US futures

Dow futures -0.17% at 34691

S&P futures -0.17% at 4464

Nasdaq futures -0.4% at 15489

In Europe

FTSE -0.12% at 7022

Dax -0.56% at 15572

Euro Stoxx -0.27% at 4158

Learn more about trading indices

Stock set to ease, looking at a flat finish to the week

US stocks are pointing to a mildly softer open following from a mixed closed in the previous session. Despite plenty of data for investors to sink their teeth into the markets haven’t moved a great deal and the S&P500 is looking to end the week roughly where it started.

Stocks have come off their record highs but have been directionless this week even after key releases such as US CPI inflation and retail sales figures. No one really seems willing to take any big positions ahead of next week’s FOMC.

Consumer confidence due

Attention will now turn to the US Michigan consumer sentiment figures for further clues over the health of the recovery. Consumer sentiment is expected to rebound to 72.2 in September up from August’s 70.2, the lowest read since December 2011.

Inflation and Delta variant have been weighing on sentiment. Whilst inflation has eased its still historically high. Furthermore, the job market puzzle is another point of uncertainty. Given that that the US economy is based on consumption, weak morale could quicker slow economic growth.

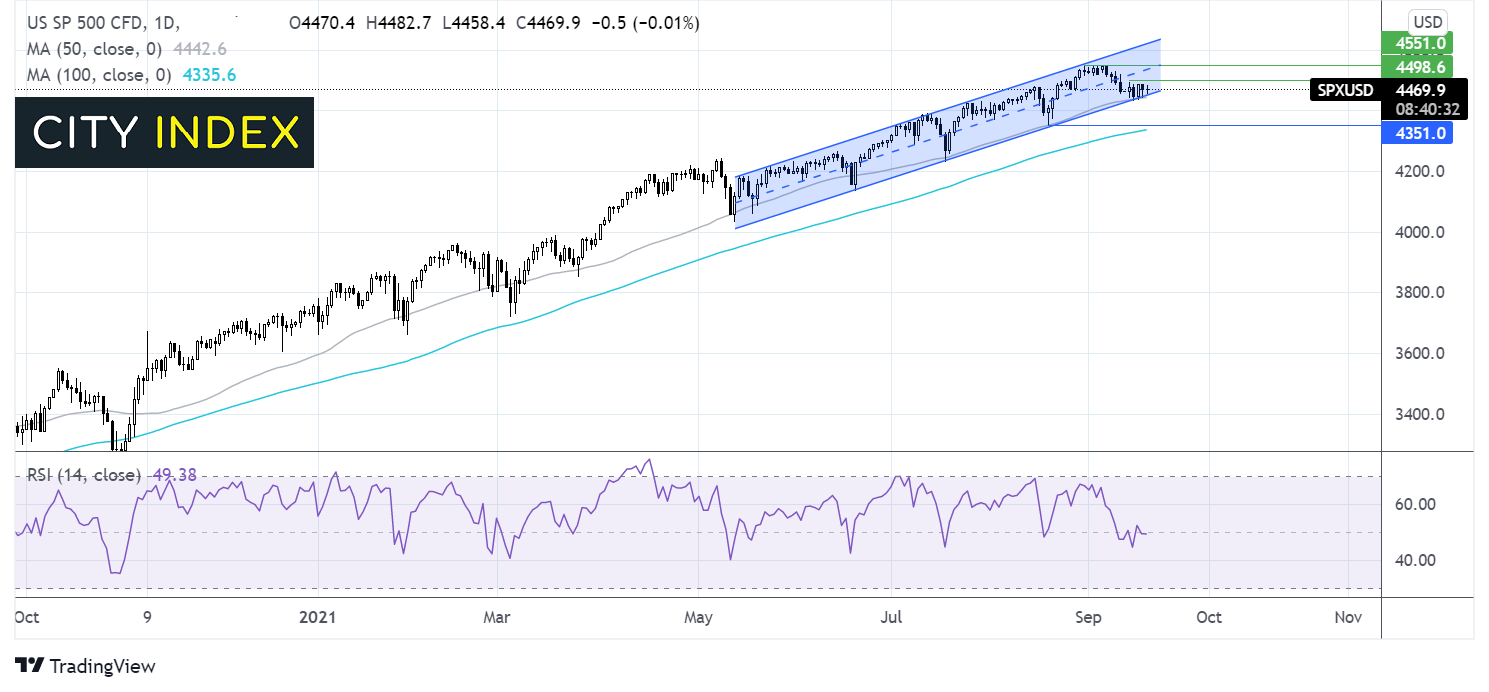

Where next for the S&P 500??

The S&P500 continues to trade within is ascending channel. After hitting resistance at 4549 has been easing lower. Last week the price has been range bound supported by the rising trendline support and the 50 sma on the daily chart at 4442. It would take a move below 4360 August low for the bias to turn bearish. Any move higher needs to clear 4491 the weekly high to push back towards 4550.

FX – USD rallies EUR slips on weak retail sales

The US Dollar is edging a few pips lower but holds near a three-week high following yesterday’s unexpected rebound in US retail sales.

GBP/USD- The pound trades under pressure following a surprise fall in retail sales. Expectations for a rise in sales was defied with a -0.9% YoY contraction, expectations had been for a 2.5% rise. On a monthly basis sales fell -0.9%, after falling -2.8% in July. This was the fourth straight month of declines amid supply chain disruptions and rising prices.

GBP/USD -0.04% at 1.3787

EUR/USD -0.36% at 1.1772

Oil eases but set for weekly gain

Oil prices are edging lower on Friday but are still looking to book a weekly gain of over 3% marking the fourth straight week of gains. Oil prices up over almost 15% from the August 23 low.

This week concerns over the slow return of supply in the US after hurricane Ida dominated and were fueled further by the larger than expected drawdown in inventories.

Supply is returning which explains the slight dip in prices. However, more broadly speaking demand is expected to continue outstripping demand as per the IEA& OPEC reports.

Baker Hughes rig count data will be in focus after the number of US rigs rose last week.

WTI crude trades -0.5% at $72.00

Brent trades -0.3% at $74.94

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

15:00 US Michigan consumer market sentiment

18:00 Baker Hughes oil rig count

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Today 08:33 AM