US futures

Dow futures -0.4% at 35670

S&P futures -0.3% at 4676

Nasdaq futures -0.36% at 15817

In Europe

FTSE +0.02% at 7273

Dax -0.93% at 15813

Euro Stoxx -0.5% at 4260

Learn more about trading indices

Stocks lower as data is released, retailers in focus

US stocks are set to open lower on the back of disappointing earnings from a number of big retailer names, after a mixed bag of US data and amid growing COVID concerns in Europe.

On the one hand, Q3 GDP was revised up in the second estimate to 2.1%, from 2% thanks to stronger than initially estimated consumer spending. However, this was still short of forecasts of an increase to 2.2%. This is still down sharply from 6.7% in Q2 amid a resurgence of COVID, supply chain disruptions and labour shortages.

Alongside a slightly disappointing GDP print were weaker than forecast durable goods sales. Durable goods sales unexpectedly contracted in October to -0.5% MoM, down from -0.4% in September and well short of the 0.2% increase forecast.

On the other side of the coin US jobless claims figures were impressive falling to a level not seen since 1969. Jobless claims came in at 199k, well below the 260k forecast. The significant drop in jobless claims is offsetting weak data elsewhere because we know that the Fed is watching the labour market very closely. The Fed wants to see improvements in the labour market recovery in order to raise rates and today’s data is certainly a step in that direction, yields trade 1.2% higher and the USD higher as expectations of a sooner move by the Fed grow, However it is worth noting that this huge drop in jobless could in fact be due to seasonal swings.

Looking ahead there is still plenty more data for investors to sink their teeth into with Michigan confidence and Core PCE data due. Core PCE is expected to show inflation at 4.1% with a high reading expected to prompt bets of a sooner move by the Fed.

The minutes from the latest Fed meeting are also due and whilst these could shed some light on the transitory inflation theme, its important to remember that the meeting happened prior to the 6.2% CPI print.

Stocks in focus

The retail sector will be in focus as black Friday and the holiday shopping season approaches but also because the likes of GAP and Nordstrom report disappointing quarterly earnings. Both trade over 20% lower pre-market.

