBP rebounds even as services pmi misses forecasts

The US Dollar is trending lower after strong gains in the previous week as investors reposition ahead of the Jackson Hole Symposium which kicks off on Thursday. Weakness in the USD as the economic forum moves to an online event suggests that investors are easing bets that the Fed will lay the groundwork for tightening policy in light of rising covid cases.

GBP/USD- the Pound is charging higher despite weaker than forecast services PMI data. The service sector expanded at 55.5 down from 59.6 in July and missing forecasts of 59. The service sector was disrupted by rising covid cases and “pingdom” as large numbers of people were ordered to self-isolate. The UK manufacturing sector, however, performed better than expected.

GBP/USD +0.42% at 1.3676

EUR/USD +0.26% at 1.1727

Oil moves bounces higher

Oil prices are rebounding after a steep selloff of over 5% in the previous week. A softer US Dollar following a less hawkish than usual Fed Kaplan, combined with an improved covid picture in China the world’s largest oil importer has boosted demand for oil. China recorded zero locally transmitted covid cases for the first time since July raising the demand outlook.

Even so, caution is the name of the game given that covid cases are rising globally.

US crude trades +3.3% at $64.09

Brent trades +3.2% at $67.01

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

14:45 Markit Manufacturing & Services PMI

15:00 Existing Home Sales

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Crude Oil articles

Yesterday 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM