US futures

Dow futures -0.1% at 34320

S&P futures -0.04% at 4346

Nasdaq futures +0.08% at 14682

In Europe

FTSE -0.06% at 7128

Dax +0.6% at 15235

Euro Stoxx 0+0.5% at 4075

Learn more about trading indices

CPI hits 5.4%

US stocks are set to open mixed after a higher-than-expected inflation print competes with impressive numbers from JP Morgan as earning season kicks off.

JP Morgan posted a larger than expected jump in quarterly profits thanks to the release of more loan reserves and thanks to a global boom in deal making.

JP Morgan’s earnings were unable to sufficiently distract investors from inflation data. Consumer prices rose above forecasts at 5.4% matching the largest annual gain in over a decade.

A perfect storm of shipping challenges, material shortages, rising commodity prices and higher wages have driven input costs steeply higher.

This CPI report has pretty much sealed the deal for the Fed to start tapering assets, particularly as the driving forces behind the rise in inflation show few signs of easing.

Attention will now shift towards the minutes from the September FOMC meeting. The minutes are expected to reflect the more hawkish tone of the policy announcement.

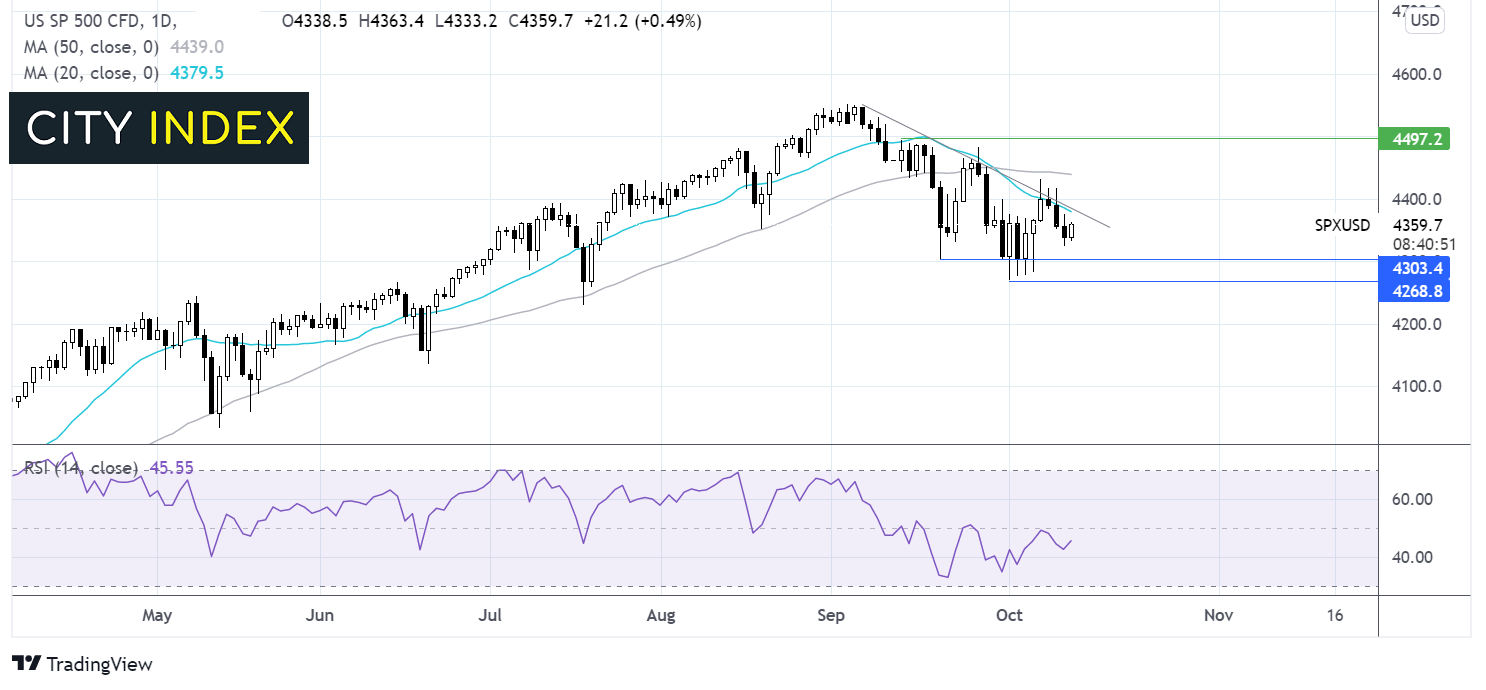

Where next for the S&P500?

The S&P has been trending lower since early September, it trades below its 20 & 50 sma on the daily chart & multi-week falling trendline. The 20 sma crossed below the 50 sma in a bearish signal. The index found support at 4270 and has since been moving higher. A move above the 20 sma and falling trendline at 4380 could signal further upside towards the 50 sma at 4445. Meanwhile bears might look for a move below 4300 to open the door to 4270 again.

FX – USD drifts, GBP rises after solid jobs data

The US Dollar has picked up off session lows but remains in the red following US CPI data. The higher than forecast reading boosts the chances of the Fed raising interest rates

GBPUSD trades higher thanks to US Dollar weakness and despite mixed data. UK economic growth picked up in August to 0.4%, from -0.1%. However, this was weaker than the 0.5% growth expected. Manufacturing production fell by more than forecast to 4.1%, down from 6% as supply chain disruptions bite.

GBP/USD +0.1% at 1.3603

EUR/USD +0.1% at 1.1545

Oil set for 5th straight day of gains

Oil prices are falling lower after 4 straight days on gains. Concerns are growing that oil demand will slow as economies suffer from elevated inflation and supply chain issues. The IMF trimmed its global growth forecast citing inflationary concerns & supply chain disruptions holding back the recovery from the pandemic.

OPEC also revised downwards its 2021 oil demand forecast to 5.8 million bpd, from 5.96 million.

Despite these concerns oil remains supported by tight supply, the ongoing energy crisis and reopening play.

WTI crude trades -0.8% at $79.43

Brent trades -0.8% at $82.38

Learn more about trading oil here.

Looking ahead

19:00 FOMC minutes

21:30 Fed Bainard

21:30 API Crude oil inventories

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Latest Indices articles

Yesterday 03:30 PM

April 18, 2024 04:46 PM