US futures

Dow futures -0.34% at 35372

S&P futures -0.36% at 4452

Nasdaq futures -0.35% at 15085

In Europe

FTSE -1.27% at 7133

Dax -0.42% at 15910

Euro Stoxx +0.6% at 4203

Learn more about trading indices

Covid woes and economic growth concerns drag on sentiment

US stocks are set to start the week on the back foot after touching fresh record highs at the end of last week. Rising covid cases coupled with concerns of the health of the economic rebound in China are weighing on risk sentiment.

Indices had been supported by impressive earnings last week with S&P500 seeing 87% of companies reporting earnings surprises to the upside.

However today the mood is more cautious after Chinese retail sales and industrial production rose more slowly than expected in July. With covid cases on the rise the disruption to businesses is becoming more apparent.

The disappointing Chinese data comes hot on the heels of weaker than forecast US consumer confidence data. Last week data revealed that US consumer morale slumped to the lowest level since 2011.

Geopolitics were adding to the downbeat mood after the Taliban took Afghanistan over the weekend.

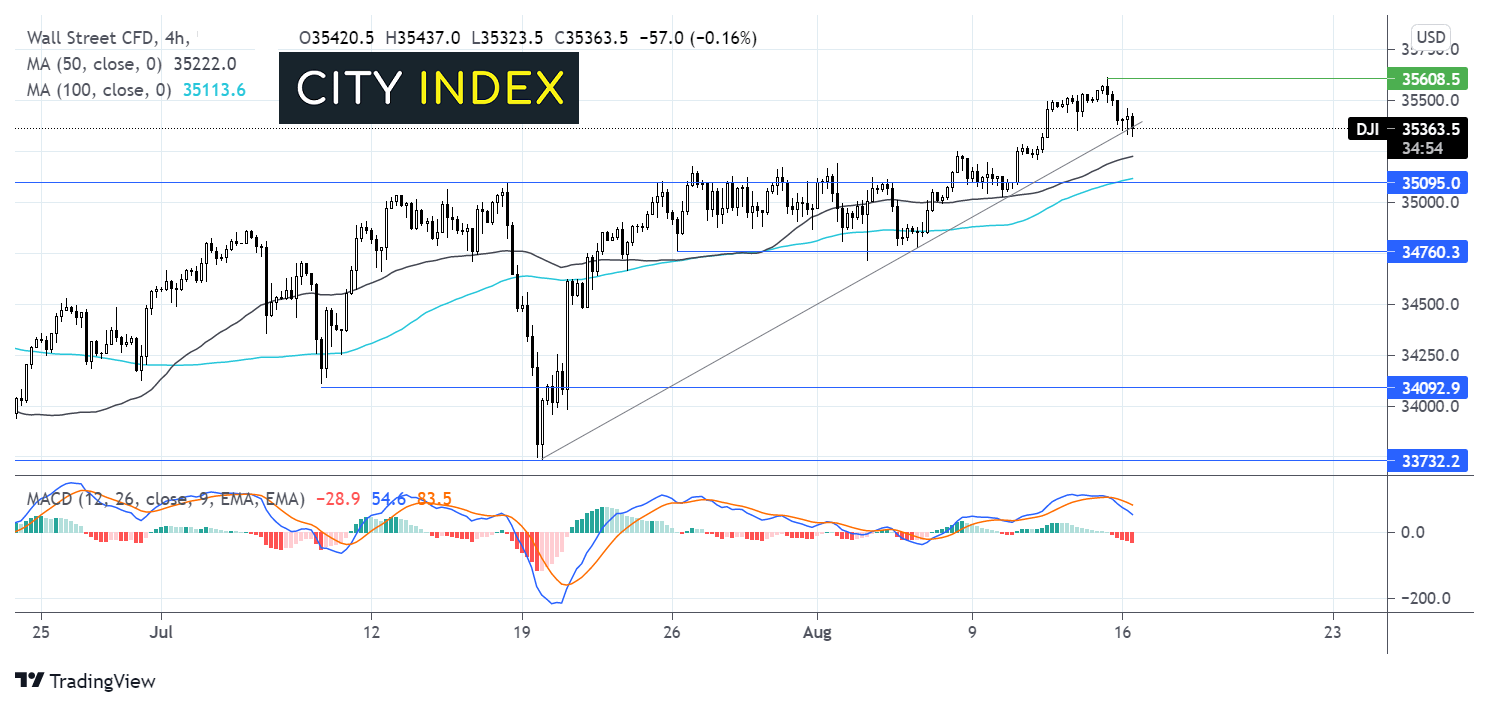

Where next for the Dow Jones?

The Dow Jones reached a fresh record high at the end of last week at 35600. The index is easing lower at the start of the week. The index is testing support of the month old ascending trendline. The bearish cross over on the MACD is supportive of further downside. Any meaningful move lower would need to break below the ascending trendline at 35350 and the 50 sma on the 4 hour chart at 35200. It would take a move below 35100 the 100 sma and previous resistance to negate the near term up trend. A move below 34760 could see more sellers jump in. Bulls meanwhile will keep their eyes on 35600 in order to break towards fresh all time highs.

Source: TradingView, StoneX

FX – USD steadies after steep losses, AUD hit by Chinese data

Broadly speaking the FX markets are quiet today after a volatile end to last week.

USD is edging a few pips higher after steep losses on Friday. The steep drop in consumer confidence eased pressure on the Fed to act to tighten monetary policy. There is no high impacting data due for release today. Attention will shift to tomorrow’s speech by Fed Jerome Powell.

AUD/USD is under performing after the weaker than forecast Chinese data. Disappointing data from China weighed on the China proxy the Aussie.

AUD/USD -0.58%

GBP/USD +0.02% at 1.3866

EUR/USD -0.12% at 1.1775

Oil skids lower on Chinese demand concerns

Oil prices are tumbling lower at the start of the week amid rising concerns over the strength of the Chinese economic recovery. Retail sales and factory output data from China were weaker than expected. Official data also showed that refining throughput slowed amid more signs that the latest COVID outbreak was hurting the world’s second largest economy and second largest importer of oil.

China’s crude processing fell on a daily basis to a level last seen in May 2020.

Doubts over the speed of the economic recovery in the US following the sharp fall in consumer confidence was adding pressure oil prices.

US crude trades -1.3% at $6731

Brent trades -1.17% at $6950

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

02:30 RBA Meeting Minutes

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Commodities articles

April 22, 2024 03:42 AM

April 19, 2024 03:35 AM

April 17, 2024 03:02 AM

April 15, 2024 12:48 AM