US futures

Dow futures -0.4% at 34472

S&P futures -0.14% at 4360

Nasdaq futures +0.31% at 14863

In Europe

FTSE -0.5% at 7081

Dax +0.07% at 15686

Euro Stoxx -0.03% at 4065

Learn more about trading indices

Mixed start to a busy week

US indices are pointing to a mixed start on the open, after all three main Wall Street indices finished at all time highs on Friday.

Concerns grow over rising covid cases, as new daily infections in the US hit the highest level since May over the weekend, unnerving investors.

Covid concerns will add to nerves that peak growth has passed as recent US economic data has under-performed.

Whilst the Dow and the S&P futures are in the red, the high growth tech stock extends its rally as investors continue to rotate back into growth.

Whilst today is a quiet day for data and earnings there is plenty across the week to keep the markets busy. US CPI and PPI data on Tuesday and Wednesday, in addition to Fed chair Jerome Powell testifying before congress on Wednesday and Thursday, will keep inflation and the Fed’s next steps firmly in focus.

Tomorrow earning season is due to kick off with the Goldman Sachs, JP Morgan and PepsiCo updating he market.

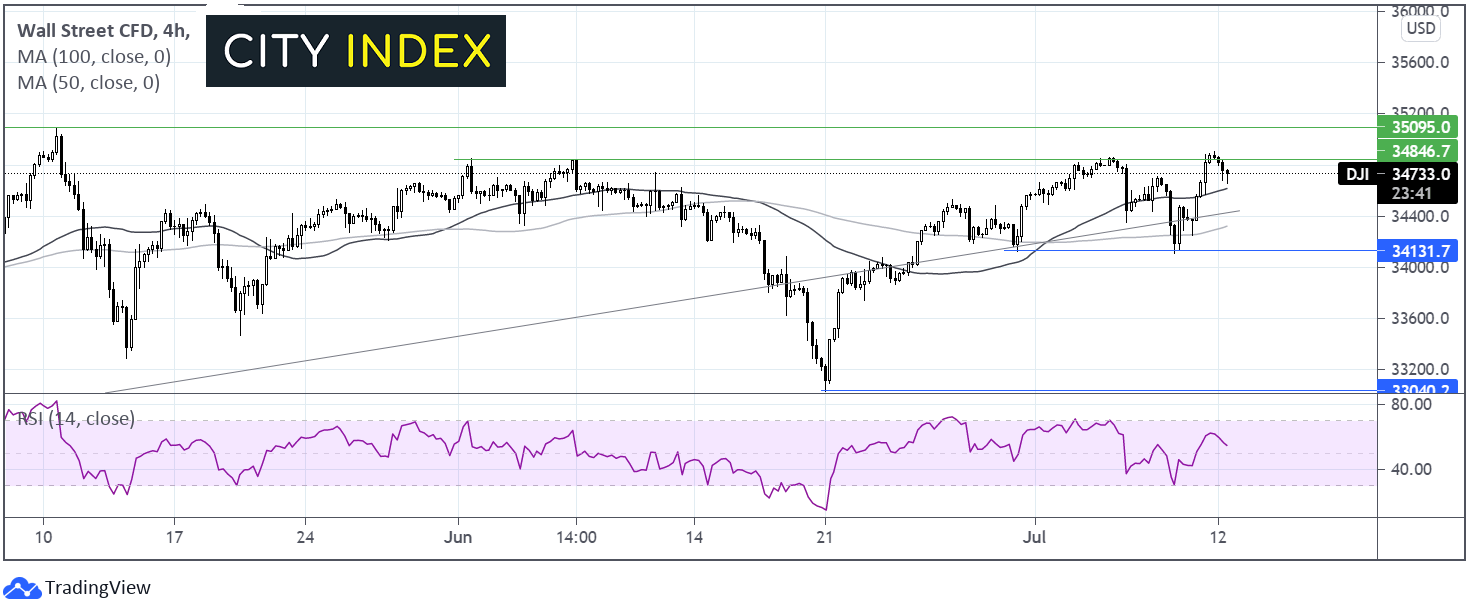

Where next for the Dow Jones?

The Dow Jones hit a high of 34906 but failed to hold that level, slipping back below the level 34850 which had offered resistance on several occasions across the past month. The RSI is in bullish terrirory but points lower, giving mixed messages. Whilst the 50 sma on the 4 hour chart holds at 34600 buyers can be hopeful of another attack on 34850 and on towards 35000. A break through the 50 sma at 34600 could open the door to 34420 the ascending trendline support from ealy October and the 100 sma at 34350. Below here the sellers could gain momentum.

FX – USD rallies, EUR falls on dovish ECB Lagarde

The US Dollar is climbing higher at the start of the week, after steep losses at the end of last week. Safe haven flows into the US Dollar amid rising covid cases are lifting the greenback. Attention is also shifting back to inflation and the Fed’s next steps with CPI data, PPI data and Jerome Powell testifying before Congress coming up this week.

EUR/USD trades lower after ECB President Christine Lagarde Sid That forward guidance will be changed at the July 22 meeting. Lagarde hinted that the bond buying scheme could be extended beyond March 2022 albeit in a new format.

GBP/USD +0.24% at 1.3820

EUR/USD +0.1% at 1.1856

Oil falls on covid worries

Oil prices are slipping lower as concerns over slowing global growth overshadowed the prospect of tightening supply after OPEC+ talks to raise output failed earlier in the month.

The rapid spread of covid cases and unequal access to covid vaccines threaten to slow global economic recovery. According to Reuters, covid infections are rising in 69 countries. Parts of Asia are back under lockdown conditions.

This comes after OPEC+ group abandoned talks at the stat of the month amid infighting and failure to agree unanimously to raise output in order to satisfy the demand outlook

US crude trades -1.4% at $72.98

Brent trades -1.3% at $74.24

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

14:30 Fed Williams due to speak

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 03:30 PM

Yesterday 01:23 PM

Yesterday 11:00 AM

Yesterday 08:15 AM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM