US futures

Dow futures -0.1% at 34720

S&P futures +0.05% at 4400

Nasdaq futures +0.4% at 14955

In Europe

FTSE -0.04% at 7082

Dax -0.09% at 15232

Euro Stoxx 00.19% at 4090

Learn more about trading indices

Just 194k jobs added

US stocks are set to open mixed following another huge miss from the US non-farm payrolls.

The closely watched US labour department’s job report revealed that just 194k jobs were added in September meanwhile August’s number was upwardly revised to 366k from 248k. The September number was well below the 500k that was forecast, which could still be Delta covid related.

The unemployment rate ticked lower to 4.8%, down from 5.2% and comfortably below the 5.1% forecast. Average hourly earnings were also well above estimates of 0.4%, at 0.6%. Rather than bringing answers, this reports keeps raising more questions.

The big question is whether the report was weak enough for the Fed to hold back on tapering bond purchases next month. There will not be another NFP before the November Fed meeting. And I don’t think that has been the case. This is a disappointing report but not sufficiently so to knock the Fed off course.

Whilst the USD has come off slightly, US futures are trading mixed with the tech sector set to lead gains whilst cyclicals are edging lower.

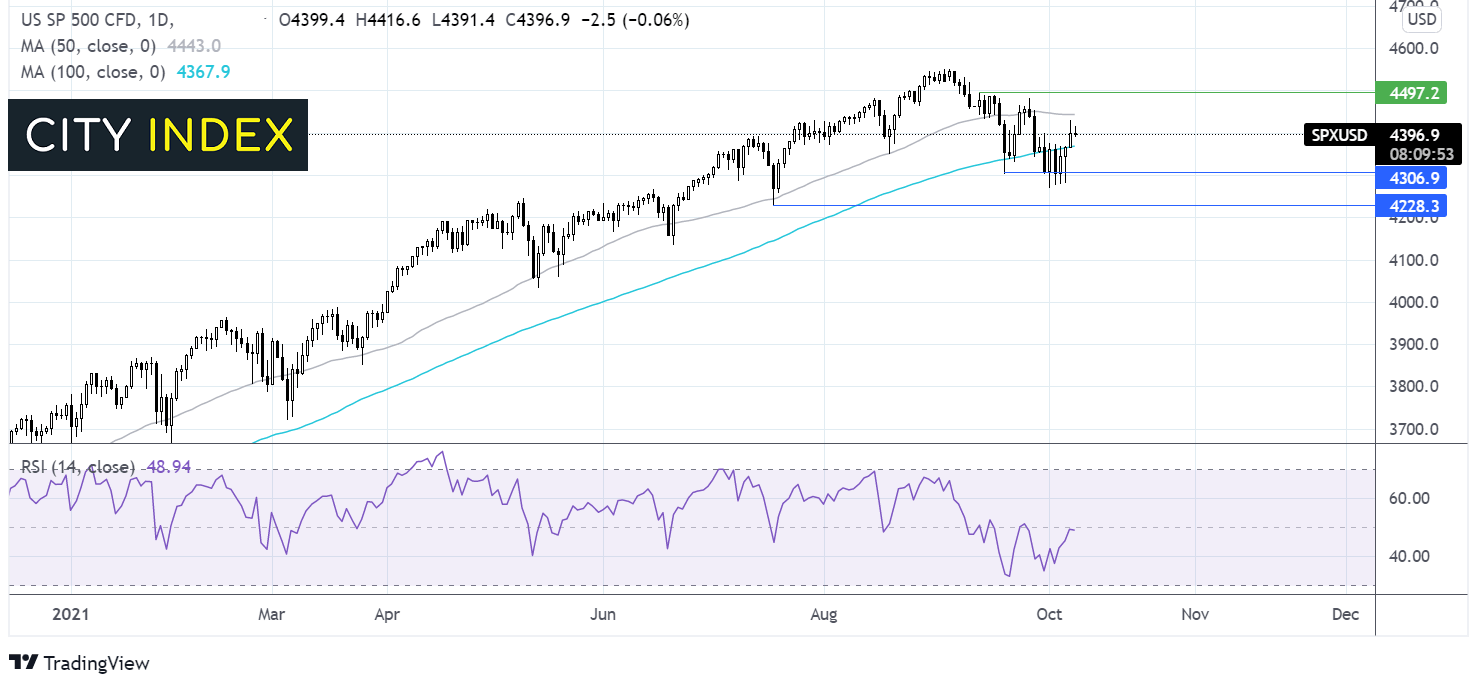

Where next for the S&P500?

The S&P continues to trade between the 50 & 200 sma. The RSI is also neutral. Buyers could wait for a move above the 50 sma at 4445 to bring 4500 back into the frame. Sellers might look for a move below 4300 for a deeper sell off.

FX – USD eases post NFP

The US Dollar has dropped lower following the release of the US NFP. The number is a huge miss and raises plenty of questions over the health of the labour market.

GBPUSD is set for weekly gains despite Brexit issues and concerns remaining. Inflation expectations continue rising as energy prices remain elevated.

GBP/USD +0.26% at 1.3650

EUR/USD +0.22% at 1.1578

Oil set for 7th straight week of gains

Oil prices are on the rise on Friday and are set to book weekly gains over 3.7% marking the 7th straight week of gains as several catalysts keep the oil price buoyant. Rising demand as economic activity rebounds and surging gas prices have under pinned oil prices. As gas prices rise expectations are for an accelerated switch from gas to oil to generate power this winter.

On the supply side, earlier this week OPEC stuck to its plan of raising output by just 400k bpd from November.

With few catalysts set to change in the near term, the upward trajectory for oil looks set to continue.

WTI crude trades +0.62% at $78.57

Brent trades +0.52% at $82.17

Learn more about trading oil here.

Looking ahead

18:00 Baker Hughes Rig Count

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

-

How to trade with FOREX.com

Follow these easy steps to start trading with FOREX.com today:

- Open a Forex.com account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels.

- Place the trade.

Latest market news

Yesterday 11:48 PM

Yesterday 11:16 PM

Yesterday 05:00 PM

Yesterday 01:13 PM

Yesterday 11:00 AM

Latest Indices articles

Yesterday 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM

April 15, 2024 06:08 AM