US futures

Dow futures -0.22% at 36225

S&P futures +0.43% at 4664

Nasdaq futures -0.81% at 16092

In Europe

FTSE +0.53% at 7309

Dax -0.12% at 16016

Euro Stoxx -0.24% at 4333

Learn more about trading indices

CPI soars - A Fed rate hike sooner?

US stocks are set for a weaker start after data revealed hat US inflation defied expectations and surged high in October. US CPI jumped to 6.2% YoY up from 5.4% in September and well above the 5.3% forecast. On a monthly basis CPI jumped 0.9%, up from 0.4% in September.

CPI is showing not signs of slowing, quite the opposite – which maybe isn’t that surprising given that PPI is at 8.6%.

Whilst the Fed say that they are focusing on employment – this number is going to get policy makers hot under the collar. The data is prompting expectations of a sooner move by the Fed, reflected in a rising US Dollar and under performance by the Nasdaq and high growth tech stocks, extra sensitive to interest rate expectations.

Banks are likely to have a strong session, along with other cyclicals – the Dow, whilst pointing to a softer start is performing better than the Nasdaq.

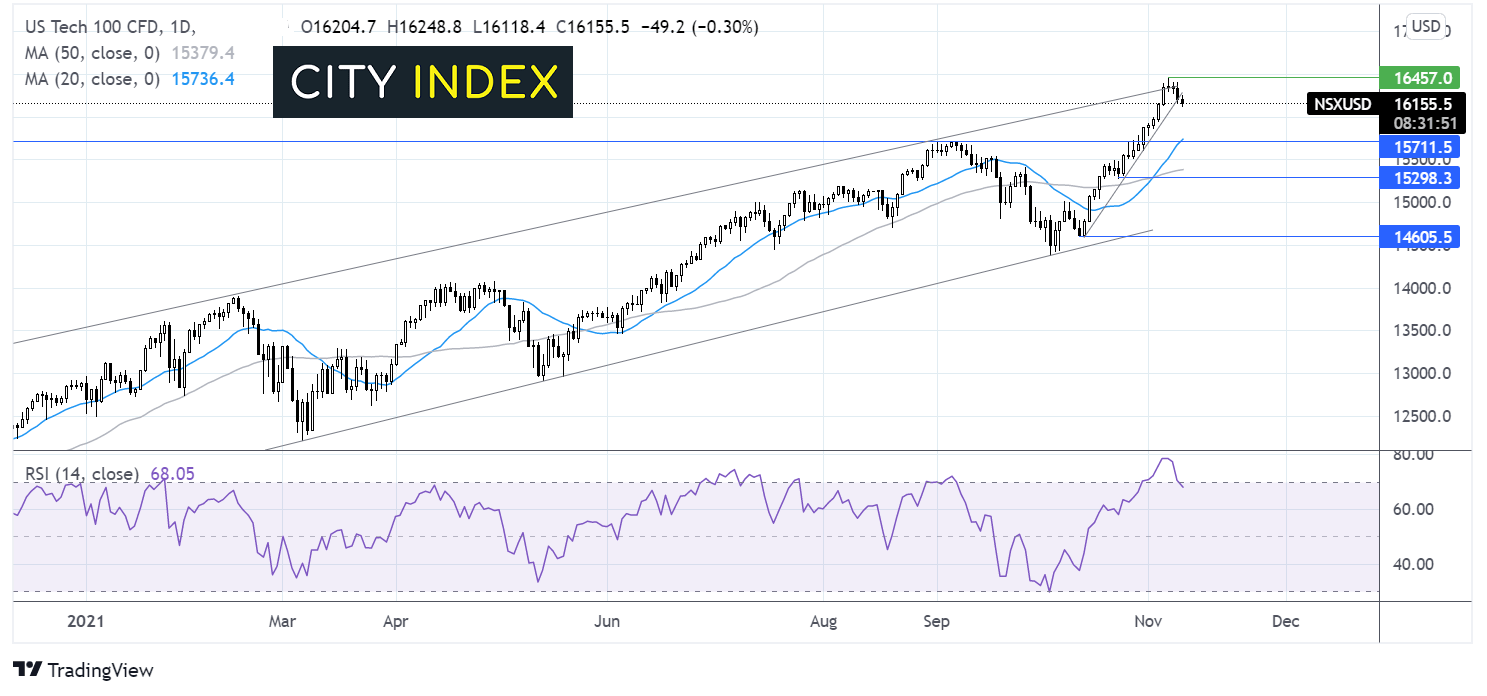

Where next for Nasdaq?

The Nasdaq is edging lower, it has slipped below the month old rising trend line dating after rejection at the rising trendline resistance dating back to August year and the new all time high of 16459. The move is bringing the RSI back from overbought territory. However, it would take a move below horizontal support at 15700 and the 20 sma at the same level to negate the near-term uptrend and expose the 50 sma at 15386.

FX – USD jumps, GBP slumps on Brexit fears

US Dollar is heading higher after 3 days of declines. Concerns over rising inflation across the globe boosted safe haven flows and US CPI prompts bets of a rate rise sooner.

GBP/USD is falling lower as Brexit headlines drag on the pound. The British government could trigger Article 16 ending co-operation with the EU over the Northern Irish border, potentially triggering a trade war with the EU.

GBP/USD -0.36% at 1.3509

EUR/USD -0.32% at 1.1556

Oil rises on global growth signals

Oil prices are easing lower after strong gains in the previous session. Oil rallied 2.4% following the release pf API crude stockpile data. The data revealed that stocks declined by 2.5 million barrels defying expectations of a 2.1-million-barrel build. The market is in wait and see mode to see whether the EIA data matches the API numbers and also to see whether the Biden administration takes action on surging oil prices.

Oil prices have rallied hard on tight supply and high demand as economies reopened and owing to the energy crisis. According to Vitol Group oil demand had returned to pre-pandemic levels and demand in Q1 2022 is likely to exceed that of the same period in 2019.

EIA inventory data is due later today.

WTI crude trades -0.5% at $82.52

Brent trades -0.25% at $84.06

Learn more about trading oil here.

Looking ahead

15:30 EIA oil inventories

How to trade with City Index

Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

- Place the trade.

Latest market news

Yesterday 08:33 AM

Latest Indices articles

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM

April 16, 2024 04:54 PM