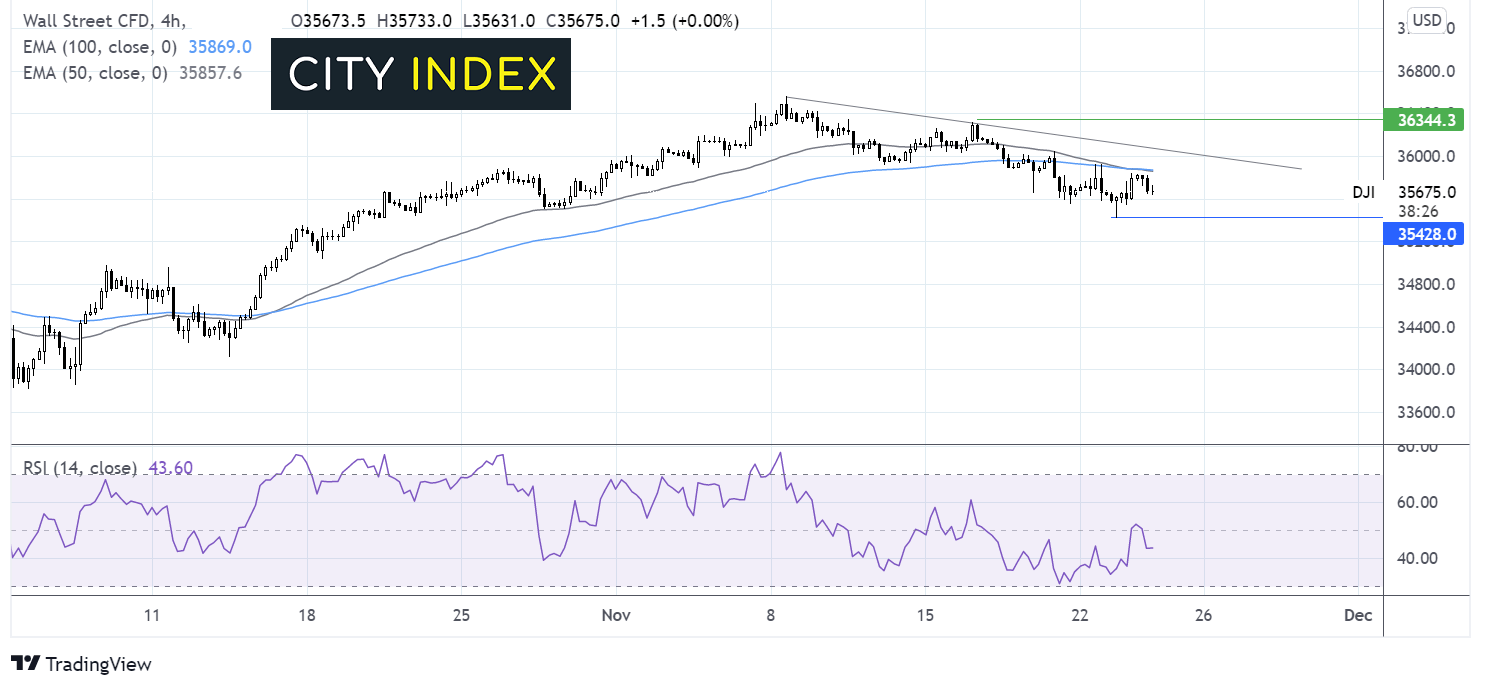

Where next for the Dow Jones?

After reaching its all-time high on November 8, the Dow Jones has been trading lower. It trades below its descending trendline, below the 50 & 100 EMA. The RSI is supportive of further downside. However, sellers will need to break below 35430 for fresh monthly lows. Meanwhile buyers will need to break above 35850 the 50 & 100 EMA to expose the 2-week falling trendline resistance at 36060 beyond here the buyers could gain traction.

FX – USD extends gains, EUR at fresh 2021 lows

The USD is pushing higher trading a fresh 16-month highs as investors continue betting on a sooner move by the Fed and treasury yields advanced. Today sees a slew of US data due to be released in addition to the minutes from the Fed’s November meeting.

EUR/USD is resuming its selloff after German IFO data revealed that business sentiment weakened further in November, its fifth straight month of declines. The headline business sentiment index fell to 96.6, down from 97.7 meaning that confidence was on a weak footing even before the most recent fourth wave of COVID hit, which doesn’t bode well for the outlook.

GBP/USD -0.14% at 1.3360

EUR/USD -0.32% at 1.1211

Oil holds most of yesterday’s gains

Oil prices are holding onto the lion’s share of yesterdays’ gains. Oil prices jumped higher despite a coordinated move by the US and other oil consumers such as China, India, Japan and South Korea to release strategic oil reserves to bring the price of oil lower. However, oil prices ended up gaining – not quite the effect that they were looking for.

It is worth noting that oil prices had been falling in the four weeks leading up to the announcement, so a good deal of the news was already priced in. Furthermore, It appears that the main reason that prices pushed higher is because the actual release is actually to be smaller at 70-80 million barrels, than the initially feared 100 million barrels.

API stockpile data revealed a 2-million-barrel increase, expectations had been for a 500,000 draw.

For now, EIA inventory data will be in focus.

WTI crude trades -0.03% at $78.31

Brent trades -0.24% at $81.15

Learn more about trading oil here.

Looking ahead

15:00 US Core PCE

15:00 New Home Sales

15:30 EIA crude oil inventory data

19:00 FOMC minutes

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Today 07:49 AM

Today 04:24 AM

Yesterday 10:48 PM

Latest Forex articles

Today 04:24 AM

Yesterday 10:48 PM

Yesterday 12:00 PM