US futures

Dow futures +0.13% at 35796

S&P futures +0.09% at 4576

Nasdaq futures +0.14% at 15575

In Europe

FTSE -0.16% at 7267

Dax -0.5% at 15657

Euro Stoxx -0.19% at 4216

Learn more about trading indices

Earnings remain in focus

US stocks are set to open mildly higher amid mixed earnings and falling commodity prices.

Microsoft is set open over 1% higher after a boom in sales. Companies moving to the cloud has lifted revenue in Microsoft’s cloud business to $20 billion for the first time. Microsoft it is snapping at Apple’s heels to take the crown of the world’s most valuable company. All eyes will now be on Apple’s results to see whether the time has come for Apple to pass the crown on.

Whilst McDonald’s, Coca-Cola and Twitter all advanced pre-market on positive earnings, Visa and Mastercard declined.

Inflation concerns continued to plague the market. Australian inflation jumping to the highest level in 6 years refocused investors attention back onto rising prices and the negative impact on growth.

The fact that the market is still rising, albeit slightly, suggests that earning optimism is still overshadowing inflation, supply chain and labour market jitters. However, concerns remain that these headwinds could start eating into margins and hamper the economic recovery going forward.

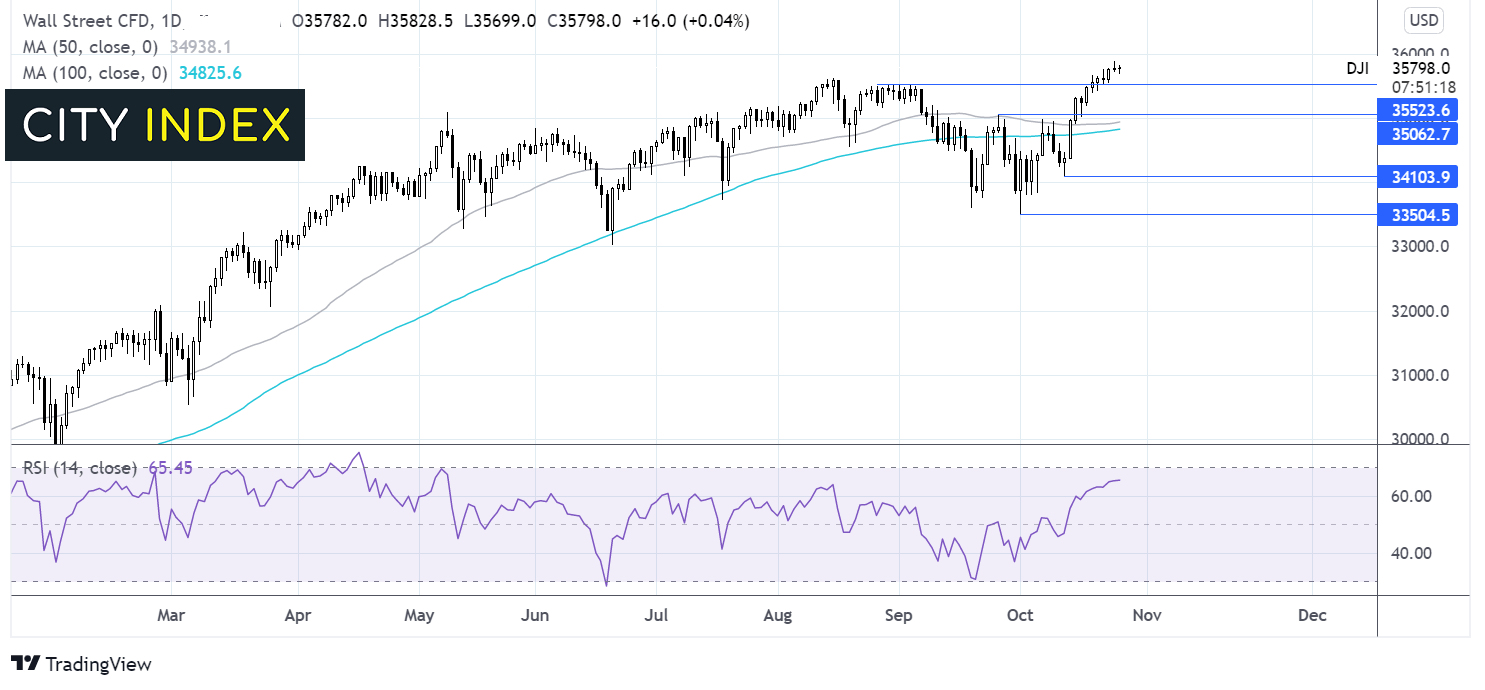

Where next for the Dow Jones Index?

After breaking out at the end of last week the Dow is set to climb higher. There are few signs on the chart that this move higher has run its path. Support can be seen at 35535 and 35000 – a move below here could negate the near term up trend. It would take a move below 34125 for sellers to gain momentum.

FX – USD tip toes higher

The US Dollar is edging higher building on gains from the previous session after consumer confidence unexpectedly in October, after falling for three straight months. Concerns over Delta covid appeared to ease. US durable goods order are due and are expected to fall for the first time in 5 months

GBP/USD -The Pound is trading under pressure as the Chancellor is giving his autumn budget. Many measures have already been announced. The OBR’s GDP forecast was upwardly revised to 6.5% from 4%

GBP/USD -0.2% at 1.3735

EUR/USD +0.17% at 1.1616

Oil pares losses

Oil prices are heading lower after industry data revealed that crude oil stocks piles rose by 2.3 million barrels, more than the 1.9 million expected and fuel inventories unexpectedly rose by 500,000 barrels. The API data release has given a reason for traders to take profits off the table, particularly after crude oil hit fresh multi year highs on Monday.

Despite today’s fall the broader uptrend remains firmly intact as investors look ahead to the release of EIA inventory data.

WTI crude trades +0.18% at $83.60

Brent trades +0.12% at $85.31

Learn more about trading oil here.

Looking ahead

15:00 BoC interest rate decision

Latest market news

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 25, 2024 01:12 PM

April 25, 2024 11:14 AM

Latest Indices articles

April 25, 2024 03:09 PM

April 25, 2024 03:00 PM

April 24, 2024 03:30 PM

April 18, 2024 04:46 PM