US futures

Dow futures -0.01% at 31315

S&P futures +0.3% at 3840

Nasdaq futures +0.5% at 12915

In Europe

FTSE -1.6% at 6540

Dax -0.4% at 13815

Euro Stoxx -0.9% at 3650

Learn more about trading indices

Risk rally halts

Risk assets are broadly out of favour again today after a steep selloff in the previous session. Investors continue to price in a solid economic recovery, rising inflation and earlier intervention from the Fed despite soothing words of support from Fed Chair earlier in the week.

The yield on the 10-year treasury yield surged to 1.6% a pre-pandemic high overnight although has eased back to 1.5% today.

The strong greenback is hitting commodity prices across the board.

Stimulus vote

The House of Representatives will vote on President Biden’s relief package later in the session.

The Democrats plans to implement a national minimum wage of $15 as part of the $1.9 trillion stimulus proposal have been stopped in their tracks. A Senate official ruled that it can’t be passed under the Budget reconciliation provisions.

Stock to open mixed, after steep selloff

US stocks are pointing to a mixed start in cautious trading after sharp declines on Thursday as investors adjusted positions for rising inflation expectations.

The Dow Jones close -1.8% lower, the S&P 500 shed -2.5% and the Nasdaq slumped -3.5% in its biggest one-day selloff since October 28th.

This selloff marked a notable turnaround for stocks which have rallied hard across January and February.

However, with bond yields rising the markets are pricing in earlier intervention from the Fed. The potential of rising borrowing costs is taking the shine off stocks, particularly high growth stocks which have stretched valuations.

Airbnb

Airbnb dived over 9% in the previous session hit by the broad tech stock selloff. However, it trades +1.5% pre-market after forecasting a strong rebound in bookings this year.

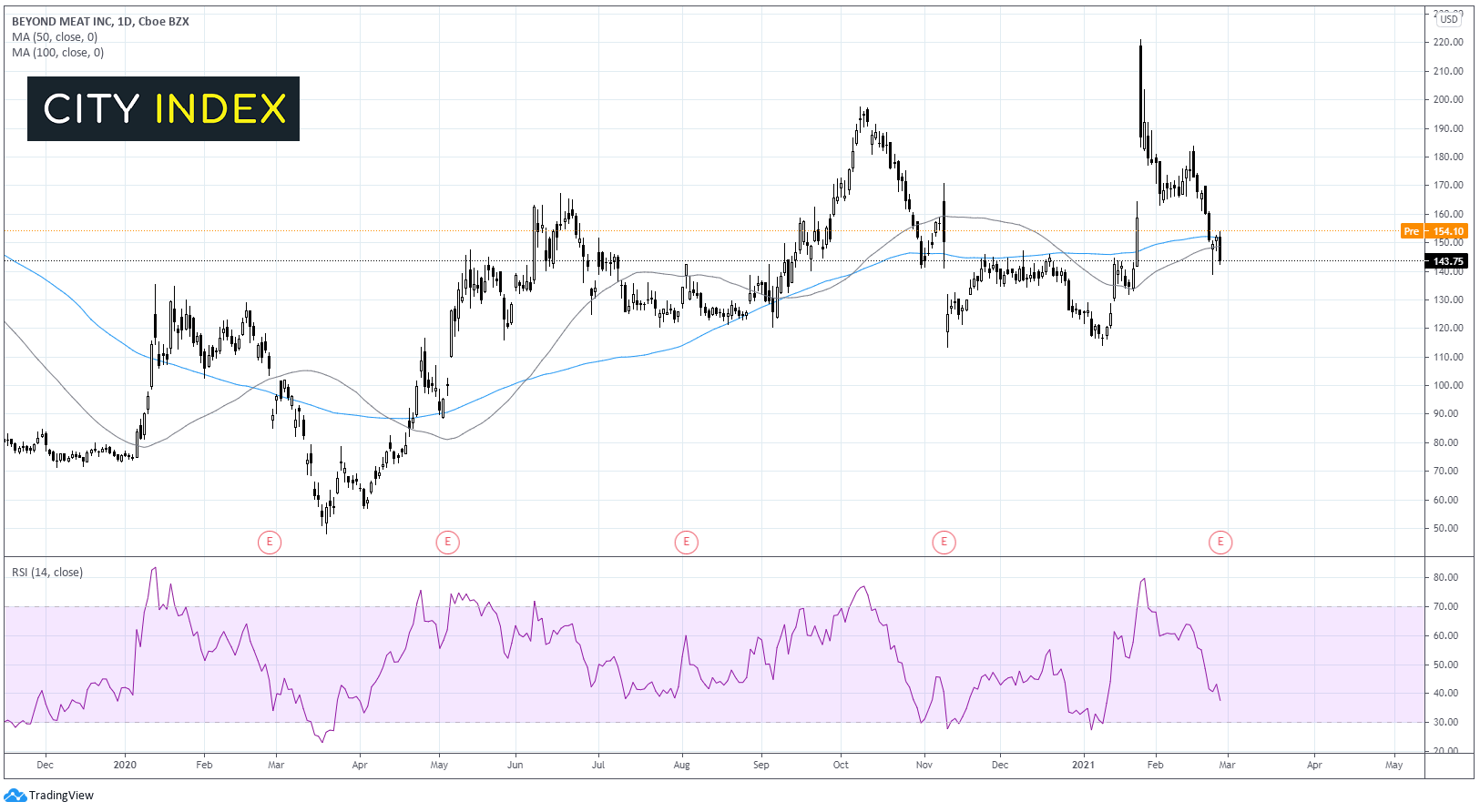

Beyond Meat

Beyond Meat trades +5.9% pre-market after announcing that it has signed an agreement with McDonalds and Yum! The owner of KFC, Pizza Hut and Taco Bell.

FX – US Dollar soars

The US Dollar rebounded off a 7 week low in the previous session and has continued rising as investors reprice the chances of a rate hike from the Fed. DXY looks towards 91.00

GBP/USD has fallen sharply from 1.4230 highs earlier in the week and heads towards $1.39 on US D strength and after BoE Governor Andrew Bailey warned that the UK economy is expected to contract in Q1.

Analyst Fiona Cincotta looks at GBP/USD price action and levels to watch.

GBP/USD trades -0.70% at 1.3914

EUR/USD trades -0.5% at 1.2115

Oil slides but set for 5% gains across the week

As with other commodities, crude oil trades over 1% lower on the back of US Dollar strength and as investors repositioned ahead of next week’s OPEC meeting. The meeting will see the output levels for April set. Speculation is growing that Russia will push for a rise in output levels.

Despite today’s selloff, WTI is still on track for 5% gains across the week.

Baker Hughes rig count data due later.

US crude trades +2% at $62.25

Brent trades +0.4% at $64.81

Learn more about trading oil here.

The complete guide to trading oil markets

Latest market news

Today 04:00 PM

Today 01:15 PM

Today 11:30 AM

Today 08:18 AM

Latest Equities articles

April 12, 2024 02:28 AM

April 7, 2024 08:46 PM

March 31, 2024 11:22 AM