US futures

Dow futures +0.2% at 34919

S&P futures +0.15% at 4396

Nasdaq futures +0.15% at 14986

In Europe

FTSE +0.16% at 7093

Dax +0.15% at 15553

Euro Stoxx +0.01% at 4115

Learn more about trading indices

Earnings, Tencent & Factory Orders in focus

US stocks are pointing to a stronger start as investors digest corporate earnings, slowing economic growth and rising covid cases.

Q2 earnings season has been encouraging. According to Refintiv over 88% of corporate reports beat forecasts, this is the highest level since records began in 1994. More earnings are due with Eli Lilly, Lyft and Marriott International all due to report today.

Earnings aside, Chinese gaming firm Tencent is likely to be under the spotlight after Chinese regulators criticized the videogaming firms raising concerns that the gaming sector could be next on regulators hit list.

Separately covid cases are on the rise with 72,000 new cases a day, up 44% over the previous week. Furthermore, economic growth is showing signs of slowing. The manufacturing PMI slowed in July. Factory orders are due to be released shortly, these are also expected to show a slowdown to 1% growth in June, down from 1.7% in May.

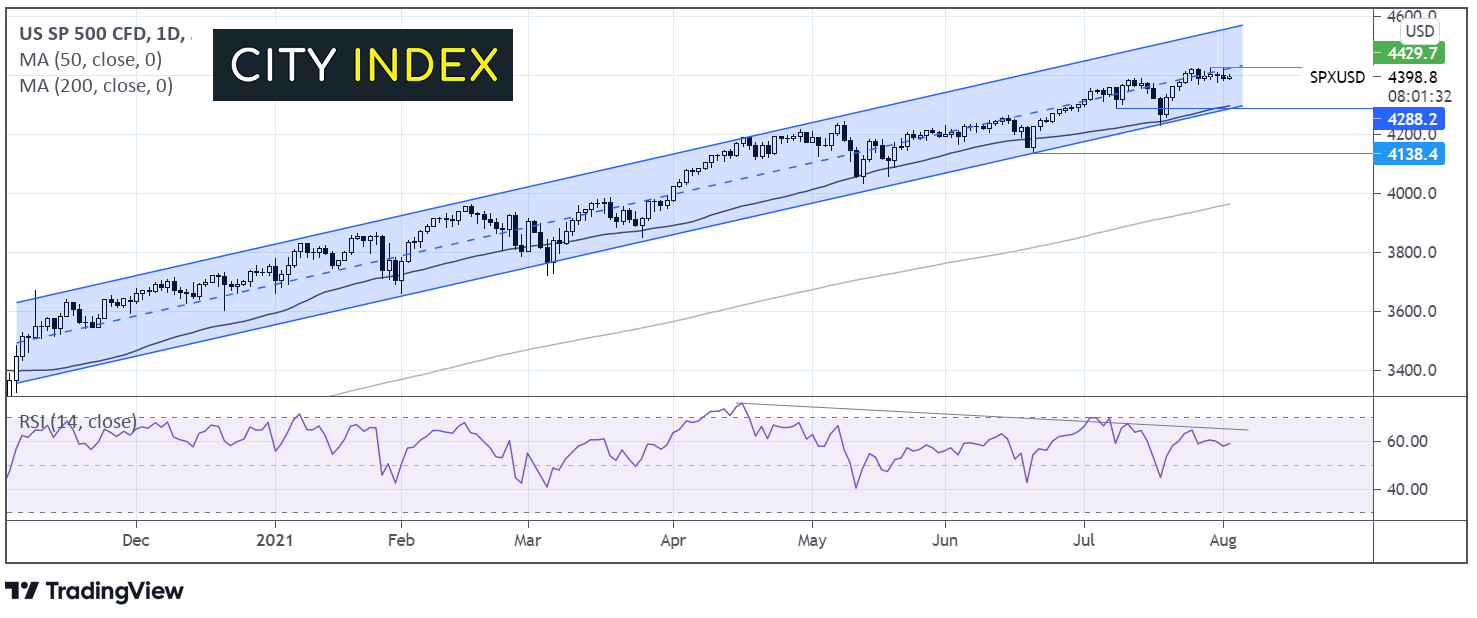

Where next for the S&P?

The S&P continues to trade in a multi-month ascending channel hovering around all time highs. It trades around the midpoint of the ascending channel. However, it is worth noting the RSI bearish divergence which could be a signal that momentum is wearing thin. It would take a move below 4280 the lower band of the ascending trendline to negate the near-term uptrend.

FX – USD subdued, antipodean’s in favour

The US Dollar is subdued on Tuesday. Declining treasury yields suggest that fears of disappointing economic growth are dominating. Manufacturing PMI showed hat activity slowed in July for a second straight month.

Antipodean currencies are in favour boosted by central bank talk. The Aussie Dollar and the New Zealand Dollar are the biggest gainers among G10 currencies. The RBA stuck with its plan to taper the bond buying programme, shrugging off any concerns stemming from the latest covid wave.

AUD/USD +0.3% at 7379

GBP/USD +0.29% at 1.3925

EUR/USD +0.12% at 1.1885

Oil consolidates after worst daily losses in 2 weeks

Oil prices are consolidating after steep losses in the previous session. Oil fell over 3% amid growing concerns over the slowing pace of growth in two key markets – China and the US. Factory activity came in weaker than expected with Chinese manufacturing printing at 50.3, less than the 51 forecast.

Covid cases are also on the rise in China with tougher restrictions being imposed. This is unnerving the oil market given that China is the second largest oil importer.

However, investors are betting on a further fall in inventories with API data due later today. This would mark the third straight week of declines in crude stock piles.

US crude trades +0.15% at $71.09

Brent trades +0.23% at $73.00

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

14:45 US Factory Orders

21:30 API Crude Oil Stockpile

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM