Place the trade.

US futures

Dow futures +0.34% at 34698

S&P futures +0.35% at 4400

Nasdaq futures +0.34% at 14909

In Europe

FTSE -0.0% at 7070

Dax +0.1% at 15170

Euro Stoxx +0.45% at 4080

Learn more about trading indices

Inflation fears ease

US stocks are set to extend gains from the previous session as debt ceiling and energy concerns ease. Progress in debt ceiling talks is boosting the mood in the market. The proposed deal in Washington will effectively see the can kicked down the road to December buying time and easing concerns. Whilst this is clearly a short-term answer, it is enough to keep the markets happy.

Separately Russia’s proposed intervention in the energy market to bring prices down is also being well received. Natural gas prices tumbled on the prospect of increased supply from Russia to Europe, whilst oil prices also came off as inventories unexpectedly rose. The easing of prices in the energy markets is cools bets of a sooner move by the Fed, boosting equities which pulling on the US Dollar.

US jobless claims rose by less than expected. Initial claims rose by 326k less than the 364k recorded in the previous week and less than the 348k forecast. After a few wobbly weeks initial claims are heading back in the direction that that Fed wants to see. This is the final piece of the jigsaw ahead of tomorrow’s NFP. Evidence is pointing to an upbeat number.

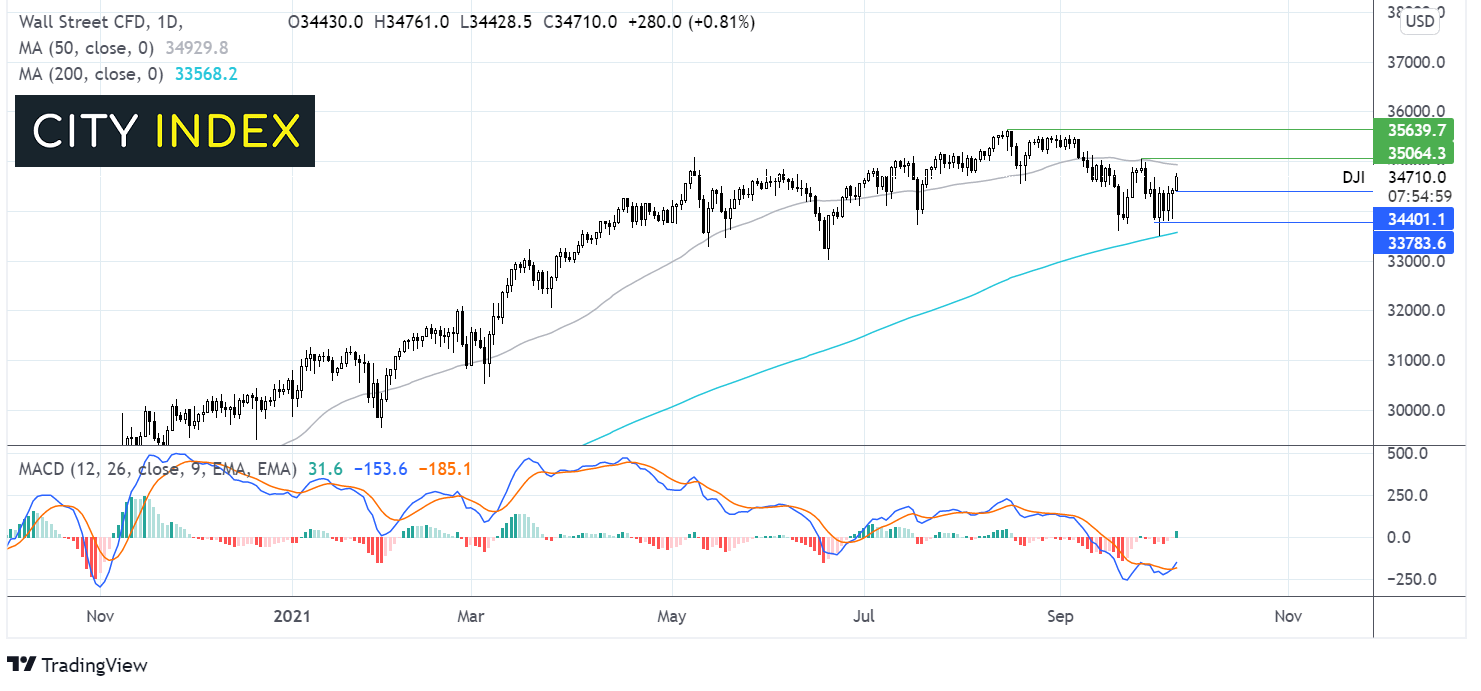

Where next for the Dow Jones?

The Dow Jones is extending gains, pushing above Friday’s high of 34685 and targeting the 50 sma at 34930. The bullish cross over on the MACD is keeping buyers optimistic. A move above 34930 and 35065 the September 27 high will be key for cementing the bullish bias. On the flip side a move below today’s low of 34400 could see sellers gain traction towards 33785.

FX – USD steady, EUR struggles as German industrial output slumps

The US Dollar has recovered earlier losses following the US jobless claims numbers. The better than forecast print supports the view that the Fed could tighten sooner. That said with Russia intervening in the energy market, inflation could still be controlled.

EUR/USD is struggling to gain ground following German industrial production which dropped 4% MoM, after rising 1.3% in August.

GBP/USD +0.04% at 1.3591

EUR/USD -0.05% at 1.1553

Oil eases as inventories rise, US consider selling strategic reserves

Oil prices are falling lower extending losses from the previous session as EIA reported oil inventories unexpectedly rose and the US considers selling oil from its strategic reserves. Easing pressure in the energy market more broadly, Russia said that it was ready to intervene to stabilize the natural gas market.

Both oil contracts fell 2% on Wednesday and are extending those losses today. The tightness that we have seen in the oil markets over the past few weeks could be eased with the US selling reserves and more gas flowing to Europe.

Despite these moves to cools the oil market, Goldman Sachs remain bullish on the price of oil saying that even if the US sell strategic reserves, they still expect oil prices to get within $3 of its $90 Brent year end price

WTI crude trades -1% at $75.98

Brent trades -0.49% at $79.80

Learn more about trading oil here.

Looking ahead

15:00 Canada Ivey PMI

16:45 ECB’s Lane speaks

17:00 BoC Governor speech

This content will only appear on City Index websites!

How to trade with City Index

- Follow these easy steps to start trading with City Index today:

- Open a City Index account, or log-in if you’re already a customer.

- Search for the market you want to trade in our award-winning platform.

- Choose your position and size, and your stop and limit levels

Latest market news

Today 11:14 AM

Today 08:28 AM

Yesterday 03:30 PM

Yesterday 01:23 PM

Latest Indices articles

Yesterday 03:30 PM

April 18, 2024 04:46 PM

April 17, 2024 11:00 AM

April 16, 2024 08:00 PM