US futures

Dow futures +0.2% at 33450

S&P futures +0.02% at 4090

Nasdaq futures -0.3% at 13721

In Europe

FTSE -0.2% at 6922

Dax +0.1% at 15208

Euro Stoxx +0.03% at 3981

Learn more about trading indices

Tech stocks ease lower as yields pick up

US futures are heading for a mixed open on Friday, with tech heavy Nasdaq set to under-perform after booking 1% gains in the previous session.

All three major indices closed higher in the previous session supported by a dovish US central bank. Fed Chair Powell echoed the accommodative tone of the FOMC minutes, released on Wednesday, lifting the S&P to a fresh record high.

Today treasury yields are once again climbing higher, with the benchmark 10 year treasury yield +2.3% at 1.67, which is slightly impacting demand for tech growth stocks.

Despite today's rise, the Nasdaq has outperformed its peers across the week after disappointing jobless claims, and dovish calls from the Fed's nest. The Fed has been clear that it needs to see a prolonged period of strong data to tighten policy. The recovery will be uneven and data this week has coincided with that.

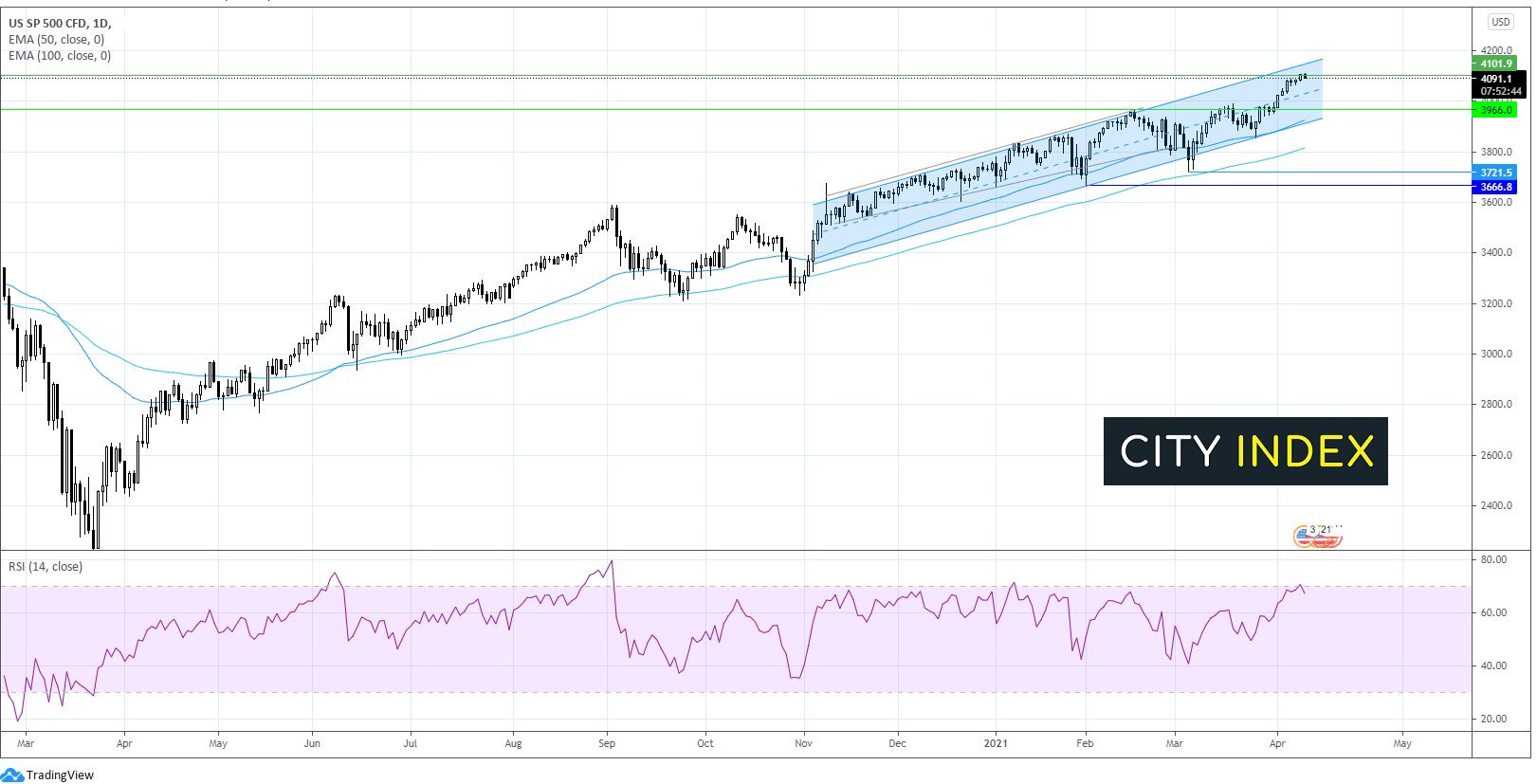

S&P 500 Chart

The S&P is easing back after hitting an all time high of 4111 in the previous session. The index remains at the top end of the ascending channel. However with the RSI reaching into over bought territory a pull back or at least some consolidation was on the cards. S&P trades -0.2% at the time of writing. The trend remains bullish. It would take a move below support at 3980 to negate the current up trend trend.

Inflation data

US PPI data is due shortly and is expected to show 0.5% MoM in-line with last month. On an annual basis PPI is forecast to increase 3.8% in March up from 2.8%.

The Fed has repeatedly said that it is willing to look through a rise in inflation, which it expects to be temporary.

Chinese PPI rose 4.4% YoY in the fastest increase since July 2018 and significantly ahead of February’s 1.7%. Expectations had been for 3.5% increase.

FX – EUR outperforms, GBP has worst week this year

The US Dollar on the rise tracing US treasury yields higher. However, the DXY is on track for its worst weekly performance since mid-December.

GBP/USD – The Pound has under-performed despite strong fundamentals. After particularly impressive gains in the first quarter investors are taking profits off the table. GBPUSD trades -0.8% this week.

Meanwhile the Euro has outperformed across the week, up 1% since Monday, on expectations that the sluggish vaccine rollout in the region will start to pick up quickly. The major economies in Europe such as Germany, Spain, France and Italy expect to vaccinate 70% of the population by the end of June.

GBP/USD -0.1% at 1.3715

EUR/USD trades -0.2% at 1.1881

Oil trades sideways with output compliance in focus

Crude oil prices continue to trade sideways after a steep drop at the start of the week as investors continue to weigh up the prospect of additional supply from OPEC as from next month against a weaker demand outlook as covid cases rise.

Concerns over compliance with OPEC output curbs are also surfacing after an S&P report pointed to oversupply by OPEC+ members to the tune of 450,000 barels per day in March with Russia and Iraq the worst offenders.

US crude trades -0.4% at $59.45

Brent trades -0.5% at $62.71

Learn more about trading oil here.

The complete guide to trading oil markets

Looking ahead

13:30 US PPI

13:30 Canadian jobs report

18:00 Baker Hughes oil rig count

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Crude Oil articles

April 22, 2024 04:00 PM

April 19, 2024 03:35 AM

April 17, 2024 05:00 PM

April 17, 2024 03:02 AM