US futures

Dow futures +0.35% at 34988

S&P futures +0.36% at 4486

Nasdaq futures +0.35% at 15490

In Europe

FTSE -0.14% at 7060

Dax +0.3% at 15751

Euro Stoxx +0.15% at 4180

Learn more about trading indices

Stocks jump as bets of a move by the Fed ease

US stocks are set to open firmly higher following the weaker than expected inflation data. Consumer prices rose at a slower pace than expected in August prompting bets that peak inflation could have passed.

CPI rose 5.3% YoY in August, down from 5.4% in July. On a monthly basis headline CPI rose 0.3%, down from 0.5% and below the 0.4% forecast.

In core CPI the slowdown was even more evident with Core CPI rising 4% down from 4.3% and below forecasts of 4.2%.

The softer inflation prints caused investors to push back on bets that the Fed could move sooner to taper bond purchases. Easing inflation would take the heats off the Fed to move prematurely. PPI data for August also rose at a slower pace so the evidence does appear to be building that peal inflation has passed. That said, supply chain bottle necks are expected to persist for a while so its unlikely that either PPI or CPI will drop dramatically or rapidly.

As bets of the Fed tightening policy eased, stocks have jumped and the US Dollar has fallen steeply.

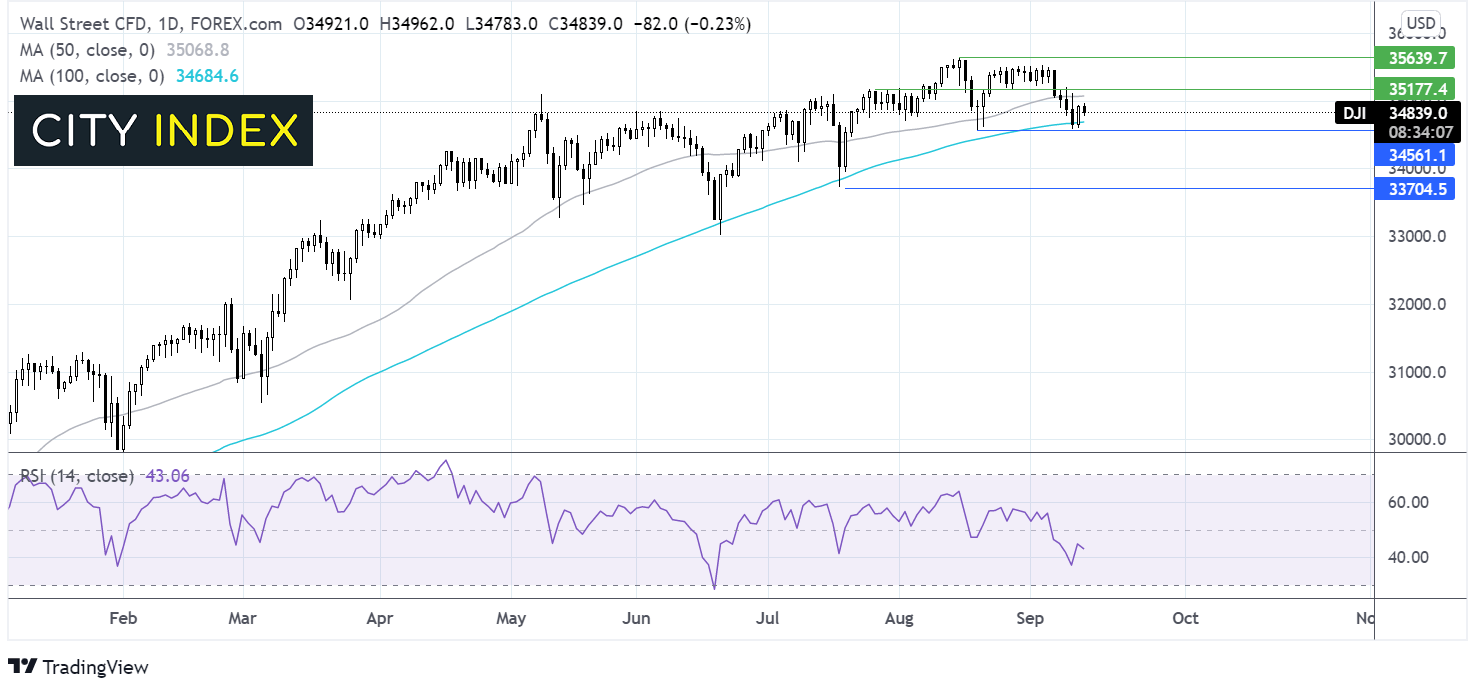

Where next for the Dow Jones?

The Dow is once again making a move towards the 50 sma, After rejection yesterday another attempt could see the index retake this key support turned resistance. Any recovery needs to retake the 50 sma at 35070 and horizontal resistance at 35180 for the buyers to gain traction. On the downside a break below the 100 sma could potentially spark a more significant selloff.

FX – USD tanks, GBP rises post jobs data

The US Dollar is plunging following the weaker inflation print.

GBP/USD the pound is pushing higher after encouraging UK labour market data. The data revealed that the number of employees on UK payrolls is back at pre-pandemic levels. The number of job vacancies rose 35% to 1 million. This suggests that the labour market can absorb the furloughed workers as the scheme winds down, prompting speculation of a sooner move by the BoE to hike interest rates.

GBP/USD +0.44% at 1.3898

EUR/USD +0.23% at 1.1837

Oil rises on US output concerns, IEA outlook

Oil prices are pushing higher trading around 6 week high as concerns over supply in the US continue to underpin the price. Supply hasn’t recovered from Hurricane Ida and is bracing for more hurricane disruption.

On the demand side, the IEA sees a 1.6-million-barrel demand rebound in October which is then expected to continue growing until the end of the year. Although the IEA did lower their global oil forecast for 2021 as a whole.

OPEC last week said they see demand easing in the final quarter but picking up to pr-pandemic levels in 2022.

Brent trades +0.4% at $73.51

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

21:30 API crude stockpiles

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 01:23 PM

Yesterday 06:01 AM

April 18, 2024 11:27 PM

April 18, 2024 04:46 PM

Latest Crude Oil articles

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM

April 10, 2024 06:07 AM